Executive Summary

How are RSUs taxed at vesting?

RSUs are taxed as ordinary income at vesting based on the fair market value of the shares on the vesting date, with employer withholding for federal income tax, FICA, and state taxes.

Restricted Stock Units (RSUs) are a popular form of employee compensation, particularly in the tech and startup sectors. However, understanding their taxation can be complex. RSUs are taxed as ordinary income at the time they vest, which means the fair market value (FMV) of the shares on the vesting date is included in your taxable income. This income is reported on Form W-2, and your employer will withhold federal income tax, FICA, and state taxes. The federal withholding is typically at a flat rate of 22% for supplemental wages, but this may not cover your entire tax liability if you are in a higher tax bracket. Proper planning is essential to avoid underpayment penalties and to optimize your tax situation.

The bottom line: RSUs can significantly impact your tax liability at vesting, and understanding the mechanics of their taxation is crucial to avoid surprises and optimize your financial planning.1

Critical Warning: Failing to plan for the tax implications of RSU vesting can lead to unexpected tax bills and potential penalties for underpayment.2

Understanding RSU Vesting Taxation

The Basics of RSU Taxation

RSUs are taxed under Internal Revenue Code (IRC) Section 83, which stipulates that property transferred in connection with services is included in gross income when it becomes substantially vested. For RSUs, this occurs at vesting when the shares are delivered to the employee. The taxable amount is calculated as the number of shares vesting multiplied by the FMV per share on the vesting date.

Example Calculation

Consider an employee who has 1,000 RSUs vesting at a FMV of $50 per share. The ordinary income recognized would be:

1,000 RSUs × $50/share = $50,000

The employer withholds approximately 22% for federal taxes ($11,000), 1.45% for Medicare ($725), and 6.2% for Social Security ($3,100, assuming the wage base is not exceeded), plus applicable state taxes (e.g., California at 10.23%, which is $5,115). After sell-to-cover, the employee receives approximately 730 shares.

Withholding Rules and Implications

RSUs are treated as supplemental wages, and federal withholding is typically at a flat rate of 22% for amounts up to $1 million, increasing to 37% for amounts above this threshold. However, if your marginal tax rate is higher than 22%, you may face a shortfall. For example, if you are in the 37% tax bracket, the shortfall on a $50,000 vesting would be:

37% of $50,000 = $18,500

22% of $50,000 = $11,000

Shortfall = $18,500 - $11,000 = $7,500

Important Note: Insufficient withholding can lead to underpayment penalties unless you meet the safe harbor requirements, which involve paying 90% of your current year's tax or 110% of the previous year's tax liability.

Key Takeaways

- RSUs are taxed as ordinary income at vesting.

- Federal withholding is at a flat rate of 22%, which may not cover your full tax liability.

- Planning is crucial to avoid underpayment penalties.

Year-End Strategies and Deadlines

Safe Harbor and Estimated Payments

To avoid underpayment penalties, you can use the safe harbor rule, which requires paying either 90% of your current year's tax liability or 110% of your previous year's tax liability. This can be achieved through estimated tax payments using Form 1040-ES.

Example: Safe Harbor Calculation

Assume your 2025 tax liability was $40,000. To meet the safe harbor for 2026, you would need to pay:

110% of $40,000 = $44,000

If your estimated 2026 tax liability is $50,000, you must pay at least $45,000 (90% of $50,000) to avoid penalties.

No Deferral and 83(b) Election

RSUs cannot be deferred; they are taxed at vesting. However, an 83(b) election, which allows you to pay taxes on the FMV at the time of grant rather than vesting, is generally not applicable to RSUs since they are not subject to a substantial risk of forfeiture at grant.

Critical Warning: Failing to make estimated payments or adjust withholdings can lead to significant tax liabilities and penalties.

Key Takeaways

- Use the safe harbor rule to avoid penalties.

- RSUs are taxed at vesting; no deferral is possible.

- The 83(b) election is not typically applicable to RSUs.

Comparative Withholding and Tax Planning

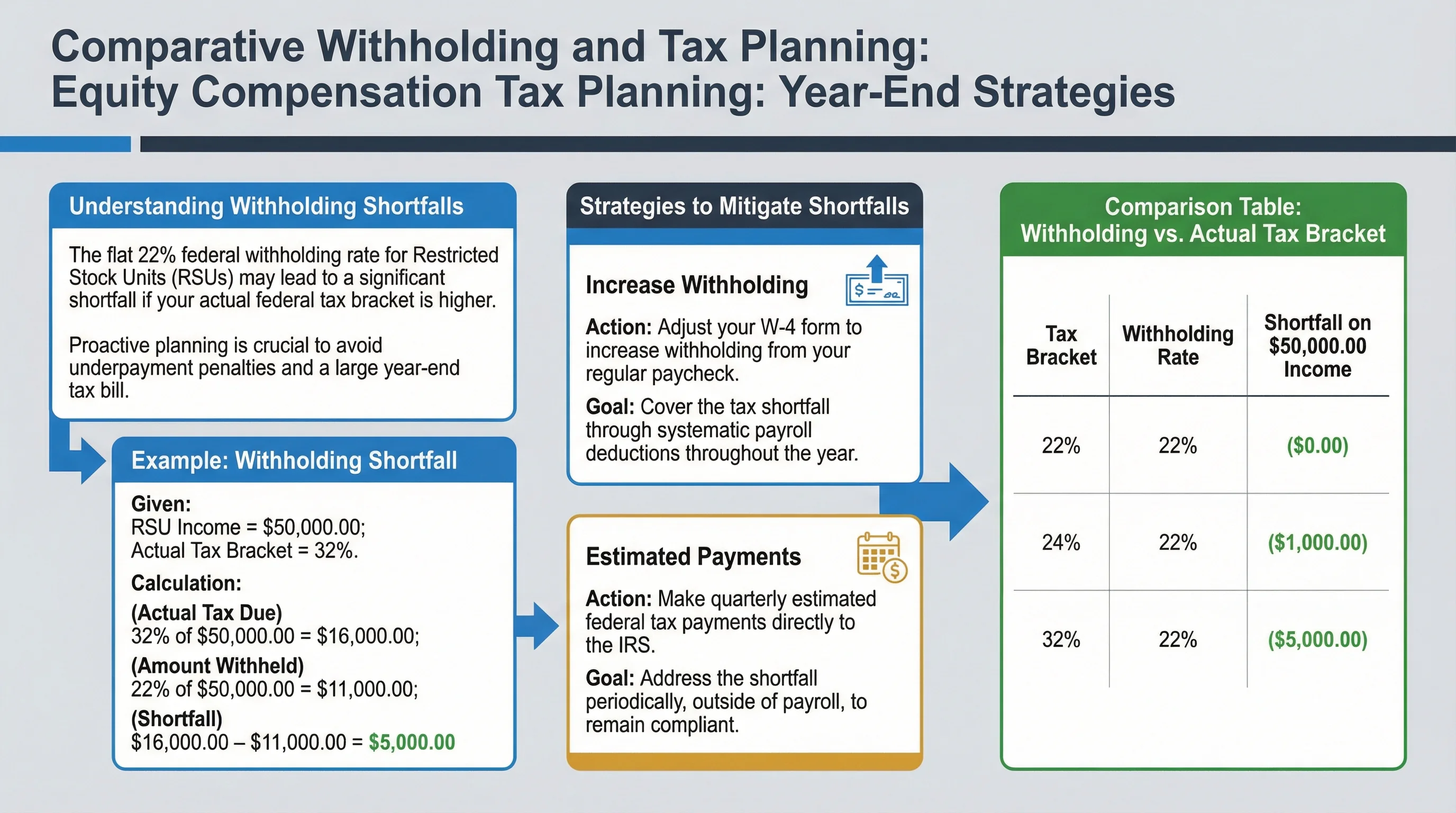

Understanding Withholding Shortfalls

The flat 22% federal withholding rate for RSUs may lead to a shortfall if your actual tax bracket is higher. It's important to plan for this by either increasing your withholding or making estimated tax payments.

Example: Withholding Shortfall

If your tax bracket is 32% and you have $50,000 in RSU income:

32% of $50,000 = $16,000

22% of $50,000 = $11,000

Shortfall = $16,000 - $11,000 = $5,000

Strategies to Mitigate Shortfalls

- Increase Withholding: Adjust your W-4 to increase withholding from your regular paycheck.

- Estimated Payments: Make quarterly estimated tax payments to cover the shortfall.

Comparison Table: Withholding vs. Actual Tax Bracket

| Tax Bracket | Withholding Rate | Shortfall on $50,000 |

|---|---|---|

| 22% | 22% | $0 |

| 24% | 22% | $1,000 |

| 32% | 22% | $5,000 |

| 37% | 22% | $7,500 |

Key Takeaways

- Plan for withholding shortfalls if your tax bracket exceeds 22%.

- Use estimated payments or adjust withholding to avoid penalties.

Real-World Scenarios and Examples

Scenario 1: High-Income Earner

Consider a high-income earner with RSUs vesting worth $200,000. The federal withholding at 22% would be $44,000, but if they are in the 37% bracket, their actual liability is $74,000, resulting in a $30,000 shortfall.

Calculation

37% of $200,000 = $74,000

22% of $200,000 = $44,000

Shortfall = $74,000 - $44,000 = $30,000

Scenario 2: State Tax Considerations

An employee in California with $100,000 in RSUs would face a 10.23% state tax, adding $10,230 to their tax liability. Combined with federal taxes, this significantly impacts their net income.

Calculation

10.23% of $100,000 = $10,230

Federal (22%) = $22,000

Total Tax = $32,230

Scenario 3: Sell-to-Cover Strategy

An employee with 500 RSUs vesting at $60/share uses a sell-to-cover strategy to pay taxes. They sell 110 shares to cover $6,600 in taxes, leaving them with 390 shares.

Calculation

500 RSUs × $60/share = $30,000

22% Federal Tax = $6,600

Shares Sold = $6,600 / $60 = 110

Remaining Shares = 500 - 110 = 390

Key Takeaways

- High-income earners should plan for significant withholding shortfalls.

- State taxes can substantially increase your overall tax liability.

- Sell-to-cover is a common strategy to manage tax payments.

Common Mistakes and Pitfalls to Avoid

Mistake 1: Ignoring State Taxes

Many employees focus solely on federal taxes and overlook state tax implications, which can lead to unexpected liabilities.

Mistake 2: Underestimating Withholding Shortfalls

Assuming the 22% withholding rate is sufficient can result in a large tax bill if you are in a higher tax bracket.

Mistake 3: Failing to Plan for AMT

For those with Incentive Stock Options (ISOs), failing to account for the Alternative Minimum Tax (AMT) can lead to significant tax surprises.

Key Takeaways

- Always consider state taxes in your planning.

- Review your tax bracket to ensure adequate withholding.

- Be aware of AMT implications if you have ISOs.

Frequently Asked Questions

What is the tax treatment of RSUs at vesting?

Answer: RSUs are taxed as ordinary income at vesting based on the FMV of the shares. This income is reported on Form W-2, and your employer withholds federal, FICA, and state taxes.

Source: IRS, IRC §83

How can I avoid underpayment penalties with RSUs?

Answer: Use the safe harbor rule by paying 90% of your current year's tax or 110% of your previous year's tax liability through estimated payments or increased withholding.

Source: IRS Publication 505

Can I defer taxes on RSUs?

Answer: No, RSUs are taxed at vesting, and deferral is not possible. The 83(b) election is not applicable to RSUs.

Source: Treas. Reg. §1.83-2

What is a sell-to-cover strategy?

Answer: A sell-to-cover strategy involves selling a portion of your vested shares to cover the tax liability, allowing you to retain the remaining shares.

Source: IRS, Form W-2 Instructions

How does the AMT affect my RSUs?

Answer: The AMT does not directly affect RSUs, but if you have ISOs, the bargain element can create an AMT adjustment. Plan accordingly to avoid surprises.

Source: IRS, AMT Guidelines

Are there any exceptions to the standard RSU taxation?

Answer: Generally, no exceptions apply to RSUs. However, in private companies, an 83(b) election might be possible for restricted stock awards.

Source: Treas. Reg. §1.83-2

What happens if I sell my RSUs immediately after vesting?

Answer: If you sell immediately, any gain or loss is typically minimal. However, if you hold the shares for more than a year, you may qualify for long-term capital gains rates.

Source: IRS, Capital Gains Guidelines

How do state taxes impact my RSU taxation?

Answer: State taxes can significantly increase your tax liability, especially in high-tax states like California. Ensure you account for these in your planning.

Source: State Tax Guidelines

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS, IRC §83 | Regulation | Link |

| IRS Publication 505 | Publication | Link |

| IRS, Form W-2 Instructions | Form Instructions | Link |

| Treasury Regulation §1.83-2 | Regulation | Link |

This comprehensive guide provides a detailed understanding of RSU taxation, ensuring you are well-prepared to manage your tax obligations effectively. By planning ahead and understanding the nuances of RSU taxation, you can avoid common pitfalls and optimize your financial outcomes.

For more detailed guides on related topics, check out our articles on RSU Taxation Basics, AMT Planning for Stock Options, and Tax-Loss Harvesting with RSUs and Stock Options.

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Tax laws vary by jurisdiction and change frequently. Always consult a qualified tax professional (CPA, tax attorney, enrolled agent) before making decisions based on this information. The authors accept no liability for actions taken based on this content.