Executive Summary

What is the difference between ISO qualifying and disqualifying disposition?

A qualifying disposition means you held the shares at least 2 years from the ISO grant date AND 1 year from the exercise date. You pay no regular income tax at exercise; the entire gain is taxed as long-term capital gains (0%, 15%, or 20%). A disqualifying disposition occurs when you sell before meeting both holding periods—the spread at exercise is taxed as ordinary income (up to 37%), and you lose the capital gains benefit.

The tax difference between a qualifying and disqualifying ISO disposition can exceed $170,000 on a $1 million gain. Yet many employees accidentally trigger a disqualifying disposition by selling too soon—or by not understanding the two-part holding rule.1 This guide explains exactly when you qualify, when you don't, and how to plan your sale.

The bottom line: The 2-year (from grant) and 1-year (from exercise) holding periods are strict. Miss either one, and your ISO is treated like an NSO—ordinary income on the spread.2

Critical Warning: Selling ISO shares the same day you exercise is always a disqualifying disposition. You receive no ISO tax benefit—the spread is taxed as ordinary income. If you need liquidity, consider whether exercising and holding is worth the risk.3

For the payroll tax angle—when FICA/FUTA generally do not apply to statutory ISO exercise and stock disposition amounts even if you disqualify for income tax—see ISO disqualifying disposition: FICA, FUTA & W-2 reporting.

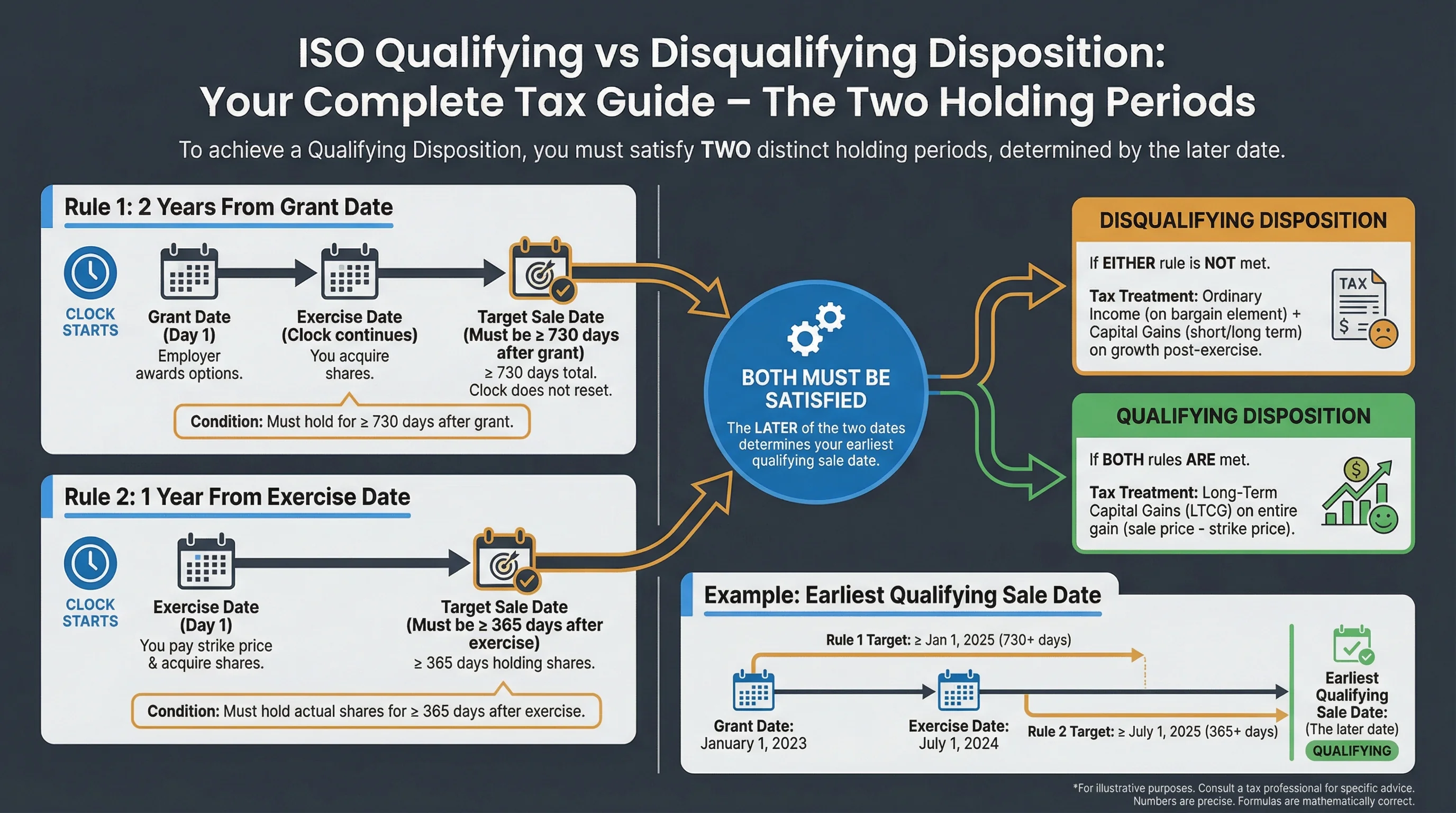

The Two Holding Periods

Rule 1: 2 Years From Grant Date

The grant date is when your employer awarded the options. The clock starts then—not when you exercise.

| Event | Start of 2-Year Clock |

|---|---|

| Grant date | Day 1 |

| Exercise date | Clock continues |

| Sale date | Must be ≥ 730 days after grant |

Rule 2: 1 Year From Exercise Date

The exercise date is when you paid the strike price and acquired the shares. You must hold the actual shares for at least 365 days.

| Event | Start of 1-Year Clock |

|---|---|

| Exercise date | Day 1 |

| Sale date | Must be ≥ 365 days after exercise |

Both Must Be Satisfied

You need both holding periods. The later of the two dates determines your earliest qualifying sale date.

Example: Grant: Jan 1, 2024. Exercise: June 1, 2025.

- 2 years from grant: Jan 1, 2026

- 1 year from exercise: June 1, 2026

- Earliest qualifying sale: June 1, 2026

Source: IRC Section 422(a)(1)

Figure 1: The two holding periods — both must be satisfied for qualifying disposition.

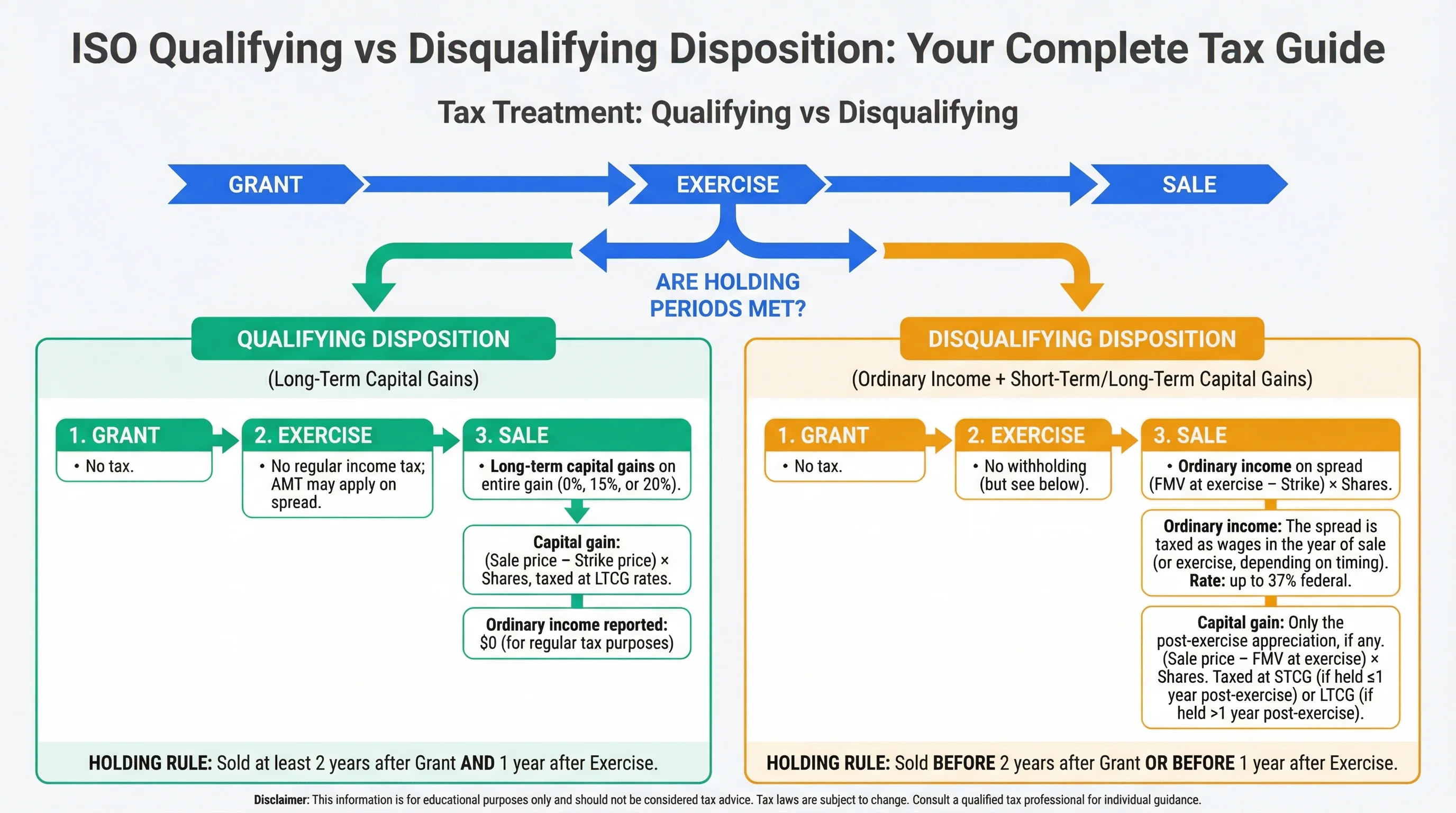

Tax Treatment: Qualifying vs Disqualifying

Qualifying Disposition

| Event | Tax Treatment |

|---|---|

| Grant | No tax |

| Exercise | No regular income tax; AMT may apply on spread |

| Sale | Long-term capital gains on entire gain (0%, 15%, or 20%) |

Ordinary income reported: $0 (for regular tax purposes)

Capital gain: (Sale price − Strike price) × Shares, taxed at LTCG rates

Disqualifying Disposition

| Event | Tax Treatment |

|---|---|

| Grant | No tax |

| Exercise | No withholding (but see below) |

| Sale | Ordinary income on spread (FMV at exercise − Strike) × Shares |

Ordinary income: The spread is taxed as wages in the year of sale (or exercise, depending on timing). Rate: up to 37% federal.

Capital gain: Only the post-exercise appreciation, if any. (Sale price − FMV at exercise) × Shares. Taxed as short-term or long-term depending on holding period.

Source: Treasury Regulation §1.422-1

Figure 2: Tax treatment — qualifying vs disqualifying disposition.

Numerical Example: The $170,000 Difference

Scenario: 1,000 ISOs, strike $10, FMV at exercise $50, sale price $110. Exercise: Jan 2024. Sale: Dec 2024 (disqualifying) vs Jan 2025 (qualifying).

Disqualifying (Sale Dec 2024, <1 year from exercise)

Ordinary income: ($50 − $10) × 1,000 = $40,000

Tax at 37%: $14,800

Capital gain: ($110 − $50) × 1,000 = $60,000 (short-term)

Tax at 37%: $22,200

Total federal tax: $37,000

Qualifying (Sale Jan 2025, ≥1 year from exercise)

Ordinary income: $0

Capital gain: ($110 − $10) × 1,000 = $100,000 (long-term)

Tax at 20%: $20,000

Total federal tax: $20,000

Savings: $17,000

On a $1M gain, the difference is $170,000 (37% vs 20%).

AMT: The Hidden Factor

Even with a qualifying disposition, AMT may apply at exercise. The spread (FMV − strike) is an AMT preference item.

| Scenario | AMT at Exercise? |

|---|---|

| Qualifying disposition | Yes, if spread pushes you into AMT |

| Disqualifying disposition | No AMT on spread (it's ordinary income) |

AMT credit: If you pay AMT in the exercise year, you may recover it as a credit in future years when your regular tax exceeds AMT. Use our ISO AMT Impact Calculator to model.

Related Guides: AMT Planning for Stock Options, ISO vs NSO Guide.

When Disqualifying Might Make Sense

In rare cases, a disqualifying disposition can be intentional:

| Situation | Why Disqualify? |

|---|---|

| Stock has fallen since exercise | Lock in loss; ordinary income may be lower than expected |

| Need liquidity urgently | Same-day sale avoids market risk |

| AMT exposure is extreme | Disqualifying converts spread to ordinary income—no AMT preference |

| Leaving country | Simplify tax reporting |

For most employees: Holding for qualifying is the better choice.

Figure 3: Decision factors — when disqualifying might be intentional.

Action Checklist

Frequently Asked Questions

What if I sell one day before the 1-year mark?

Answer: Disqualifying disposition. The holding periods are strict—no exceptions. One day early costs you the capital gains treatment.

Does the 2-year clock reset if I exercise in tranches?

Answer: No. The 2-year clock starts at grant for all shares from that grant. Each exercise starts its own 1-year clock.

Can I have a qualifying disposition if I exercise after leaving the company?

Answer: Yes, if you exercise within 90 days of leaving (or 12 months if disabled). The holding periods still apply from grant and exercise.

How is a disqualifying disposition reported on my tax return?

Answer: The spread is reported as compensation (W-2 or 1099). Your employer files Form 3921. You report the sale on Form 8949 and Schedule D, with basis adjustment for the compensation already taxed.

What if my company is acquired before I meet the holding period?

Answer: If your options are substituted in the deal (per IRC Section 424), the holding period may tack. If cashed out, it's a disqualifying disposition. See our Stock Options in M&A guide.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRC Section 422 | Reference | https://www.law.cornell.edu/uscode/text/26/422 |

| IRS Publication 525 | Reference | https://www.irs.gov/publications/p525 |

| Treasury Regulation §1.422-1 | Reference | https://www.law.cornell.edu/cfr/text/26/1.422-1 |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Always consult a qualified tax professional before making decisions based on this information.