Executive Summary

When should I sell my company stock?

There's no single answer—it depends on concentration risk, tax timing, and liquidity needs. A practical approach: (1) If company stock exceeds 10-20% of your net worth, consider diversifying. (2) Holding >1 year after vesting/exercise qualifies for long-term capital gains (0-20% vs up to 37% ordinary). (3) Sell systematically over time rather than all at once to reduce timing risk.

The decision to sell company stock is one of the most consequential financial choices employees face. If you have RSUs specifically, see our When to sell RSUs guide for a focused take. Hold for tax efficiency and you may capture upside—or watch a concentrated position collapse. Sell for diversification and you lock in gains but may leave money on the table.1 This guide provides a framework, not a prescription.

The bottom line: Balance concentration risk, tax timing, and liquidity. Most employees benefit from diversifying over time—selling in tranches rather than all-or-nothing.2

Critical Warning: Holding a large concentration in a single stock is risky. Enron, Lehman, and countless startups have shown that company stock can go to zero. Diversification protects you from firm-specific risk.3

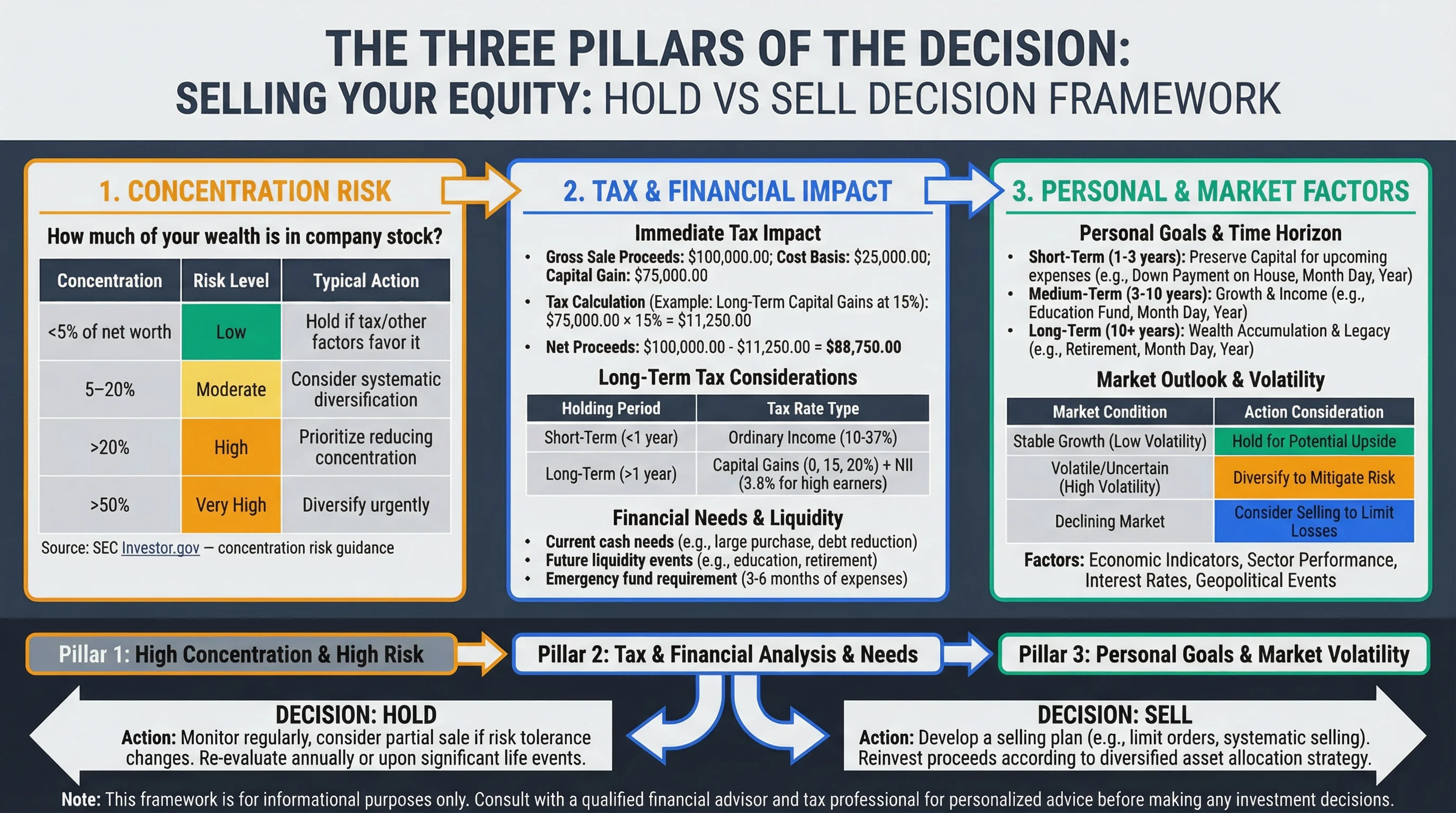

The Three Pillars of the Decision

1. Concentration Risk

How much of your wealth is in company stock?

| Concentration | Risk Level | Typical Action |

|---|---|---|

| <5% of net worth | Low | Hold if tax/other factors favor it |

| 5–20% | Moderate | Consider systematic diversification |

| >20% | High | Prioritize reducing concentration |

| >50% | Very High | Diversify urgently |

Source: SEC Investor.gov — concentration risk guidance

Figure 1: Concentration risk — when company stock becomes too much of your wealth.

If your job, salary, and equity are all tied to one company, you have triple concentration. A company downturn affects your income and your wealth. Diversifying equity reduces that risk.

2. Tax Timing

Short-term vs long-term capital gains:

| Holding Period | Tax Rate | When It Applies |

|---|---|---|

| <1 year from vest/exercise | Ordinary income rates (up to 37%) | Short-term |

| ≥1 year | Long-term: 0%, 15%, or 20% + 3.8% NIIT | Long-term |

Example: $100,000 gain. At 37% ordinary: $37,000 tax. At 20% LTCG: $20,000 tax. Savings: $17,000 by holding >1 year.

Related Guides: Capital Gains Calculator, Holding Period Tracker.

Figure 2: Tax timing — short-term vs long-term capital gains rates.

3. Liquidity Needs

Do you need the cash?

| Need | Consideration |

|---|---|

| Down payment, emergency fund | Selling may be necessary—don't let tax tail wag the dog |

| Exercise cost (options) | May need to sell some shares to fund exercise |

| Tax bill | RSU vesting creates tax due—selling at vest can cover it |

| No immediate need | More flexibility to optimize for tax and concentration |

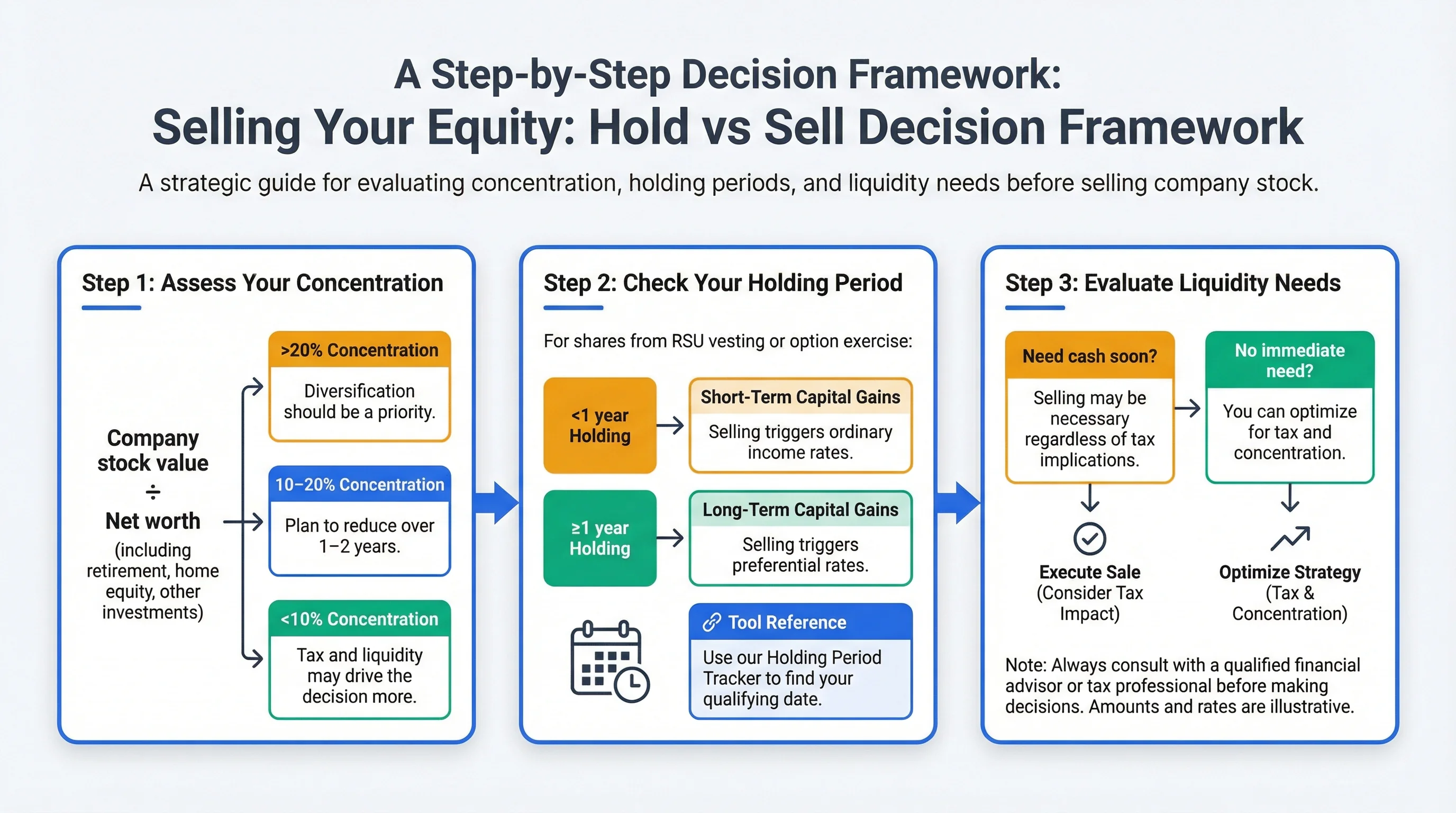

A Step-by-Step Decision Framework

Step 1: Assess Your Concentration

Calculate: Company stock value ÷ Net worth (including retirement, home equity, other investments).

- If >20%: Diversification should be a priority

- If 10–20%: Plan to reduce over 1–2 years

- If <10%: Tax and liquidity may drive the decision more

Step 2: Check Your Holding Period

For shares from RSU vesting or option exercise:

- <1 year: Selling triggers short-term gains (ordinary income rates)

- ≥1 year: Selling triggers long-term gains (preferential rates)

Use our Holding Period Tracker to find your qualifying date.

Step 3: Evaluate Liquidity Needs

- Need cash soon? Selling may be necessary regardless of tax

- No immediate need? You can optimize for tax and concentration

Step 4: Choose a Strategy

| Strategy | Best For | How |

|---|---|---|

| Sell at vest (RSU) | High concentration, need cash | Sell immediately; tax already due |

| Hold to qualify (LTCG) | Low concentration, no liquidity need | Hold >1 year, then sell |

| Systematic diversification | Moderate concentration | Sell X% per quarter/year |

| Sell to fund exercise | Options, need cash for strike | Sell enough to cover exercise + tax |

Figure 3: Decision framework — concentration, tax timing, liquidity, and strategy.

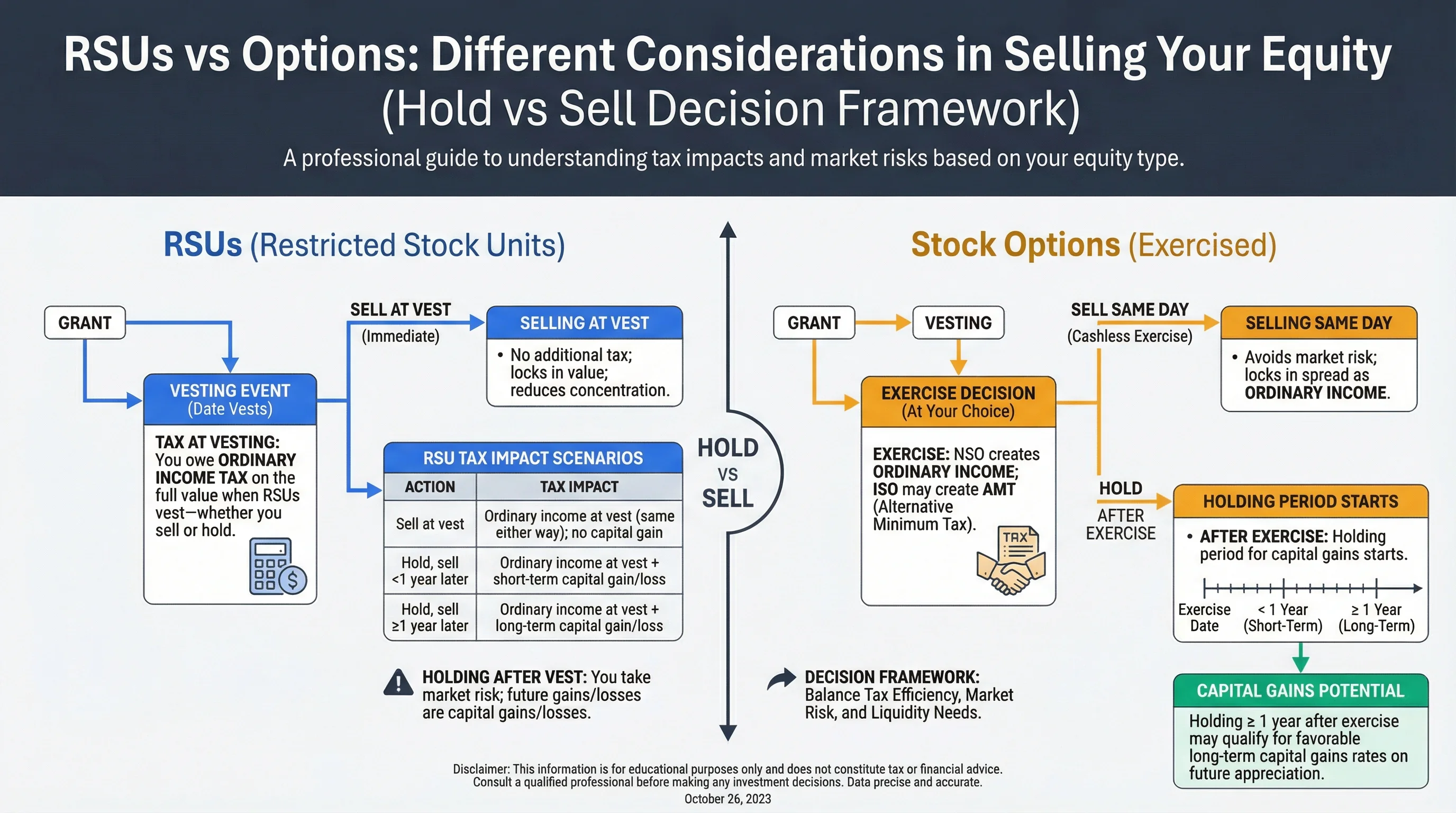

RSUs vs Options: Different Considerations

RSUs

- Tax at vesting: You owe ordinary income tax when RSUs vest—whether you sell or hold

- Selling at vest: No additional tax; locks in value; reduces concentration

- Holding after vest: You take market risk; future gains/losses are capital gains/losses

| Action | Tax Impact |

|---|---|

| Sell at vest | Ordinary income at vest (same either way); no capital gain |

| Hold, sell <1 year later | Ordinary income at vest + short-term capital gain/loss |

| Hold, sell ≥1 year later | Ordinary income at vest + long-term capital gain/loss |

Stock Options (Exercised)

- Exercise: NSO creates ordinary income; ISO may create AMT

- After exercise: Holding period for capital gains starts

- Sell same day: Avoids market risk; locks in spread as ordinary income

Related Guides: RSU Tax Guide, ISO vs NSO.

Common Scenarios

Scenario A: High Concentration, Need to Diversify

Situation: 40% of net worth in company stock; no immediate cash need.

Approach: Sell in tranches over 12–24 months. If some shares are short-term, consider waiting for long-term on a portion. Balance tax efficiency with risk reduction.

Scenario B: Approaching Long-Term Holding

Situation: 8 months since vest; 4 months to long-term; concentration 15%.

Approach: If you can wait 4 months without undue risk, holding for long-term may save 10–17% in tax. If the stock is volatile, consider selling half now, half at long-term.

Scenario C: Need Cash for Down Payment

Situation: Need $50K in 6 months; have $80K in vested RSUs.

Approach: Liquidity need overrides tax optimization. Sell enough to fund the purchase. Consider timing within the year (e.g., sell when you have losses to harvest, or when you're in a lower bracket).

Frequently Asked Questions

Is it better to sell RSUs at vest or hold?

Answer: Tax is the same at vest either way. The decision is about concentration and market risk. If company stock is a large share of your wealth, selling at vest diversifies. If it's small and you're bullish, holding is a calculated risk.

How do I avoid emotional selling (panic or greed)?

Answer: Use a predetermined plan—e.g., "sell 25% per quarter until concentration is under 10%." Stick to the plan regardless of short-term price moves.

What about lockup periods after IPO?

Answer: You can't sell during the lockup (typically 180 days post-IPO). Plan your diversification for when the lockup ends. See our IPO Lockup Periods guide.

Should I sell to fund an option exercise?

Answer: If you believe in the company and have the cash, exercising and holding can make sense. If you need to sell shares to fund the exercise, you're effectively converting paper gains to cash—evaluate whether the exercise is worth the concentration and tax impact.

How do capital gains rates work for high earners?

Answer: Long-term rates are 0%, 15%, or 20% depending on income. Above ~$200K (single), add 3.8% NIIT. Use our Capital Gains Calculator to estimate.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS Publication 550 | Reference | https://www.irs.gov/publications/p550 |

| IRS Topic 409 | Reference | https://www.irs.gov/taxtopics/tc409 |

| SEC Investor.gov | Educational | https://www.investor.gov |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Tax laws vary by jurisdiction and change frequently. Always consult a qualified tax professional (CPA, tax attorney, enrolled agent) before making decisions based on this information. The authors accept no liability for actions taken based on this content.