Executive Summary

How are employee stock purchase plans (ESPPs) taxed in Canada?

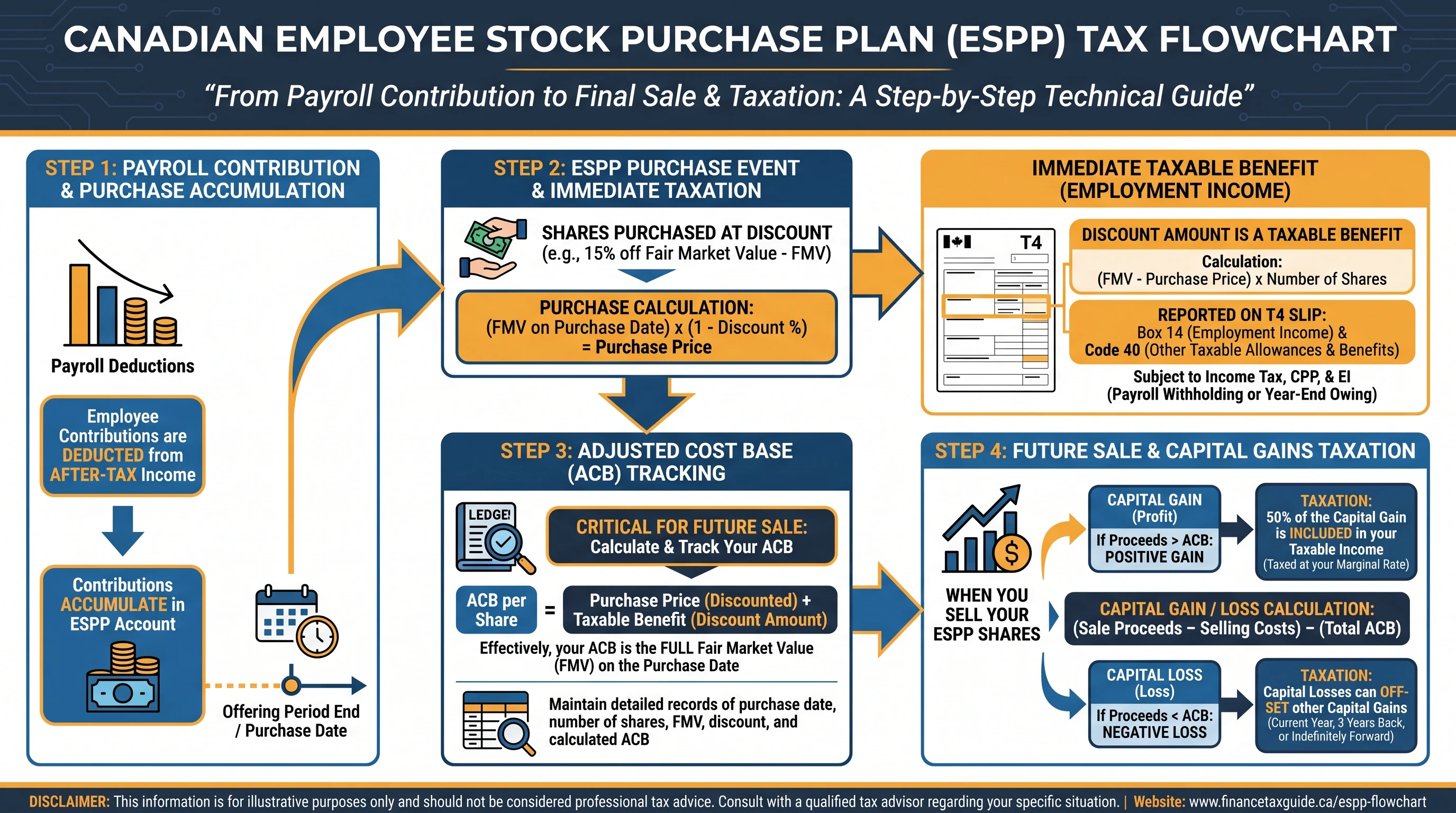

In typical public-company ESPPs, the discount on shares (fair market value at acquisition minus what you pay) is usually taxed as employment income around the time you acquire the shares. Your adjusted cost base is increased by that benefit so you are not taxed again on the same amount when you sell. A later sale generally produces a capital gain or loss based on proceeds minus ACB.

Employee stock purchase plans are everywhere in tech: payroll contributions, an offering period, then shares bought at a discount. If you are used to U.S. IRC Section 423 stories (qualifying disposition, Form 3922, and taxes often layered at sale), Canada usually front-loads more of the story into employment income at acquisition, with capital gains treated as a second chapter when you dispose of the shares. That difference matters for cash flow, for comparing notes with U.S. coworkers, and for reading your T4 without surprises. This guide translates the core Canadian framework, points to official CRA pages, and links to related VestingStrategy coverage for cross-border employees and general ESPP mechanics.

The bottom line: Map your plan to an employment-benefit event at acquisition (most common for large public tech employers), rebuild ACB using the taxed benefit, then report Schedule 3 gains on sale—your slips and brokerage statements should tell the same story.1

Critical Warning: Labels like "qualified ESPP" in a U.S. parent plan document do not automatically import U.S. tax timing into Canada. Your Canadian T4/RL-1 and CRA rules drive Canadian tax, not your colleague's W-2.

Where ESPPs Sit in Canadian Tax Law

Canadian tax starts with the Income Tax Act (ITA). ESPPs usually touch:

- Employment income and benefits (for example ITA section 6) when you receive a benefit from employment.

- Rules for security options and agreements to issue securities (ITA section 7) when the plan looks like options or deferred issuance rather than a simple open-market purchase—but many payroll ESPPs are not the same as classic incentive stock option grants.

- Capital gains and ACB (for example ITA sections 39 and 53) when you sell shares that you hold as capital property.

The CRA consolidates much of its plain-language employer guidance under Security options and the broader employers' publication Taxable Benefits and Allowances (T4130). Those pages are the right first stop when your payroll team points you to "employment benefit" language.

| Topic | What employees should verify | Why it matters |

|---|---|---|

| Plan type | Open-market purchase vs. formula price vs. parent-country "qualified" wording | Determines whether section 7-style analysis ever applies |

| Acquisition date | Date shares are actually acquired | Drives the taxation year of the employment benefit |

| FMV method | How your employer prices FMV for the benefit | Affects dollars in Box 14 / Box 38 style reporting |

| Share issuer | Canadian listed vs. foreign issuer | Currency conversion and forms like T1135 may enter |

ESPPs vs. stock options (high level)

Many employees conflate ESPPs with stock options. Statutory stock-option relief and holding-period logic under the ITA can be very different from a purchase discount delivered through payroll. If your employer grants options, start with our Canada stock options and RSU guide; if your program is a purchase plan, stay in this article first, then compare cash-flow timing with our U.S. ESPP taxation overview.

The Employment Benefit and When It Is Taxed

The central economic idea is simple: if your employer lets you buy $100 stock for $85, the $15 per share slice is usually economic upside from employment, not luck. Canada generally treats that upside as taxable—often as an employment benefit included in income in the year you acquire the securities, for non-CCPC public employers (subject to plan facts).

For Canadian-controlled private corporations (CCPCs), ITA section 7 contains deferral mechanics for certain security acquisitions that do not apply the same way to every public-company ESPP. If you are at an early-stage CCPC, ask whether your plan is intentionally structured for deferral or taxed immediately like a large public filer.

| Concept | Plain English | Common pitfall |

|---|---|---|

| FMV at purchase | Price the CRA accepts as fair market value when you acquire | Using the wrong exchange rate day for USD parents |

| Purchase price | What you paid per share after payroll deductions | Ignoring employer matching shares as a separate benefit |

| Benefit inclusion | Usually (FMV − price) × shares for a classic discount | Assuming "no tax" because payroll did not withhold visibly |

Worked example (illustrative): You acquire 200 shares. FMV is $50 CAD and you pay $42.50 per share. The discount is $7.50/share, so the employment benefit is 200 × 7.50 = $1,500 dollars of employment income before considering any sale.

Adjusted Cost Base and Tax on Sale

After you pay tax on the employment benefit, Canada generally adds that benefit to your cost so the same discount is not taxed again as full capital appreciation. Conceptually:

ACB per share ≈ cash paid per share + (employment benefit per share included in income)

On sale, proceeds − ACB = capital gain (or loss), and the capital gains inclusion rate applies to the taxable portion (verify current law for the year of sale—the 66.67% hike proposed in Budget 2024 was cancelled in March 2025; see Canada capital gains tax hike & stock options).

| Event | Typical tax character | Slip hints |

|---|---|---|

| Acquisition | Employment income (benefit) | T4 Boxes 14 / 38-style reporting varies by payroll setup |

| Later sale | Capital gain or loss | Schedule 3 of the T1; keep brokerage confirmations |

If you also hold U.S. equity, read Canada–U.S. cross-border equity before assuming a single-country story for acquisition and sale.

T4, RL-1, Payroll Withholding, and Schedules

Employers use payroll to withhold income tax and social contributions on taxable benefits where required. CRA's payroll guidance (including special payments charts) explains when CPP, EI, and Quebec contributions apply—your pay stub and T4 are the operational truth.

Quebec residents also receive RL-1 information; boxes differ from federal T4 labels, but the economic income should reconcile when you file TP-1.

| Document | What to check | Action if wrong |

|---|---|---|

| T4 | Employment income totals and benefit boxes | Payroll correction before filing deadline |

| RL-1 (QC) | Mirrored employment and benefit amounts | Request employer reissue |

| Trade confirmations | Share count, price, currency | Evidence for ACB audits |

| T1135 | Foreign property thresholds | File if required; see CRA criteria |

Provincial Layers and Quebec Specifics

Federal inclusion flows into provincial taxable income. Ontario, British Columbia, and other provinces piggyback on the federal return; Quebec uses a separate provincial return with RL-1 sourcing. Marginal rates change the cash you should set aside even when the legal structure of the benefit matches a colleague in another province.

Cross-Border Tech Employees (Orientation Only)

If you are a Canadian resident participating in a U.S. parent ESPP, you may face FX conversion, foreign-property reporting, and treaty questions that are not visible on a single T4 line. Use this article for the Canadian baseline, then continue with international equity tax planning and the Canada–U.S. cross-border equity guide. The comparison to RSU vs ESPP helps when your employer gives you both vehicles.

Planning Checklist Before You Enroll or Sell

- Read the plan document for purchase mechanics, holding restrictions, and whether the employer asserts option-like treatment.

- Model cash for benefit inclusion in the acquisition year—not only for capital gains later.

- Track ACB in your spreadsheet even if the brokerage reflects most of it; employers and brokers can disagree after corporate actions.

- Coordinate RRSP/TFSA decisions with contribution room; employer-directed purchases can still trigger T4 income depending on design (verify with your administrator).

- Export trade logs if you move brokers—historical FMV evidence matters in audits.

Year-End Checklist for Canadian ESPP Participants

Before you file, line up four artifacts: the annual T4 (and RL-1 if applicable), the ESPP statement from your employer showing per-purchase FMV, the brokerage year-end gain/loss export, and your FX worksheet if purchases were priced in USD. Check that the employment benefit on the T4 matches your own calculation of shares × (FMV − price) for each purchase window; payroll systems sometimes lag corporate actions for a year. For sales, recompute ACB from cash paid + taxed benefit and compare to the book value your broker displays—discrepancies often trace to transfers between broker-dealers. If you participated in a parent-country plan, ask whether Canadian payroll grossed up foreign employer costs; that gross-up is usually additional employment income. Keep PDFs of each enrolment election and change form—auditors routinely ask for evidence of what you agreed to, not only what a website showed.

Is my Canadian ESPP taxed like a U.S. "qualified ESPP"?

Answer: Not automatically. U.S. rules under the Internal Revenue Code can defer or split the taxation of discounts in ways that differ from the typical Canadian benefit-at-acquisition pattern. Your Canadian return follows ITA concepts and your Canadian slips.

Source: CRA — Security options

Does the 50% stock-option deduction apply to my ESPP discount?

Answer: Often no. The deduction is specific to statutory stock option facts. A payroll purchase discount may be fully included as ordinary employment income without that relief.

Source: Income Tax Act — Justice Laws (consult counsel for plan-specific analysis)

What is my ACB if payroll shows a taxable benefit?

Answer: Generally your cash cost plus the included benefit per share, so the discount is not taxed again as gain when you sell.

Source: CRA — Employers' guide (T4130)

Do I pay CPP/EI on the ESPP benefit?

Answer: Frequently yes for amounts treated as pensionable or insurable employment income; exact payroll treatment follows CRA charts and your employer's configuration.

Source: CRA payroll guidance

I moved provinces mid-year—who taxes the benefit?

Answer: Provincial allocation depends on residency and sourcing rules on your return; the T4 income still enters federal net income, then provincial schedules apply.

Source: CRA — T4130

Can I contribute ESPP shares directly to my TFSA without a sale?

Answer: In-kind contributions have tax nuance (deemed dispositions may arise). Most employees sell then contribute cash unless a planner structures otherwise.

Source: CRA — TFSA information

What records should I keep?

Answer: Keep T4/RL-1, plan enrollments, payroll deductions, trade confirmations, and FX worksheets for foreign parents.

Source: CRA — Security options

Where can I compare ESPPs to RSUs in one place?

Answer: Start with RSU vs ESPP—RSUs usually create wage income at vest, while ESPPs center on purchase economics.

Source: VestingStrategy guide index

How do I sanity-check my T4 against brokerage cost basis?

Answer: Build a ledger: for each acquisition, record shares, CAD FMV, cash paid, benefit per share, and running ACB. After a corporate action (split, merger), restate prior rows before trusting broker imports.

Source: CRA — Security options

What if my employer reports in USD but I file in CAD?

Answer: Convert amounts using Bank of Canada rates for the relevant dates; keep a simple rate table with sources attached to your tax folder. Large U.S. parents often generate USD FMV numbers even for Canadian payroll.

Source: CRA exchange rate guidance

When should I involve a cross-border specialist?

Answer: Engage one when you have U.S. citizenship or green card status, days in Canada below substantive residency tests, corporate recharges between parents and subsidiaries, or options and ESPPs from different issuers in the same year. The Canadian employment benefit still needs correct FX and foreign-information reporting even if your dashboard looks "American."

Source: CRA — International tax

Coordinating T4 Income with Schedule 3 (Worked Skeleton)

Assume your T4 shows $4,000 of ESPP employment benefit for the year and you sell all related shares later for $14,000 cash after a prior $9,500 out-of-pocket payroll total for those same shares (numbers illustrative):

Employment benefit (already on T4) = $4,000 (ordinary income)

Cash paid for shares = $9,500

ACB for sale ≈ cash + benefit = $13,500

Capital gain ≈ $14,000 − $13,500 = $500

Only half (verify for your tax year) of the capital gain may be taxable at ordinary inclusion rates; the $4,000 is not taxed again as capital gain when ACB is correct. This skeleton is why keeping T4 + confirmations together matters.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| CRA — Security options | Government | canada.ca |

| CRA — Taxable benefits (T4130) | Government | canada.ca |

| Income Tax Act | Statute | Justice Laws |

Figure 1: High-level flow from ESPP enrollment through employment benefit inclusion and eventual disposition, for orientation alongside your official slips.

Research note: Topic selection followed VestingStrategy's CCO API (npm run cco:recommend). Perplexity research notes are at docs/research/RESEARCH-CCO-ESPP-TAX-CANADA-COMPLETE-GUIDE-PERPLEXITY-BRUT.md.

Footnotes

-

Employment benefit timing, ACB additions, and provincial reporting are fact-specific; verify against your T4/RL-1 and CRA publications for the taxation year. ↩