Executive Summary

Why isn't my RSU withholding enough to cover my taxes?

Employers withhold RSU vesting and NSO exercise income at a flat 22% federal rate (or 37% if you've had over $1 million in supplemental wages that year). If your marginal tax bracket is 32%, 35%, or 37%, you'll owe the difference at tax time. High earners commonly face a 10–15% shortfall, plus state tax gaps.

Over 40% of employees with RSU vesting report owing additional tax at filing—and many are surprised by underpayment penalties.1 The culprit is supplemental wage withholding: a flat rate that doesn't account for your actual tax bracket. If you earn enough to be in the 32% or higher bracket, 22% withholding leaves a significant gap.

The bottom line: Supplemental income is withheld at 22% (or 37% in limited cases). Your marginal rate may be higher. Plan for the gap with increased withholding or estimated payments.2

Critical Warning: Underpayment penalties can add 4–6% to your tax bill if you don't meet safe-harbor thresholds. The IRS expects you to pay as you go—withholding or estimated tax—not in one lump at filing. New parents on leave may face additional gaps when vesting continues—see our Equity for New Parents guide.3

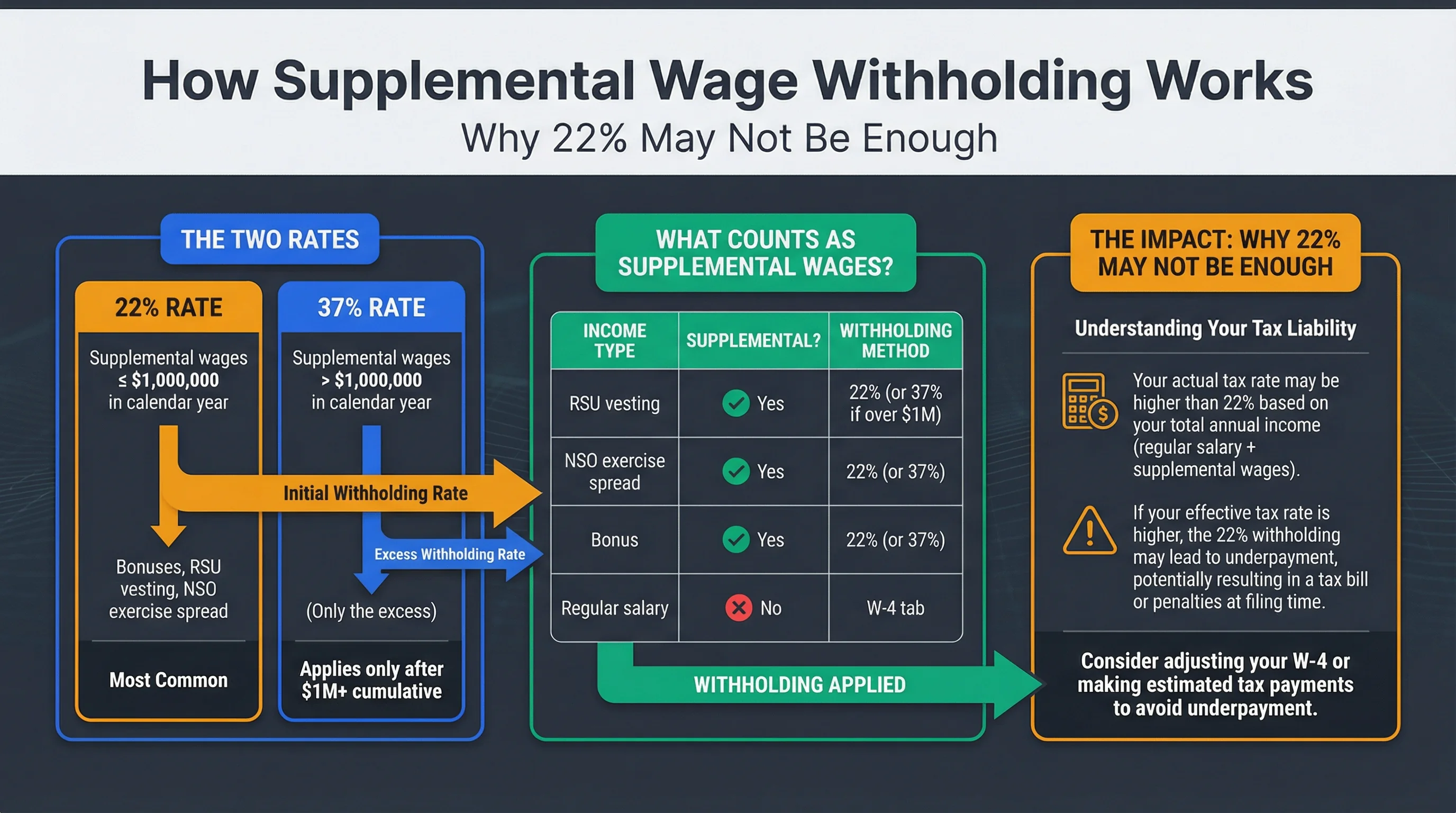

How Supplemental Wage Withholding Works

The Two Rates

The IRS allows employers to withhold supplemental wages (bonuses, RSU vesting, NSO exercise spread) at:4

| Rate | When It Applies |

|---|---|

| 22% | Supplemental wages ≤ $1 million in the calendar year |

| 37% | Supplemental wages > $1 million in the calendar year (only the excess) |

Most RSU and option events fall under the 22% rate. The 37% rate applies only after you've already received $1M+ in supplemental wages that year.

What Counts as Supplemental Wages?

| Income Type | Supplemental? | Withholding Method |

|---|---|---|

| RSU vesting | Yes | 22% (or 37% if over $1M) |

| NSO exercise spread | Yes | 22% (or 37%) |

| Bonus | Yes | 22% (or 37%) |

| Regular salary | No | W-4 tables (marginal rate) |

| ISO exercise (held) | No withholding | You may owe AMT; no W-2 withholding |

Source: IRS Publication 15-T

Figure 1: Supplemental wage withholding — 22% and 37% rates, RSU and NSO treatment.

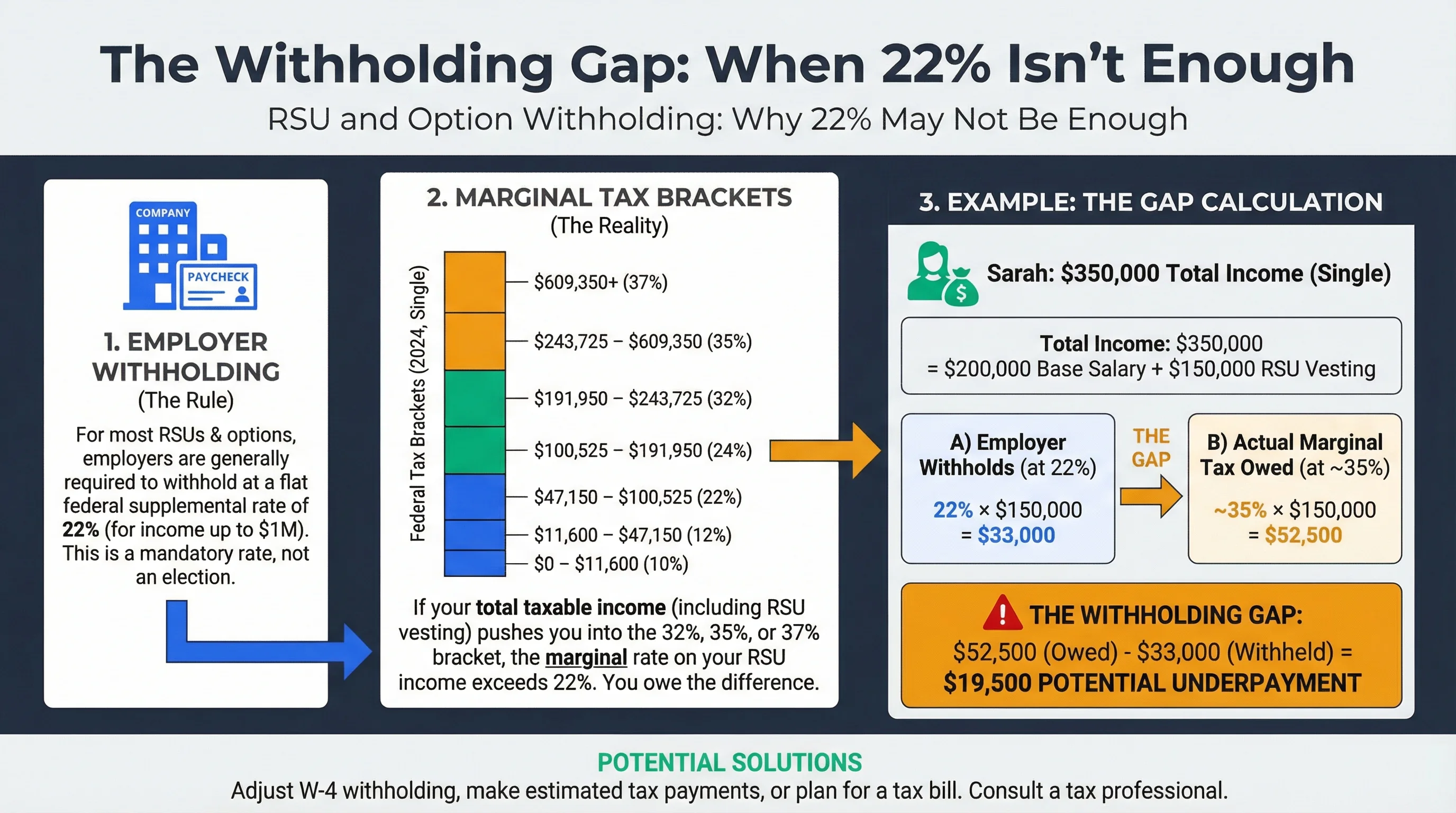

The Withholding Gap: When 22% Isn't Enough

Federal Tax Brackets (2024, Single)

| Bracket | Income Range | Rate |

|---|---|---|

| 10% | $0 – $11,600 | 10% |

| 12% | $11,600 – $47,150 | 12% |

| 22% | $47,150 – $100,525 | 22% |

| 24% | $100,525 – $191,950 | 24% |

| 32% | $191,950 – $243,725 | 32% |

| 35% | $243,725 – $609,350 | 35% |

| 37% | $609,350+ | 37% |

If your total taxable income (including RSU vesting) pushes you into the 32%, 35%, or 37% bracket, the marginal rate on your RSU income exceeds 22%. You owe the difference.

Example: The Gap

Sarah has $200,000 base salary and $150,000 RSU vesting. Total income: $350,000.

- Employer withholds: 22% × $150,000 = $33,000 on RSUs

- Actual marginal rate: ~35% (she's in the 35% bracket)

- Tax owed on RSUs: ~35% × $150,000 = $52,500

- Gap: $52,500 − $33,000 = $19,500 owed at filing

Source: IRS Publication 505

Figure 2: The withholding gap — when 22% falls short of your marginal rate.

State and FICA Considerations

State Withholding

States handle supplemental wages differently. Some use a flat rate; others use your marginal rate. Common gaps:

| State | Typical Supplemental Rate | Notes |

|---|---|---|

| California | 10.23% (supplemental) | High earners may be in 12.3%+ bracket |

| New York | Varies | Can use aggregate or flat method |

| Washington | No state income tax | N/A |

| Texas | No state income tax | N/A |

Related Guides: California Tax on Equity Compensation, Multi-State Tax for Remote Workers.

FICA (Social Security and Medicare)

- Social Security: Capped at $168,600 (2024). If you've already hit the cap from salary, RSU vesting may not add more.

- Medicare: 1.45% on all + 0.9% Additional Medicare Tax on income over $200,000 (single). RSU vesting counts.

How to Avoid Underpayment Penalties

Safe Harbor Rules

The IRS generally won't penalize you if you've paid during the year:5

- 100% of prior year's tax (110% if prior year AGI > $150,000), or

- 90% of current year's tax

| Prior Year Tax | Safe Harbor (AGI ≤ $150K) | Safe Harbor (AGI > $150K) |

|---|---|---|

| $50,000 | Pay $50,000 during year | Pay $55,000 during year |

| $100,000 | Pay $100,000 during year | Pay $110,000 during year |

Options to Close the Gap

| Strategy | How It Works | Pros | Cons |

|---|---|---|---|

| Increase W-4 withholding | Add extra amount per paycheck | Simple, automatic | May over-withhold early in year |

| Estimated quarterly payments | Form 1040-ES, pay 4x/year | Precise control | Manual, deadlines |

| Sell shares at vesting | Use proceeds to cover tax | No cash out of pocket | Concentrates risk; not always allowed |

| Year-end bonus withholding | Ask for higher % on bonus | One-time adjustment | Depends on employer |

Related Guides: Use our RSU Tax Estimator to model your withholding gap.

Figure 3: Avoiding underpayment penalties — safe harbor rules and payment options.

Frequently Asked Questions

Can I ask my employer to withhold more than 22% on RSUs?

Answer: Some employers allow you to elect a higher withholding rate or additional amount. Many do not—their payroll system uses the statutory 22%. Check with HR or your equity administrator.

What if I'm in the 22% bracket—am I covered?

Answer: If your marginal rate is 22%, the withholding may roughly match. But state tax, Medicare (1.45% + 0.9% if over $200K), and phase-outs can still create a gap. Model your situation.

Do I need to make estimated payments if I have a big RSU vest in Q4?

Answer: The IRS expects you to pay as you earn. If you have a large Q4 vest, you may need to make an estimated payment by January 15 of the following year to avoid penalties. Consult a tax advisor.

Does ISO exercise trigger withholding?

Answer: No. ISO exercise (if you hold the shares) doesn't create W-2 income, so there's no withholding. You may owe AMT—plan for it separately. See our ISO AMT Impact Calculator.

How do I calculate my estimated tax for RSU vesting?

Answer: Estimate total income (salary + RSU + other), apply marginal rate, subtract expected withholding. Use our RSU Tax Estimator or work with a CPA.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS Publication 15-T | Reference | https://www.irs.gov/publications/p15t |

| IRS Publication 505 | Reference | https://www.irs.gov/publications/p505 |

| IRC Section 3402 | Reference | https://www.law.cornell.edu/uscode/text/26/3402 |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Tax laws vary by jurisdiction and change frequently. Always consult a qualified tax professional (CPA, tax attorney, enrolled agent) before making decisions based on this information. The authors accept no liability for actions taken based on this content.