Executive Summary

Why do I owe tax on RSUs even though my employer withheld?

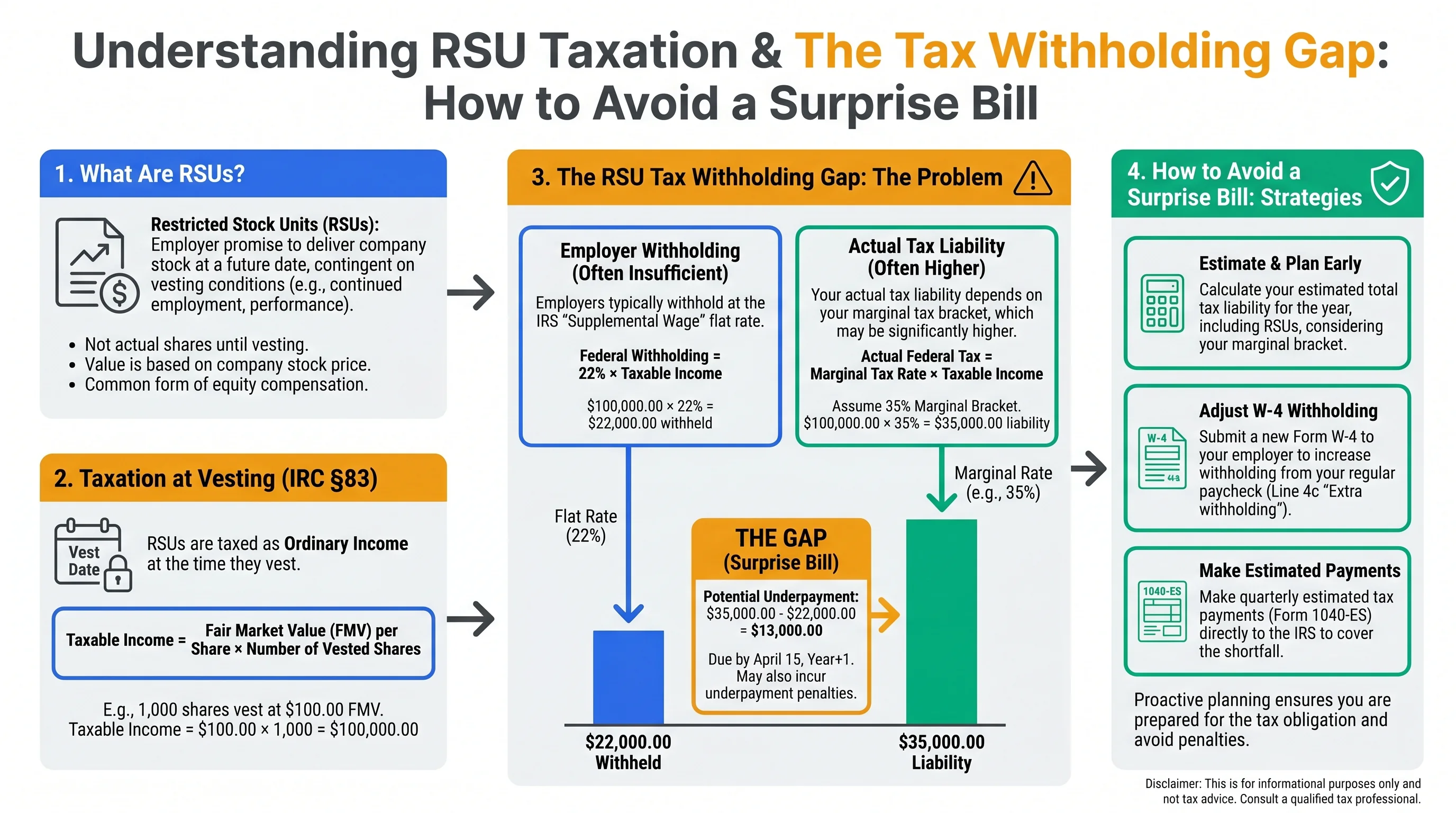

RSU vesting is taxed as wages, and your employer must withhold—but federal income tax withholding on supplemental payments often uses a flat rate (commonly 22% for supplemental wages under $1 million when paid separately using the optional flat rate method). If your actual marginal tax rate is higher, withholding may not cover the full liability, so you still owe at filing unless you proactively increase withholding or make estimated tax payments.

If you have ever opened your paystub on a vest date and thought, “They already took taxes—why did I still owe thousands in April?” you are not imagining it. Restricted Stock Units (RSUs) are intentionally taxed like a bonus-like wage event at vest, and the withholding mechanics are not guaranteed to match your marginal tax bracket.

This article explains the withholding gap in plain language, when the 22% supplemental rate shows up, what employers can (and cannot) do, and the most practical ways employees close the hole before underpayment penalties appear. For adjacent reading, compare RSU and option withholding: why 22% may not be enough and RSU sell-to-cover withholding explained.

The bottom line: Treat RSU vesting as a cash-flow planning event, not only a “portfolio” event—your Form 1040 result is driven by total tax minus total withholding and estimates, not by whether vesting felt taxed at the time.1

Critical Warning: Payroll systems vary. Some employers use aggregate withholding (which can track your W-4 more closely) for certain payments. Others use flat supplemental withholding for equity settlements. Do not assume your employer’s method matches your friend’s employer.2

Figure 1: The core mismatch—flat withholding vs progressive tax rates.

RSU Income Is Wages (That Is the Root of the Confusion)

What happens at vest?

When RSUs vest, you generally have compensation income equal to the fair market value of shares delivered (unless a rare deferral arrangement applies). That inclusion is wages for tax purposes and is commonly analyzed under IRC Section 83.3

Employees sometimes mentally model RSUs like “stock,” but payroll treats the vest as cash-like wage income—because you received something valuable as pay.

Why withholding can feel “wrong”

Withholding is a payroll approximation. It is designed to collect tax during the year, but supplemental pay rules can make the approximation too low for high earners.

Pair this section with first-year RSU tax survival guide if you are new to equity.

Do not confuse effective tax rate with marginal tax rate. A flat 22% withholding can look “reasonable” if you mentally average your whole return, but RSU income often lands in your top federal bracket for the year. The mismatch is between flat withholding on a big vest and progressive tax on total income—not a mystery IRS rule.

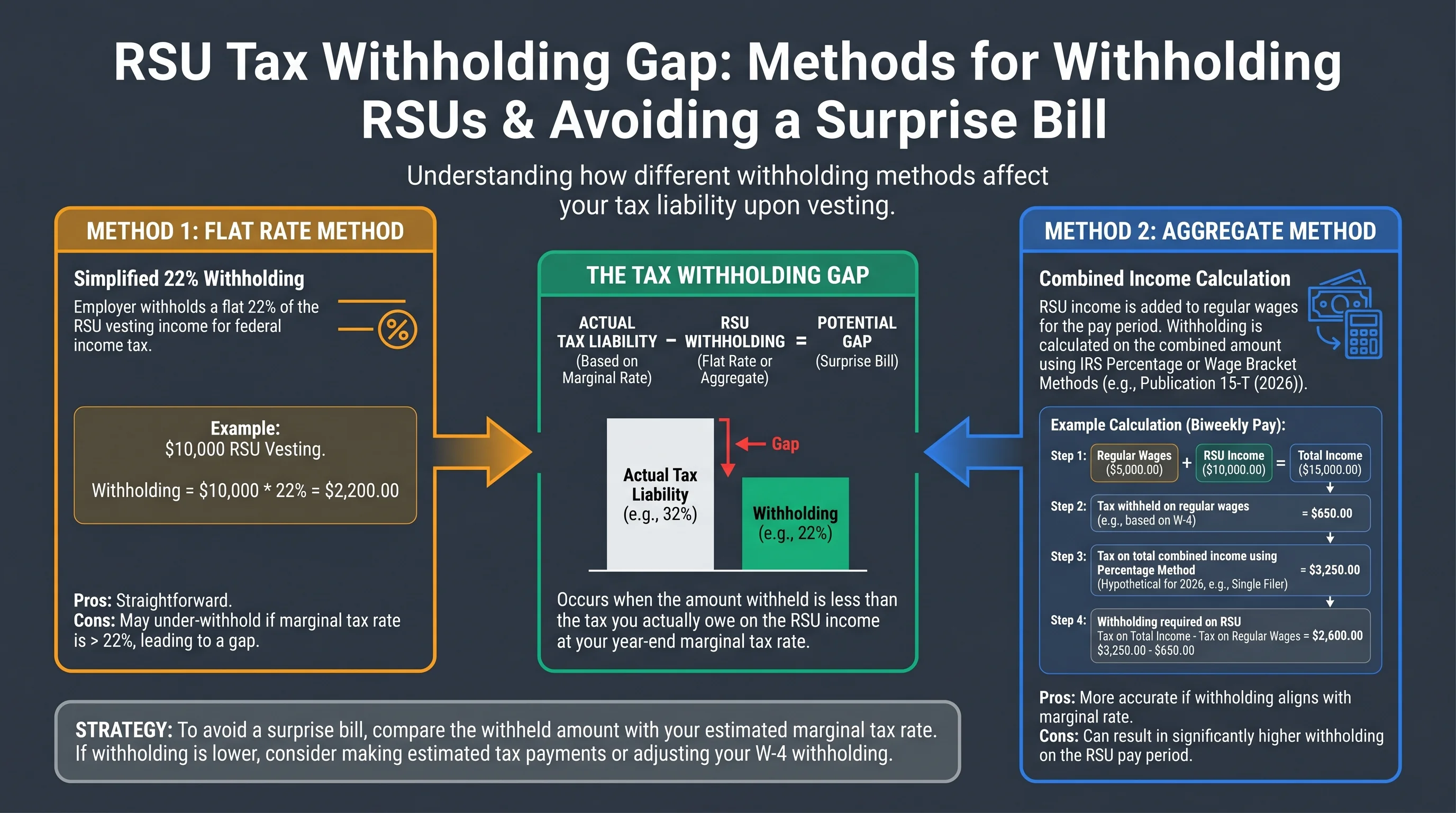

Supplemental Wages: The 22% and 37% Story Everyone Quotes

IRS guidance for employers describes supplemental wages and methods for withholding on them. A common pattern for large tech employers is to treat RSU settlement as supplemental wages.

For federal income tax withholding, employers may be required to use 37% on supplemental wage payments above $1 million during the calendar year (for that employee). For amounts up to $1 million, employers may have options that include a flat 22% rate for the supplemental payment when certain conditions are met—see IRS Publication 15 for the precise rules, exceptions, and when the aggregate method must be used.4

| Concept | Employee-facing meaning |

|---|---|

| Supplemental wages | Compensation paid outside regular salary, often including bonuses and equity settlements (employer-dependent) |

| Optional flat 22% | A simplified withholding rate that may not match your marginal bracket |

| $1M threshold | Different withholding rules can apply once supplemental wages exceed $1 million in a calendar year |

A numeric illustration (single vest)

Assume your employer withholds 22% federal income tax on a $120,000 RSU vest (purely illustrative payroll behavior):

Federal income tax withheld (illustrative flat supplemental) = $120,000 × 22% = $26,400

If your marginal federal income tax rate on that income is 32%, your “true” federal income tax attributable to that increment might be closer to:

$120,000 × 32% = $38,400

Illustrative gap ≈ $38,400 − $26,400 = $12,000

This gap does not include state tax, Additional Medicare Tax, or other items—so real-world surprises can be larger.

Figure 2: Employer payroll configuration drives whether withholding tracks your W-4 closely.

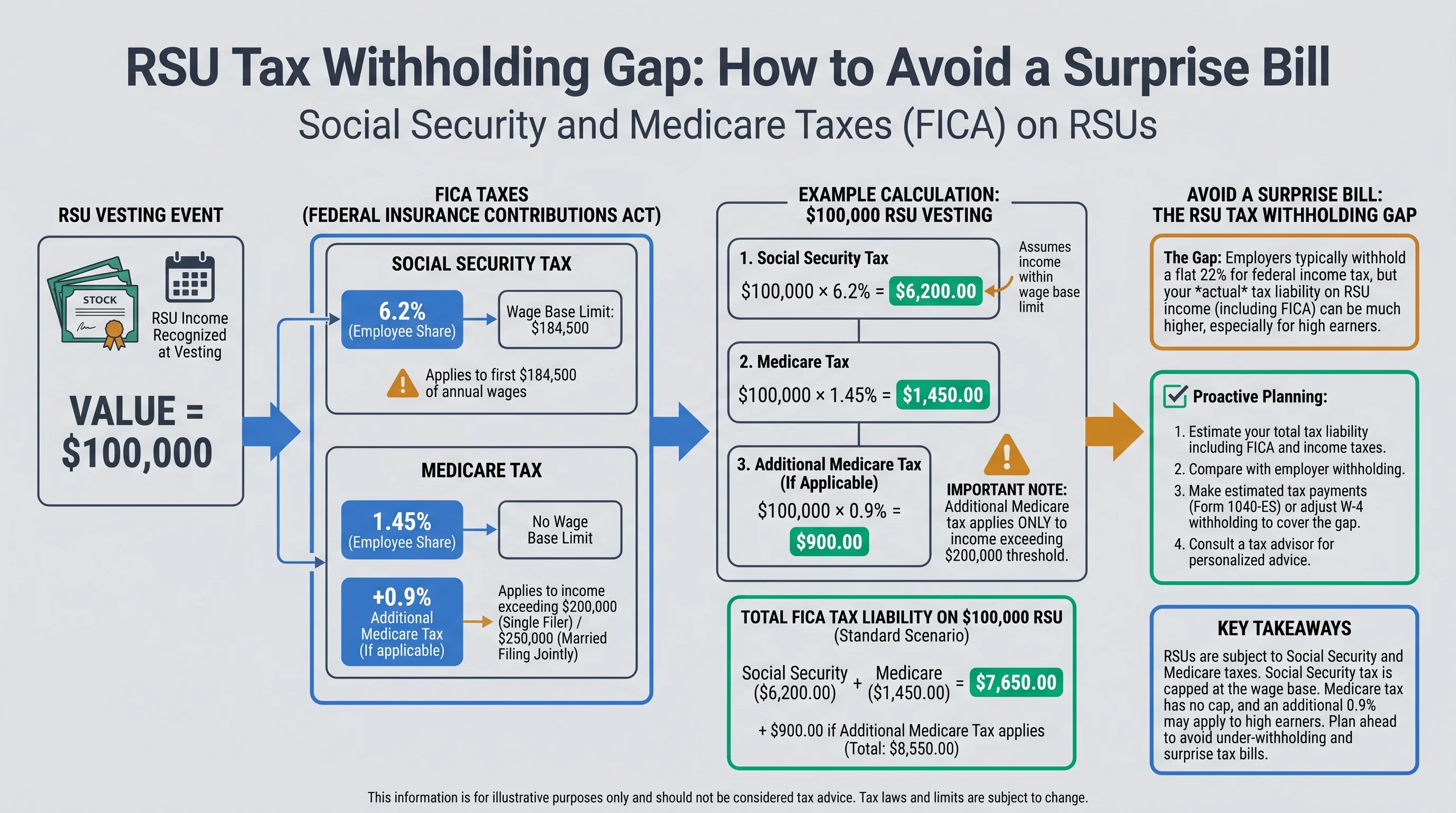

FICA and Medicare: Separate From the “22% Gap”

RSU vesting generally triggers FICA taxes in typical employee settlements:

| Tax | Typical employee rate | Notes |

|---|---|---|

| Social Security | 6.2% | Applies up to the annual wage base |

| Medicare | 1.45% | No wage cap |

| Additional Medicare Tax | 0.9% | Applies to wages above thresholds for high earners |

Employees sometimes confuse “I paid payroll taxes” with “I prepaid all federal income tax I owe.” They are different buckets.

State Withholding: Another Layer of “Surprise”

Even if federal withholding is decent, state withholding may not match your state marginal rate—especially if you work in high-tax jurisdictions or have multi-state travel. If you relocated, read relocating with equity.

How to Close the Gap (The Practical Playbook)

Option A: Increase withholding on your W-4

The most common fix is to add extra withholding (often via Form W-4, Step 4(c)) so your regular paychecks collect enough tax to cover RSU-driven liability. See Form W-4 adjustments for equity compensation.

Option B: Quarterly estimated tax payments

If you prefer not to touch W-4, you can pay estimated taxes using Form 1040-ES. The IRS discusses underpayment rules and safe harbors in Publication 505.5 Also see our estimated tax payments guide.

Option C: Model the problem before vest season

Use calculators to stress-test withholding:

Option D: Coordinate with AMT / ISO planning (if you also have options)

If you have ISOs, RSU income can indirectly change tax outcomes via bracket effects—even though ISOs are a different asset class. Keep AMT planning on your radar if you exercise.

Figure 3: Pick a lane—usually W-4 adjustments or estimated payments.

Underpayment Penalties: What You Are Trying to Avoid

If you owe too much at filing, you may hit estimated tax underpayment rules. The IRS outlines exceptions and safe harbors in Publication 505 (for example, paying at least 90% of current-year tax or 100%/110% of prior-year tax depending on income).5

NIIT and High Earners: Don’t Forget the Investment Tax Stack

If you have large RSU income plus taxable investment income, you may need to model Net Investment Income Tax (NIIT) separately. RSU wages can push modified AGI, which affects NIIT exposure. Start with NIIT and equity compensation.

Sell-to-Cover vs Net Settlement: Liquidity vs Withholding Adequacy

Many public-company RSU programs default to sell-to-cover or net settlement so you do not have to mail a check for taxes on vest day. That solves cash liquidity, but it does not automatically solve annual tax adequacy.

What sell-to-cover is doing

On vest, the employer (or broker) calculates withholding obligations and sells enough shares to fund required payroll taxes. The remaining shares deposit into your brokerage account. The taxable wage amount is still generally based on the value at vest—not on how many shares you keep.

Why you can still owe in April

Sell-to-cover uses the same underlying withholding rules as any other payroll settlement. If the income tax withheld on the vest is too flat relative to your annual tax picture, you can finish the year underpaid even though the vest “felt” fully taxed.

For a deeper dive on mechanics, read RSU sell-to-cover withholding explained.

Multi-Vest Years: How Lumpy Income Breaks “Set and Forget” W-4s

Tech schedules often cluster RSU vesting on monthly, quarterly, or semi-annual cadences. A W-4 calibrated for base salary alone may be reasonable in January and dangerously low by December once two or three large vests stack.

A two-vest illustration (conceptual)

Suppose you vest $80,000 in February and $80,000 in August, and your employer uses 22% federal income tax withholding on each supplemental payment (illustrative):

Per vest federal income tax withheld ≈ $80,000 × 22% = $17,600

Two vests total withheld ≈ $35,200 on $160,000 of RSU wages

If the average federal marginal rate on that RSU slice across the year is closer to 32%, the “expected” federal income tax on the RSU wages alone might be closer to:

$160,000 × 32% = $51,200

Illustrative gap ≈ $16,000 (before state taxes and other items)

This is why equity-heavy employees often do a mid-year projection in June—not because they love taxes, but because June is the last easy moment to fix withholding before a big November/December vest.

Year-End Equity Tax Checklist (Employee Version)

| Step | Why it matters |

|---|---|

| Export YTD paystubs | Withholding is the only lever you control mid-year |

| List scheduled vest dates | Big December vests decide whether you need a Q4 estimated payment |

| Reconcile W-4 Step 4(c) | A small extra per-paycheck amount can offset a flat supplemental shortfall |

| Model state residency | Remote moves can change withholding obligations |

| If you sell shares after vest | Separate capital gain/loss tracking from the wage inclusion at vest |

If you want a broader December playbook, see equity compensation year-end tax planning.

If your spouse also earns equity, run the projection jointly—household withholding is a single pool for many safe-harbor tests, and marriage can change marginal brackets materially.

How to Talk to Payroll (Without Sounding Accusatory)

You will get farther if you assume compliance is doing something rational under IRS rules—not “trying to underwithhold.”

Questions that usually get useful answers

- Do you treat RSU settlement as supplemental wages for federal income tax withholding?

- Do you use the flat rate method or the aggregate method for typical equity settlements?

- If flat: what rate are you applying on payments under $1 million, and does it change when RSUs are paid with salary in the same period?

- What state withholding rate is applied by default for equity, and can it be increased on request?

What you can request (sometimes)

Some employers allow employees to elect extra withholding on equity events or to coordinate aggregate treatment when operational constraints allow. Others do not. If payroll cannot change methodology, your fallback remains W-4 adjustments or estimated tax.

Private Companies vs Public Companies: Same Tax Idea, Different Friction

Public companies usually have mature equity payroll integrations and broker-driven settlements. Private companies may have fewer vest events, but surprises still happen when a liquidity event (tender offer, secondary sale) creates large wage inclusions with flat withholding.

If you are navigating private-market liquidity, read secondary markets and tender offers for context—but keep withholding on your checklist whenever cash hits payroll.

Frequently Asked Questions

Is RSU withholding always 22%?

Answer: Not necessarily. Employers follow IRS rules for supplemental wages, and the rate depends on facts like whether wages are paid concurrently, totals for the year, and whether the employer uses flat or aggregate methods. Many employees see 22% as a common outcome for large supplemental payments under $1 million, but it is not universal.

Source: IRS Publication 15

Does my employer withhold enough for my tax bracket?

Answer: Not automatically. Withholding aims to approximate liability, but supplemental methods can be flat, which may be too low if your marginal rate is higher than the flat rate used.

Source: IRS Publication 15-T

Are RSU taxes FICA wages?

Answer: Typically yes for employee RSUs settled through payroll—Social Security and Medicare often apply, subject to thresholds and wage bases.

Source: IRS Tax Topic 751

What is the difference between sell-to-cover and withholding shortfalls?

Answer: Sell-to-cover decides how shares are sold to fund withholding at vest. A withholding shortfall is when the total tax withheld across the year is still less than your eventual liability. You can have clean sell-to-cover mechanics and still owe at filing if federal withholding was too flat relative to your bracket.

Source: IRS Publication 15

Should I use estimated tax or W-4 adjustments?

Answer: Either can work. W-4 changes are simpler for many W-2 employees; estimated tax can help if you have volatile non-wage income or prefer direct payments.

Source: IRS Publication 505

Do RSUs affect my NIIT?

Answer: RSU wages increase income and can affect thresholds indirectly. NIIT is separate from wage withholding and may require projection.

Source: IRS Publication 505

What records should I keep?

Answer: Keep paystubs, equity statements, Form W-2, and brokerage 1099-B records for sales after vest. Cost basis mistakes are a separate problem from withholding gaps—see Form 1099-B stock compensation.

Source: IRS Publication 525

Can I fix this mid-year?

Answer: Often yes. Mid-year W-4 adjustments and remaining estimated payments can reduce April surprises if you act before year-end.

Source: IRS Form W-4 instructions

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS Publication 15 | IRS | irs.gov |

| IRS Publication 15-T | IRS | irs.gov |

| IRS Publication 505 | IRS | irs.gov |

| IRC §83 | Statute | law.cornell.edu |

Disclaimer: This guide is educational and not individualized tax advice. Tax rules change, employers vary, and state laws differ. Consult a CPA or tax advisor for projections tied to your W-4, RSU settlements, and multi-state facts.

Footnotes

-

Your annual reconciliation on Form 1040 compares total tax to withholding plus refundable credits and other payments; equity withholding is only one component. ↩

-

Employer payroll departments must follow IRS guidance; employees do not choose the employer’s supplemental wage method. ↩

-

See IRC §83 for the general inclusion framework for property transferred in connection with services. ↩

-

See IRS Publication 15 and Publication 15-T for employer withholding methods and tables. ↩

-

See IRS Publication 505 for estimated tax rules and safe harbors. ↩ ↩2