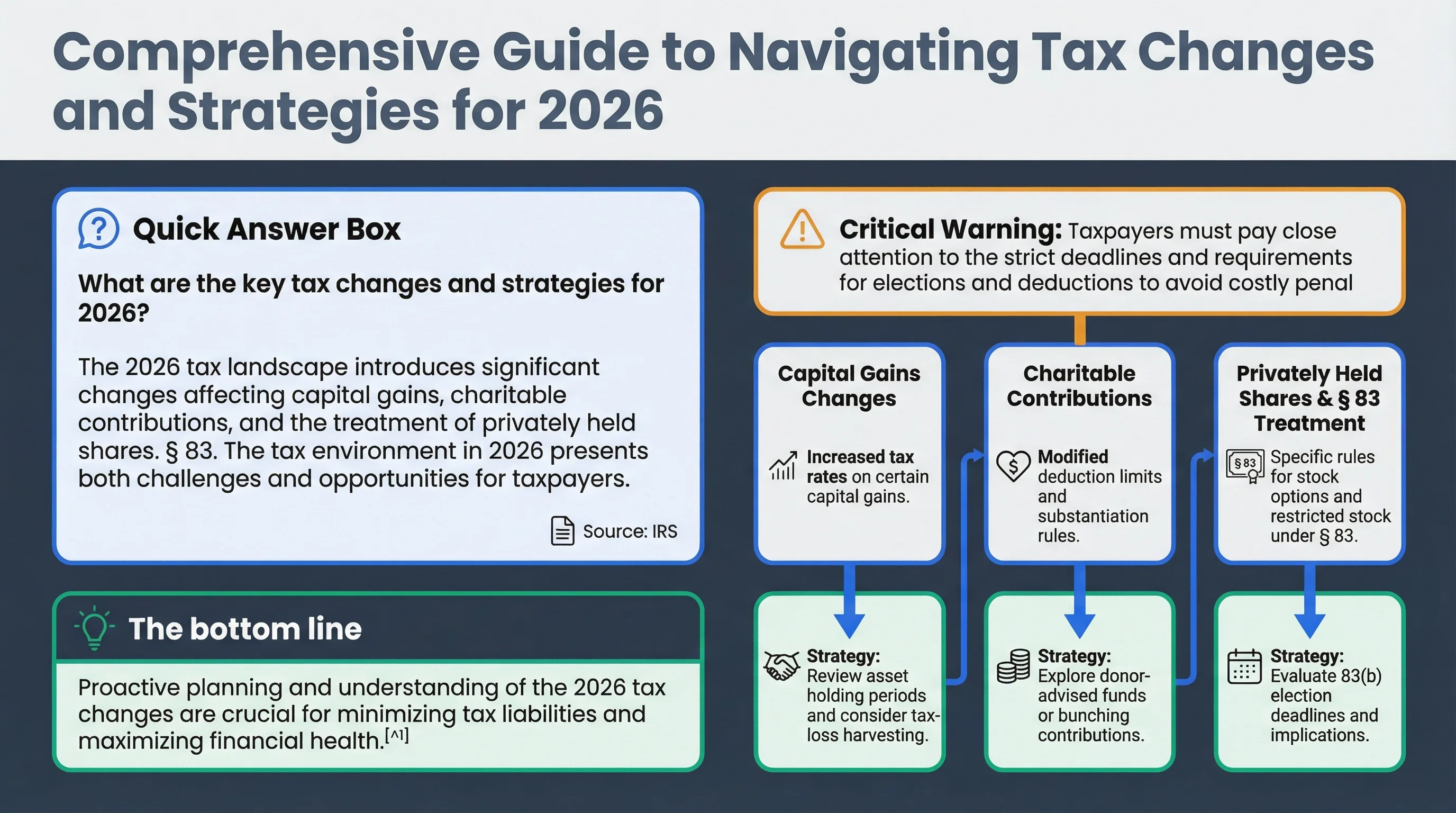

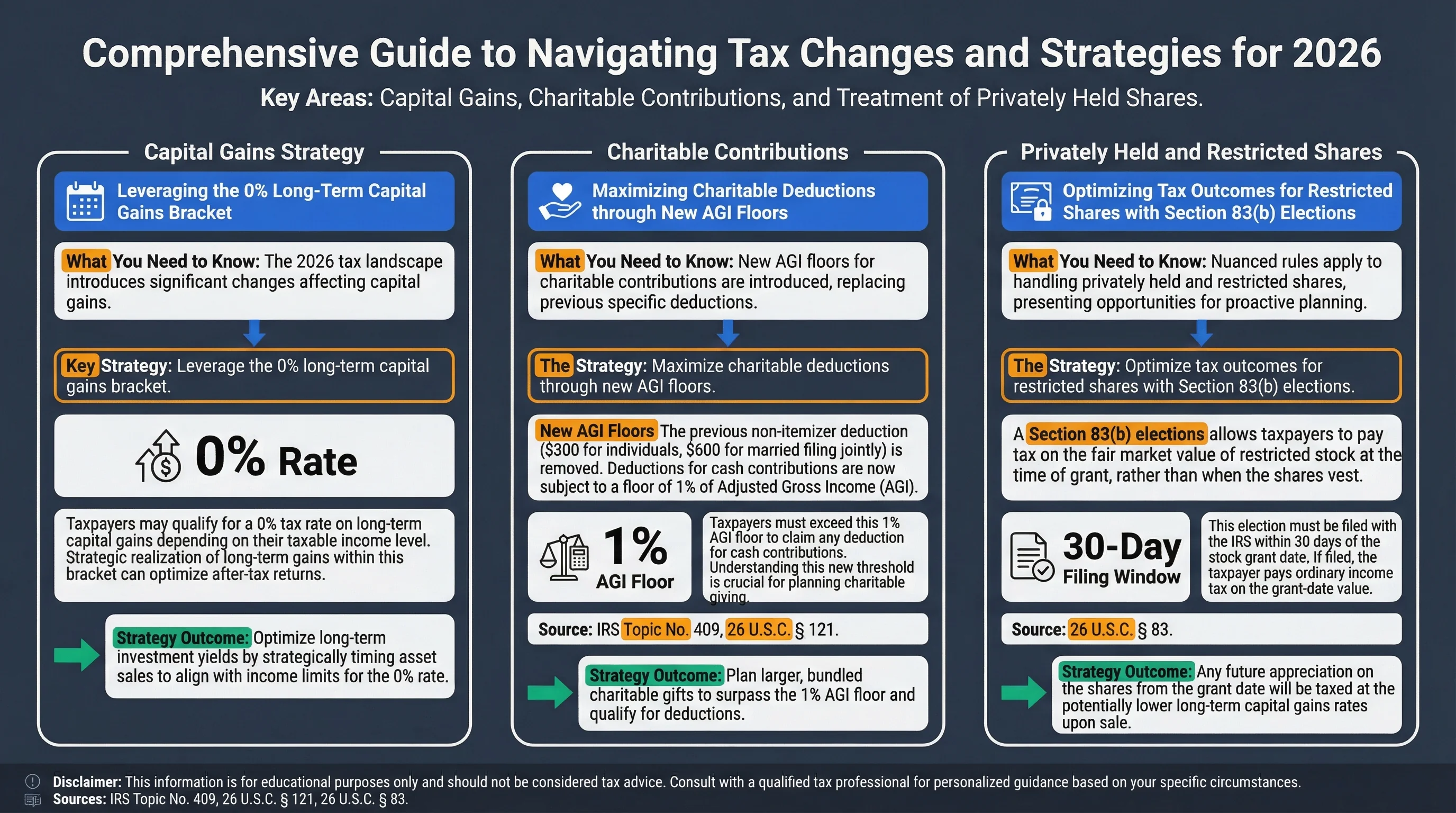

Executive Summary

How can I donate equity shares tax-free?

Donate appreciated equity shares directly to a qualified public charity to deduct the full fair market value (up to 30% of AGI) while avoiding capital gains tax entirely. This strategy can save $50,000+ compared to selling shares and donating cash. The shares must be long-term capital gain property and donated directly—selling first triggers capital gains tax.

Donating appreciated equity shares directly to charity represents one of the most tax-efficient wealth transfer strategies available. By donating shares instead of selling them, you can avoid capital gains tax entirely while deducting the full fair market value—potentially saving $50,000+ in taxes on a $200,000 donation compared to selling and donating cash.

The bottom line: Donating equity shares directly to qualified charities allows you to maximize your charitable impact while minimizing your tax burden. The key is donating the shares directly—selling first triggers capital gains tax and eliminates the benefit.1

Critical Warning: You must donate the shares directly to a qualified public charity. Selling the shares first and then donating cash triggers capital gains tax and eliminates the tax benefit. The charity must be a 501(c)(3) organization, and you must have held the shares for more than one year to qualify for the full FMV deduction.2

The Tax-Free Strategy: How It Works

Direct Donation vs. Sell-and-Donate

When you donate appreciated equity shares directly to a qualified charity, you receive two tax benefits:

- Full Fair Market Value Deduction — Deduct the full FMV of the shares (up to 30% of AGI for long-term capital gain property)

- Zero Capital Gains Tax — Avoid paying capital gains tax on the appreciation

Example Calculation:

| Scenario | Sell Shares, Donate Cash | Donate Shares Directly |

|---|---|---|

| Share Value | $200,000 | $200,000 |

| Cost Basis | $50,000 | $50,000 |

| Capital Gain | $150,000 | $0 (no sale) |

| Capital Gains Tax (20%) | $30,000 | $0 |

| Charitable Deduction | $200,000 | $200,000 |

| Tax Savings (37% bracket) | $74,000 | $74,000 |

| Net Tax Benefit | $44,000 | $74,000 |

| Additional Savings | — | +$30,000 |

Key Insight: By donating shares directly, you save the $30,000 in capital gains tax while still receiving the full $200,000 charitable deduction. This represents a $30,000 additional benefit compared to selling first.

Source: IRS Publication 526 – Charitable Contributions

Requirements for Full FMV Deduction

To qualify for the full fair market value deduction, the donated shares must meet specific criteria:

| Requirement | Specification |

|---|---|

| Holding Period | More than one year (long-term capital gain property) |

| Recipient | Qualified public charity (501(c)(3) organization) |

| Valuation | Fair market value on date of donation |

| Documentation | Written acknowledgment from charity required for donations > $250 |

| AGI Limit | Up to 30% of AGI for long-term capital gain property (carry forward 5 years) |

Source: Internal Revenue Code § 170

Figure 1: Direct donation vs. sell-and-donate comparison — donating shares directly avoids capital gains tax while maximizing charitable deduction benefits.

AGI Limits and Deduction Strategies

2026 AGI Limits for Charitable Contributions

The 2026 tax year introduces new rules for charitable deductions, including a 0.5% AGI floor for itemizers:

| Contribution Type | AGI Limit | AGI Floor (2026) | Carry Forward |

|---|---|---|---|

| Cash to Public Charity | 60% of AGI | 0.5% of AGI | 5 years |

| Long-Term Capital Gain Property | 30% of AGI | 0.5% of AGI | 5 years |

| Appreciated Stock (Public) | 30% of AGI | 0.5% of AGI | 5 years |

| Appreciated Stock (Private) | 30% of AGI* | 0.5% of AGI | 5 years |

*Private company stock requires qualified appraisal for donations > $5,000

Example: A married couple with $200,000 AGI donating $5,000 in appreciated stock can only deduct $4,000 after applying the 0.5% AGI floor ($1,000). The remaining $1,000 can be carried forward for up to 5 years.

Source: IRS Publication 526

Non-Itemizer Deduction (2026)

For the first time in 2026, non-itemizers can deduct up to $1,000 ($2,000 for MFJ) in cash donations to eligible public charities. However, this does not apply to appreciated property donations—you must itemize to claim deductions for donated shares.

Donor-Advised Funds: Flexibility and Timing

What Are Donor-Advised Funds?

Donor-advised funds (DAFs) are charitable giving vehicles that allow you to make a charitable contribution, receive an immediate tax deduction, and then recommend grants to qualified charities over time. This provides flexibility in timing your charitable giving while maximizing tax benefits.

Benefits of Using DAFs for Equity Donations:

| Benefit | Description |

|---|---|

| Immediate Deduction | Receive tax deduction in year of contribution |

| Timing Flexibility | Recommend grants to charities over multiple years |

| Avoid Capital Gains | Donate appreciated shares directly to DAF |

| Simplified Recordkeeping | DAF provider handles charity verification |

| Investment Growth | Assets can grow tax-free while in DAF |

Source: Fidelity Charitable

DAF Contribution Process

- Donate Shares — Transfer appreciated shares directly to DAF (avoiding capital gains tax)

- Receive Deduction — Claim deduction on current year tax return (up to 30% AGI limit)

- Recommend Grants — Direct DAF to make grants to qualified charities over time

- Track Impact — DAF provides consolidated reporting of all charitable activity

Example: Donate $100,000 in appreciated stock to a DAF in 2026, receive $100,000 deduction (subject to AGI limits), then recommend grants to charities in 2027, 2028, and beyond as needed.

Figure 2: Donor-advised fund workflow — maximize tax benefits by donating shares directly to DAF, then recommend grants to charities over time.

Qualified Charitable Distributions (QCDs) for IRAs

QCD Basics

Qualified Charitable Distributions (QCDs) allow individuals aged 70½ or older to contribute up to $111,000 per person directly from their IRAs to qualified charities. The distribution is not counted as taxable income, effectively providing a tax-free way to satisfy Required Minimum Distributions (RMDs).

QCD Requirements:

| Requirement | Specification |

|---|---|

| Age | 70½ or older |

| Source | Traditional IRA or Inherited IRA (not 401(k) or Roth IRA) |

| Recipient | Qualified public charity (not DAF or private foundation) |

| Annual Limit | $111,000 per person (2026) |

| Tax Treatment | Not counted as taxable income |

Source: IRS Publication 590-B

Note: QCDs apply to IRA distributions, not equity shares. However, they represent another tax-efficient charitable giving strategy for retirees with significant IRA balances. For expats considering equity compensation strategies, see our Section 83(b) election guide for expats.

Fair Market Value Valuation

Public Company Stock

For publicly traded stock, the fair market value is the average of the high and low trading prices on the date of donation. This is straightforward to determine using public market data.

Example: Donating 1,000 shares of publicly traded stock on January 15, 2026:

- High price: $50.00

- Low price: $49.50

- Average: $49.75

- FMV Deduction: $49,750

Private Company Stock

Valuing private company stock requires a qualified appraisal for donations exceeding $5,000. The appraisal must be completed within 60 days of the donation and follow IRS guidelines.

Appraisal Requirements:

| Donation Value | Appraisal Required | Form Required |

|---|---|---|

| $250 - $500 | No | Written acknowledgment |

| $500 - $5,000 | No | Written acknowledgment |

| $5,000 - $500,000 | Yes (qualified appraiser) | Form 8283, Section A |

| > $500,000 | Yes (qualified appraiser) | Form 8283, Section B |

Source: IRS Publication 561 – Determining the Value of Donated Property

Figure 3: Fair market value determination — public stock uses market prices, while private stock requires qualified appraisal for larger donations.

Strategic Planning Considerations

Timing Your Donations

Best Practices:

- Donate in High-Income Years — Maximize deduction value when in higher tax brackets

- Bunch Contributions — Combine multiple years of giving into one year to exceed AGI floor

- Consider DAFs — Donate shares to DAF in high-income year, grant to charities over time

- Monitor AGI Limits — Plan contributions to stay within 30% AGI limit for long-term capital gain property

Avoiding Common Mistakes

| Mistake | Consequence | Solution |

|---|---|---|

| Selling shares first | Triggers capital gains tax | Donate shares directly to charity |

| Donating to non-qualified charity | No deduction allowed | Verify 501(c)(3) status |

| Missing documentation | Deduction disallowed | Get written acknowledgment for > $250 |

| Exceeding AGI limits | Lost deduction | Carry forward excess for 5 years |

| Donating short-term property | Only cost basis deductible | Wait until shares are long-term (> 1 year) |

Frequently Asked Questions

Can I donate stock options instead of shares?

Answer: Stock options cannot be donated directly to charity. You must exercise the options first (triggering ordinary income tax), then donate the resulting shares. However, if you hold the shares for more than one year after exercise, you can then donate them and receive the FMV deduction. For guidance on ISO vs NSO tax treatment, see our complete stock options tax guide. If you're concerned about AMT implications from exercising ISOs, consult our AMT planning guide.

Source: IRS Publication 525

What happens if I donate shares worth more than 30% of my AGI?

Answer: You can deduct up to 30% of AGI in the current year, and carry forward the excess for up to 5 years. The carryforward maintains its character as long-term capital gain property, so it's still subject to the 30% AGI limit in future years.

Source: Internal Revenue Code § 170(d)(1)

Can I donate restricted stock or RSUs?

Answer: Yes, but only after the shares have vested and you have taken ownership. You must have held the shares for more than one year to qualify for the full FMV deduction. If you make a Section 83(b) election on restricted stock, the holding period starts from the grant date. For more information on RSU taxation, see our comprehensive RSU tax guide.

Source: IRS Publication 525

Do I need to file Form 8283 for stock donations?

Answer: Yes, if you donate non-cash property (including stock) worth more than $500. For donations between $500 and $5,000, complete Section A. For donations over $5,000, you'll need a qualified appraisal and must complete Section B.

Source: IRS Form 8283 Instructions

Can I donate shares to a private foundation?

Answer: Yes, but the deduction limits are more restrictive. For long-term capital gain property donated to a private foundation, the deduction is limited to your cost basis (not FMV) unless the foundation distributes the property to a public charity within 2.5 months.

Source: IRS Publication 526

What if the charity sells the shares immediately?

Answer: The charity's use of the shares doesn't affect your deduction. As long as you donated long-term capital gain property to a qualified public charity, you receive the full FMV deduction regardless of when or how the charity disposes of the shares.

Source: IRS Publication 526

Can I donate shares from my 401(k) or IRA?

Answer: No, you cannot directly donate shares from a 401(k) or IRA. However, if you're 70½ or older, you can make a Qualified Charitable Distribution (QCD) directly from your IRA to a qualified charity, which provides similar tax benefits.

Source: IRS Publication 590-B

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS Publication 526 | Guidance | https://www.irs.gov/publications/p526 |

| Internal Revenue Code § 170 | Statute | https://www.law.cornell.edu/uscode/text/26/170 |

| IRS Publication 561 | Guidance | https://www.irs.gov/publications/p561 |

| IRS Publication 590-B | Guidance | https://www.irs.gov/publications/p590b |

| Fidelity Charitable - Donating Stock | Reference | https://www.fidelitycharitable.org/giving-philanthropy/ways-to-give/donating-stock.html |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Tax laws vary by jurisdiction and change frequently. Always consult a qualified tax professional (CPA, tax attorney, enrolled agent) before making decisions based on this information. The authors accept no liability for actions taken based on this content.

Footnotes

-

IRS Publication 526 provides comprehensive guidance on charitable contributions, including the tax treatment of donated property. ↩

-

Internal Revenue Code § 170 outlines the deduction limits and requirements for charitable contributions, including the distinction between cash and property donations. ↩