Executive Summary

I’m a US citizen in Toronto with RSUs—do I only file Canadian taxes?

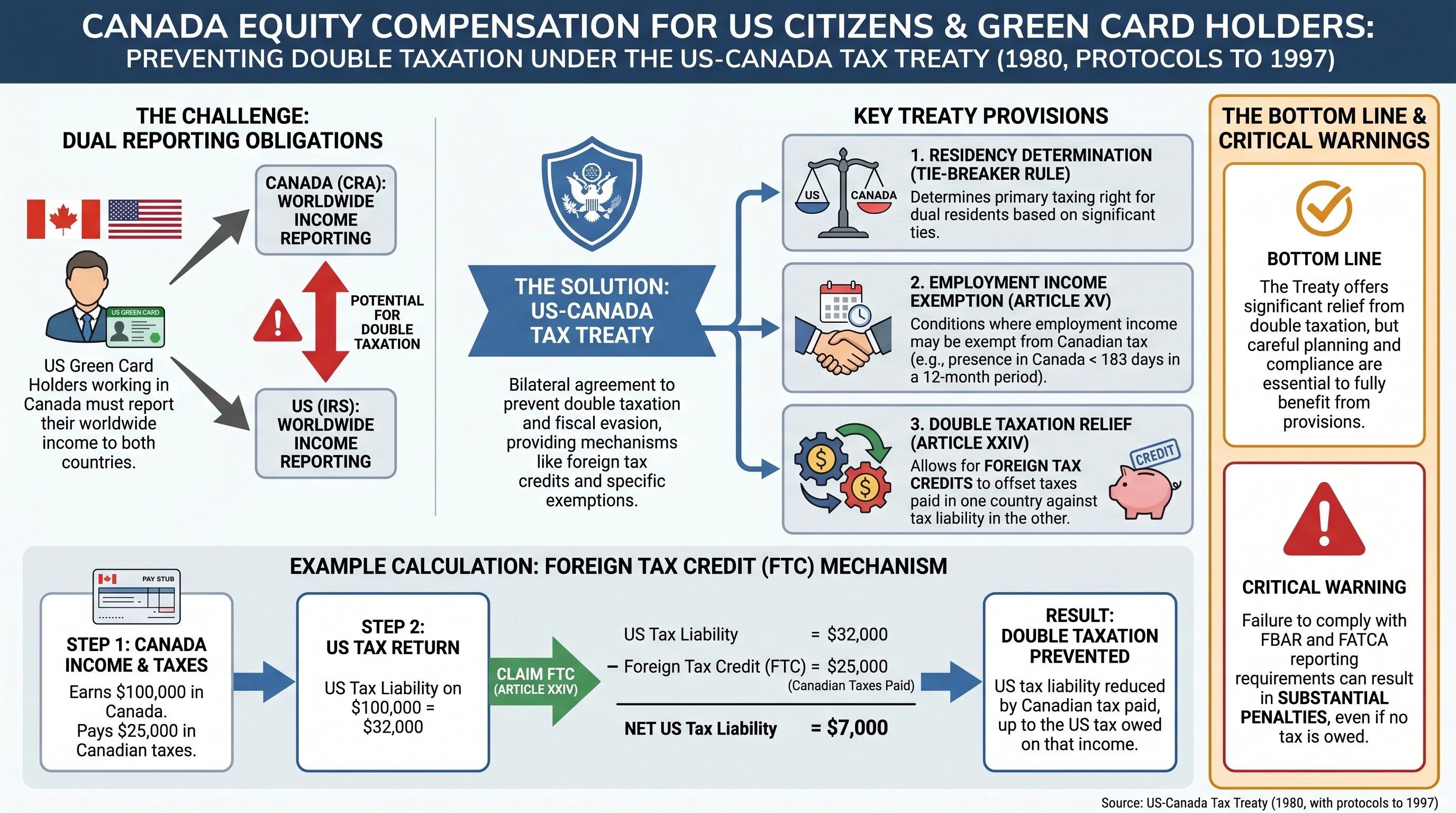

Usually no. US citizens generally must file a US federal return reporting worldwide income. Canada may tax employment equity based on Canadian rules and reporting slips (commonly T4, and RL-1 in Quebec). You often coordinate the two systems with foreign tax credits and careful sourcing—not by ignoring either side.

I’m a US green card holder living in Canada—am I treated like a US citizen?

Not identically, but overlap is common. Green card holders are generally US resident aliens for US tax purposes and must file US returns on worldwide income unless they have a specific, validated nonresident claim under US law and treaty tie-breaker rules. This is a planning-sensitive area—document facts and get cross-border advice before assuming you can file as a nonresident.

Canada is a top destination for US tech workers, but equity is where cross-border tax stops being “just a filing exercise.” A Canadian payroll team may tax and report RSU or option income on T4 boxes while a US parent payroll still issues W-2 equity codes for overlapping periods. Meanwhile, US law may still require worldwide reporting, and information returns may apply even when your income tax is coordinated cleanly.

The bottom line: Build a per-grant ledger (dates, FMV, shares, payroll slips, broker statements) and reconcile Canada first, then US sourcing and credits—not the other way around. Start from our Canada stock option & RSU guide and Canada–US cross-border equity guide, then use this article for the US-person overlay (citizenship, green cards, common US forms).1

Critical warning: FBAR and FATCA (Form 8938) are separate regimes with separate thresholds. Missing them can create penalty exposure even when your income tax math is fine. If you are new to cross-border compliance, read slowly and involve a CPA who does both sides regularly.

US persons in Canada often run two tax systems at once: Canadian wage reporting on equity plus US worldwide taxation, with foreign tax credits and information returns layered on top—educational only, not individualized advice.

Who this guide is for (and who should skip it)

This article is written for:

- US citizens resident in Canada (short-term assignees or long-term emigrants)

- US green card holders resident in Canada (or commuting cross-border)

- Employees with RSUs, stock options, or similar payroll-reported equity

It is not a substitute for:

- A Canadian CPA who can interpret your T4/RL-1 and provincial rates

- A US CPA who can model Form 1116, ISO AMT, and any streamlined disclosure history you may already have

Concepts that confuse people immediately

Citizenship vs treaty residency vs “where I pay most tax”

Canada decides many Canadian obligations using residency and ties. The US taxes US citizens on worldwide income regardless of where you live. That basic fact is why “I pay tax in Canada” does not end the US story for citizens.

Green card holders are typically US resident aliens and generally file Form 1040 on worldwide income. If you live in Canada full-time, you may encounter treaty tie-breaker analysis and highly fact-specific claims about US residency cessation—this is not something to infer from a blog chart. If that is your profile, stop reading “quick answers” on the internet and get a professional who will document your position.

Employment income vs investment income (equity is not “one thing”)

For many employees, equity is employment income at a specific event (vest, exercise, settlement—depending on instrument and country). But the US may still need a capital gain/loss story on later share sales, and ISOs can add AMT even when regular tax is deferred.

If you have ISOs, pair this guide with AMT planning for stock options and ISO qualifying vs disqualifying disposition.

Canadian side: what typically shows up on slips (high level)

Canadian reporting is slip-driven. For equity, employers commonly use:

| Slip | What it often represents | Why US persons still care |

|---|---|---|

| T4 | Employment income and withheld tax; equity may appear in employment income and related boxes depending on plan mechanics | You need the same facts the CRA received |

| RL-1 (Quebec) | Quebec-specific employment and withholding | A second provincial return layer |

Do not treat payroll withholding as your final tax. Large equity events can still create balances due or refunds after filing—similar in spirit to US supplemental withholding issues discussed in RSU withholding gaps.

For a domestic Canada baseline (before the US overlay), use:

US side: worldwide income, common coordination tools

Form 1116 foreign tax credit (conceptual)

Form 1116 is the usual workhorse to reduce double taxation on foreign-source income taxed by both countries, subject to limitations and basket rules. Equity compensation often lands in the general limitation income basket, but your facts matter.

Why credits fail “intuitively” sometimes:

- Timing mismatch: the income is recognized in different years between countries

- Sourcing mismatch: US and Canada disagree on how much income is US vs Canadian

- Rate mismatch: credit is limited to US tax attributable to that foreign-source income

If you are new to FTC planning, read IRS materials carefully and model scenarios—this is not something to optimize from memory after one vest.

When a treaty article matters (and when it does not)

The US–Canada tax treaty can matter for allocation of taxing rights and relief, but it is not a blanket “don’t file” pass. Treaty analysis is especially common for:

- Cross-border commuters and partial-year residents

- Dual residency situations (more common for non-citizens than for US citizens)

Official treaty text (PDF) is published by the IRS: US–Canada tax treaty (IRS PDF).

RSUs: a practical reconciliation pattern

RSUs are the cleanest teaching example because many employers tax them as employment income at settlement/vest for Canadian purposes, while US reporting still needs correct US dollar translation and sourcing.

Build the RSU ledger (minimum viable)

For each vest/settlement, track:

- Date and share count

- FMV per share used by payroll (CAD) and how FX was applied

- Canadian income tax withheld (T4/RL-1)

- CPP/EI implications (cash-flow, not always parallel to US FICA)

- Broker sale if any shares sold for taxes (may create a separate gain/loss)

Then ask: what did the US return think happened in the same window? If you also have a US W-2, reconcile duplicates carefully—many “double tax” panics are actually double reporting mistakes.

Stock options: Canada timing vs US ISO/NSO complexity

Canadian option taxation can differ materially depending on employer type (for example, CCPC vs public company contexts). The CRA’s employer-facing overview is a useful anchor: CRA — stock options.

On the US side, remember:

- NSO spread at exercise is often W-2 wages with familiar payroll tax mechanics

- ISO can trigger AMT at exercise even when regular tax is not due at exercise

If you exercise while resident in Canada, you may have no Canadian parallel to US AMT—cash planning matters.

Information returns: FBAR and Form 8938 (do not round thresholds)

| Topic | FBAR (FinCEN Form 114) | FATCA (IRS Form 8938) |

|---|---|---|

| What it targets | Foreign financial accounts | Specified foreign financial assets (broader categories than FBAR in some ways) |

| Threshold intuition | Aggregate >$10,000 at any point (FBAR framing) | Higher thresholds that depend on filing status and US/abroad residence facts |

| Why equity people hit this | RSU cash sitting in Canadian accounts; multi-currency payroll | Foreign brokerage holdings; foreign pension-like accounts (facts matter) |

Use official FinCEN/IRS guidance for thresholds and definitions—do not rely on summarized charts alone.

Relocation year: partial-year residency is a project

If you moved mid-year, expect:

- Partial-year Canadian residency and slip oddities

- Partial-year US sourcing discussions

- A higher chance of needing a treaty disclosure position on the US return (Form 8833 facts)

Use relocating with equity as the movement checklist, then return here for the Canada/US person overlay.

Planning checklist (actionable, not exhaustive)

- Collect all slips: T4, RL-1 (if Quebec), W-2 if US payroll still runs, and any broker tax forms.

- Per-grant timeline: grant, vest, exercise, sale—each may matter differently in each country.

- FX documentation: know which rates your employer used and whether you must translate for US reporting.

- Model US tax with and without FTC before you spend the proceeds.

- Information returns: accounts and assets, not just income tax.

- If ISOs exist: model AMT and disqualifying disposition scenarios before exercising.

One sentence on state taxes (US)

If you recently lived in a US state with aggressive sourcing (for example, California), do not assume moving to Canada automatically ends state reporting for prior-year equity or trailing obligations. State rules are not harmonized with federal foreign tax credits the way many taxpayers expect.

Frequently Asked Questions

Do US citizens living in Canada still file US taxes if they pay Canadian tax?

Answer: Generally yes. US citizens typically must file US federal income tax returns reporting worldwide income. Canadian taxes paid may reduce double taxation via mechanisms like the foreign tax credit, but “I paid Canada” does not automatically end US filing.

Source: IRS — International taxpayers

Are green card holders taxed like US citizens?

Answer: Green card holders are usually US resident aliens and generally have US worldwide filing obligations similar to US residents. Living in Canada can create complex residency and treaty issues that should be analyzed professionally—do not assume you can simply file as a US nonresident without a documented position.

Source: IRS — Taxation of resident aliens

How do RSUs usually show up for Canadian tax?

Answer: Employers generally report employment benefits through payroll reporting slips (T4, and RL-1 in Quebec). The precise boxes and timing depend on plan design and whether amounts are cash-settled or share-settled.

Source: CRA payroll benefits — stock options overview

What is Form 1116 used for?

Answer: Form 1116 is used to claim the foreign tax credit, which can reduce US tax on foreign-source income when you also paid foreign income taxes, subject to limitations.

Source: IRS — About Form 1116

Is FBAR the same as FATCA Form 8938?

Answer: No. They overlap conceptually but have different rules, thresholds, and agencies. You might need one, both, or neither—determine based on official thresholds and your accounts/assets.

Source: IRS — Comparison of Form 8938 and FBAR requirements

Can the US–Canada treaty eliminate Canadian tax on my salary?

Answer: Sometimes Article XV style limitations can apply to employment income for specific short presence facts and employer residence conditions—but this is famously fact-specific. Do not treat “183 days” as a universal safe harbor without checking treaty conditions and your employment contract.

Source: US–Canada tax treaty (PDF)

Do I need a US CPA and a Canadian CPA?

Answer: Often yes for active equity compensation, Quebec returns, or ISO AMT. The expensive mistake is optimizing one country in isolation and discovering a timing mismatch in the other.

Source: professional standard practice (no single IRS/CRA pamphlet replaces this)

What if my employer withheld too little for US taxes while I live in Canada?

Answer: You may need Form W-4 adjustments on any US payroll, estimated tax payments, or both. Equity can spike income unevenly across quarters—see estimated tax payments.

Source: IRS — Estimated tax

How should I think about Canadian CPP/EI vs US Social Security/Medicare?

Answer: They are different systems; totalization agreements may matter for some workers. Payroll line items should be reviewed alongside your cross-border CPA rather than assumed to “net out.”

Source: SSA — International programs

What internal guides should I read next on this site?

Answer: Read Canada–US cross-border equity tax for mechanics, then Canada stock option & RSU tax guide for domestic baseline, and international equity tax planning for the broader framework.

Source: VestingStrategy guide index

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| US–Canada income tax treaty (consolidated text, IRS PDF) | Treaty | https://www.irs.gov/pub/irs-trty/canada.pdf |

| CRA — Stock options (payroll benefits overview) | Government | https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll/benefits-allowances/benefits/stock-options.html |

| IRS — Form 1116 (foreign tax credit) | Government | https://www.irs.gov/forms-pubs/about-form-1116 |

| IRS — Form 8938 vs FBAR | Government | https://www.irs.gov/businesses/comparison-of-form-8938-and-fbar-requirements |

Disclaimer: This guide is for general education only and is not individualized tax, legal, or investment advice. Tax rules change, and your facts (employer plan design, province, payroll location, citizenship, residency elections, and treaty positions) may differ. Consult a qualified cross-border tax professional before making decisions.

Footnotes

-

US persons may use foreign tax credits and treaty positions, but compliance requires correct sourcing and timing—not treaty slogans alone. ↩