Executive Summary

Can my employer take back vested RSUs?

Sometimes—if your grant agreement includes clawback triggers and enforcement mechanisms. Vesting makes shares ‘yours’ for many purposes, but contracts can still require repayment or forfeiture under specific conditions depending on structure and law.

Are clawbacks only for executives?

Mandatory executive clawback contexts exist in public company governance, but private companies can include clawback language broadly. Read your documents—titles don’t determine enforceability.

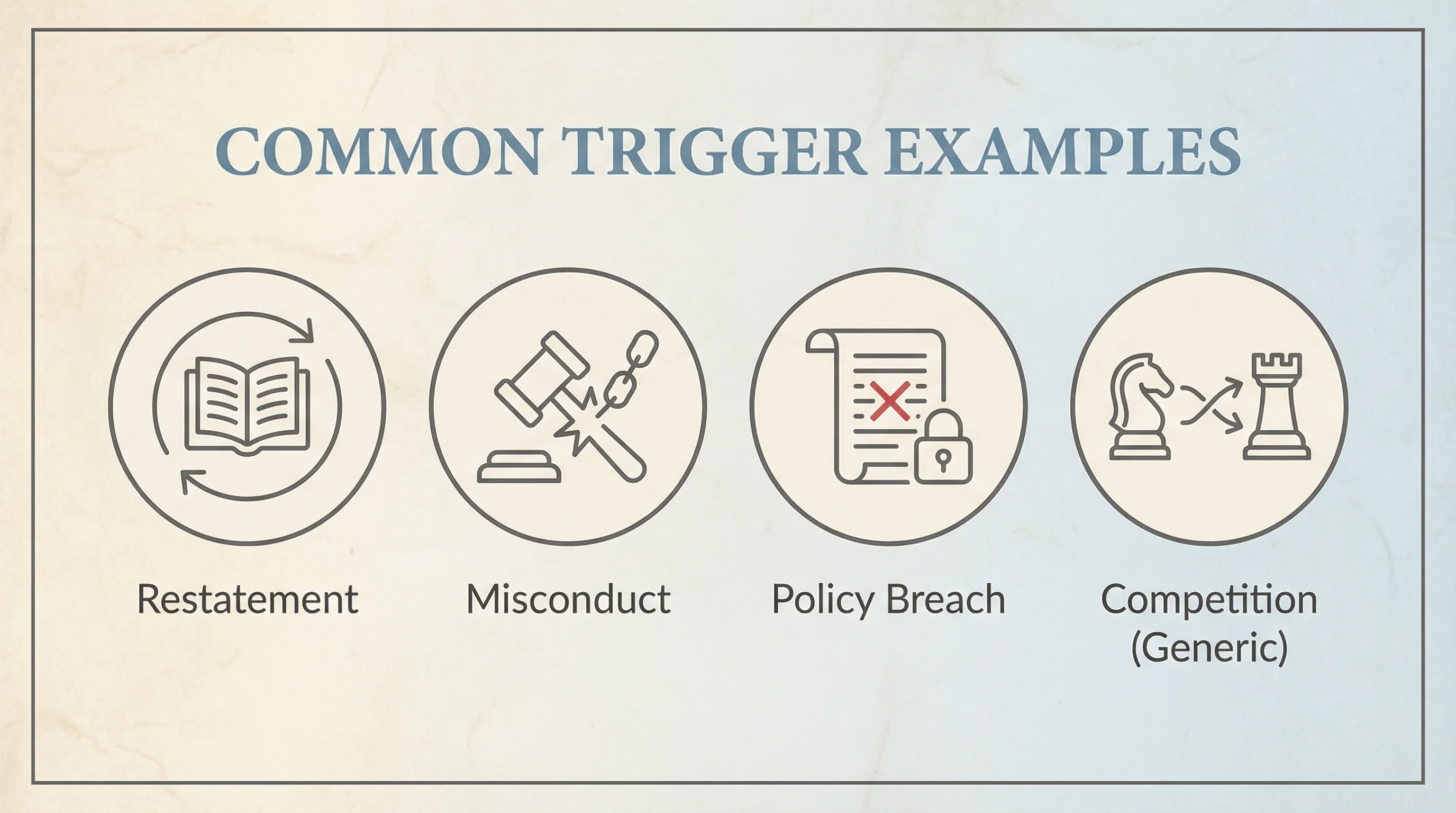

What triggers are common?

Accounting restatements, violation of policies, fraud, confidential information misuse, and sometimes competition or solicitation—each agreement differs.

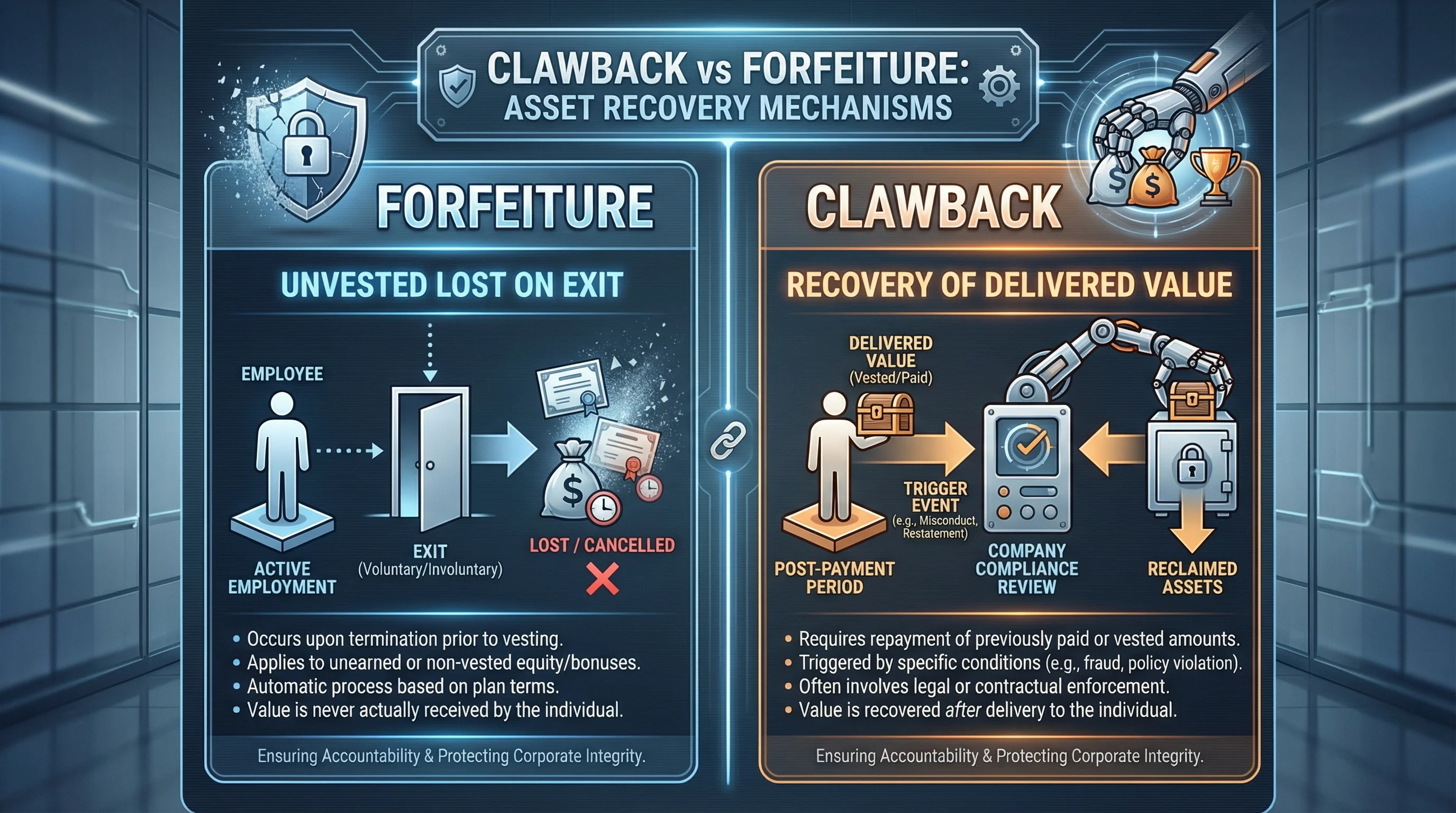

Figure 1: Different mechanisms—different contract language.

Clawback vs Forfeiture

| Concept | Typical meaning |

|---|---|

| Forfeiture | Unvested awards lost on termination |

| Clawback | Recovery of value already delivered |

Figure 2: Triggers vary—your agreement controls.

Practical Employee Checklist

- Search grant PDFs for clawback, malus, repayment

- Check good leaver / bad leaver definitions

- Understand equity vs cash clawback mechanics

Figure 3: Paper trail matters if repayment is disputed.

Tax note

Repaying amounts previously taxed can create complex tax reporting—see IRS materials and a CPA.

Related

Disclaimer

Not legal advice—consult counsel for enforceability in your state.

Primary sources

| Source | URL |

|---|---|

| IRS Publication 525 | https://www.irs.gov/publications/p525 |