Executive Summary

Should I exercise and sell my ISO options the same day or hold for capital gains?

Same-day sale avoids cash outlay and market risk but taxes the spread as ordinary income (up to 37%)—you get no ISO benefit. Holding 2 years from grant and 1 year from exercise qualifies for long-term capital gains (0-20%) but requires cash to exercise, may trigger AMT, and exposes you to stock risk. The better choice depends on your income, cash availability, and conviction in the stock.

The decision to exercise ISO options and sell immediately—or hold for qualifying disposition—is one of the most consequential tax choices tech employees face. Same-day sale is simple and risk-free but expensive. Holding can save six figures in tax but requires cash, invites AMT, and bets on the stock.1 This guide provides a framework to decide.

The bottom line: There is no universal answer. Model both scenarios with your numbers—income, spread, AMT exposure, and time horizon.2

Figure 1: Same-day sale vs hold — key tradeoffs.

Critical Warning: Holding ISO shares exposes you to AMT at exercise. The spread (FMV − strike) is an AMT preference item. Even with a qualifying disposition later, you may owe significant AMT in the exercise year. Use our ISO AMT Impact Calculator before committing.3

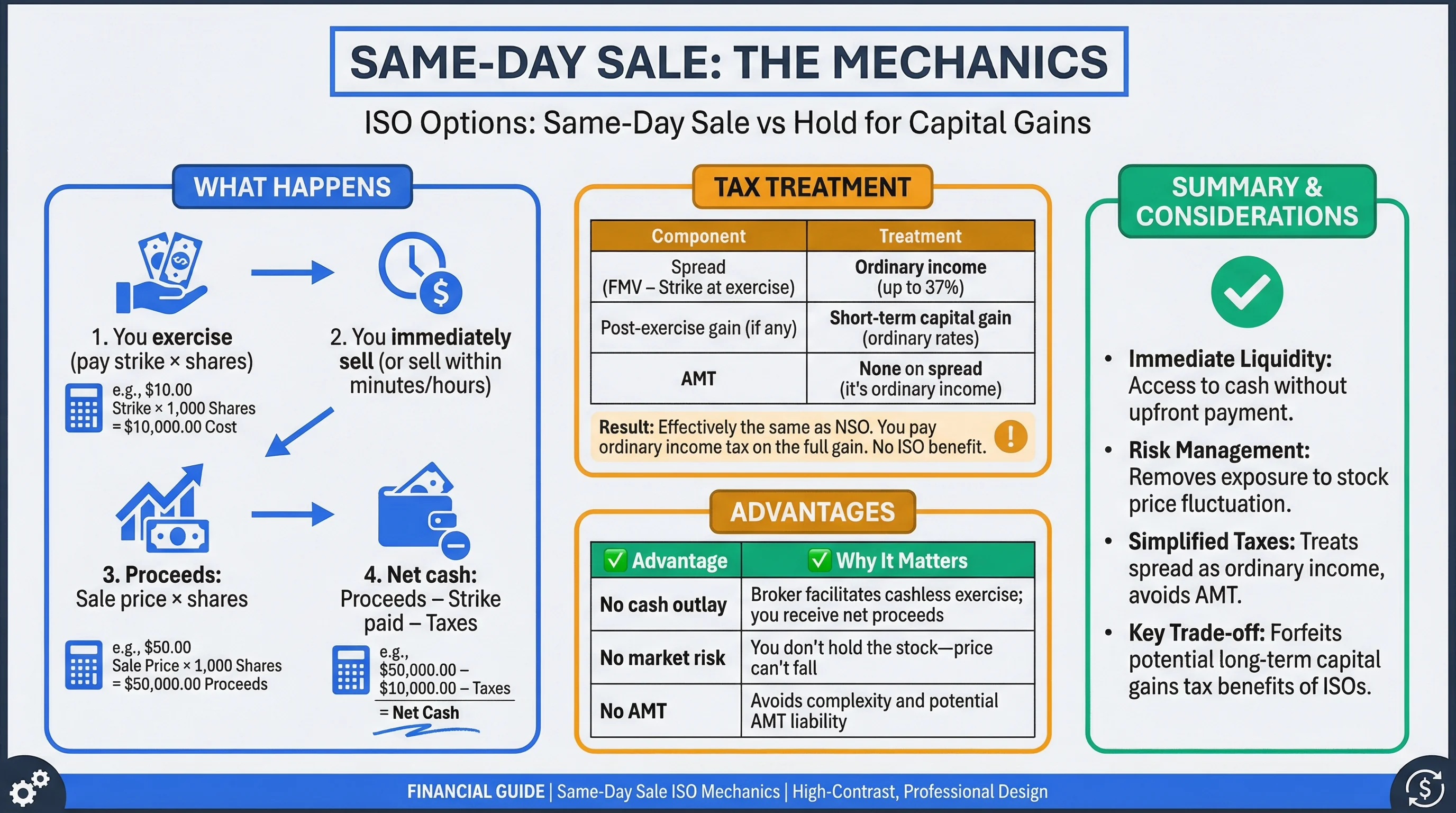

Same-Day Sale: The Mechanics

What Happens

- You exercise (pay strike × shares)

- You immediately sell (or sell within minutes/hours)

- Proceeds: Sale price × shares

- Net cash: Proceeds − Strike paid − Taxes

Tax Treatment

| Component | Treatment |

|---|---|

| Spread (FMV − Strike at exercise) | Ordinary income (up to 37%) |

| Post-exercise gain (if any) | Short-term capital gain (ordinary rates) |

| AMT | None on spread (it's ordinary income) |

Result: Effectively the same as NSO. You pay ordinary income tax on the full gain. No ISO benefit.

Advantages

| Advantage | Why It Matters |

|---|---|

| No cash outlay | Broker facilitates cashless exercise; you receive net proceeds |

| No market risk | You don't hold the stock—price can't fall |

| No AMT | Spread is ordinary income, not AMT preference |

| Predictable | You know your tax bill at exercise |

| Liquidity | Immediate access to proceeds |

Disadvantages

| Disadvantage | Cost |

|---|---|

| Ordinary income rates | Up to 37% federal vs 20% LTCG |

| State tax | Often 5-13% additional |

| No upside capture | If stock doubles after exercise, you don't benefit |

Figure 2: Tax comparison — same-day sale (ordinary) vs hold (LTCG).

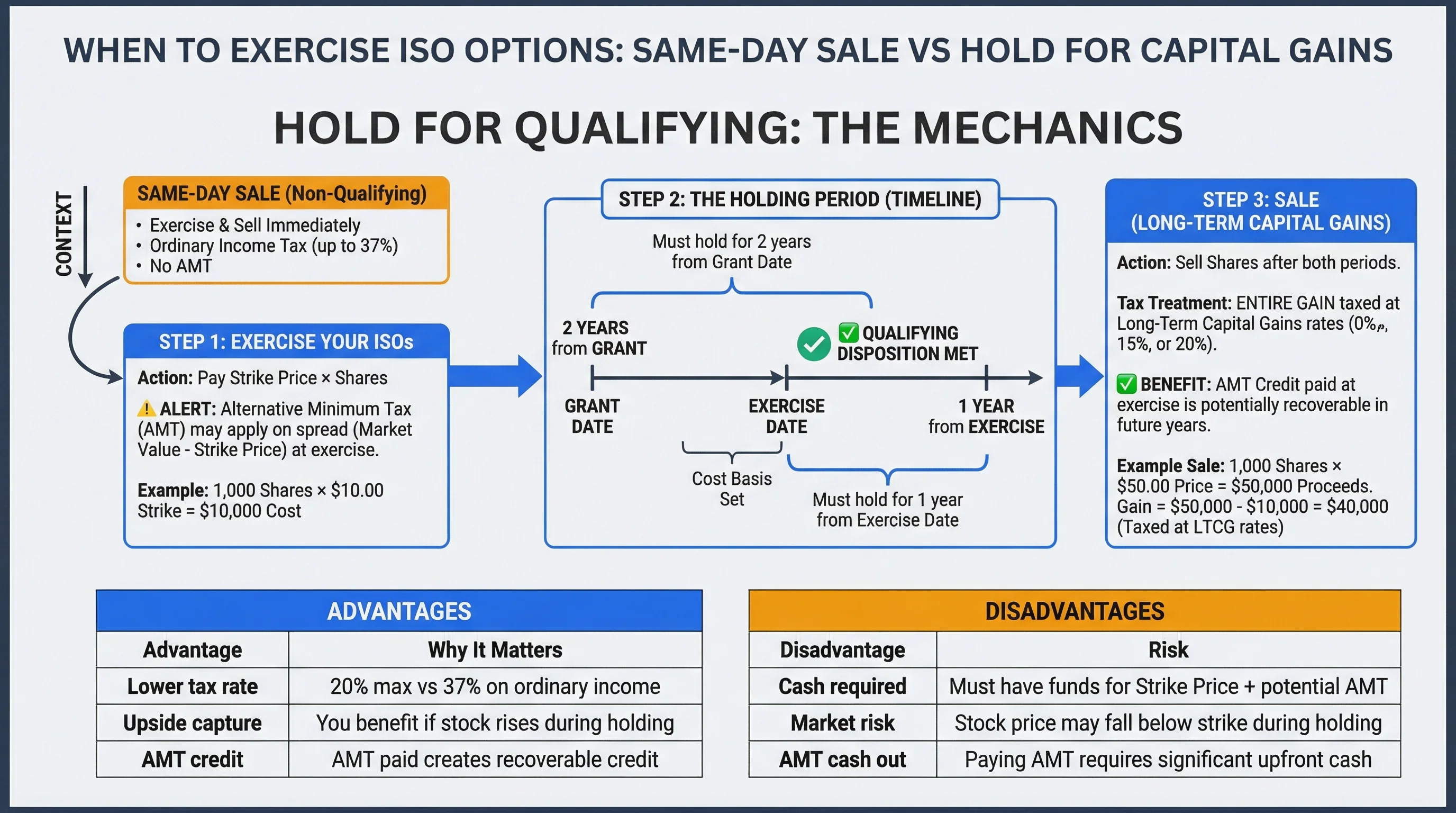

Hold for Qualifying: The Mechanics

What Happens

- You exercise (pay strike × shares)

- You hold the shares for 2 years from grant + 1 year from exercise

- You sell after both periods

- Gain taxed as long-term capital gains

Tax Treatment

| Component | Treatment |

|---|---|

| At exercise | No regular income tax; AMT may apply on spread |

| At sale | Long-term capital gains (0%, 15%, or 20%) on entire gain |

| AMT credit | Recoverable in future years if you paid AMT |

Advantages

| Advantage | Why It Matters |

|---|---|

| Lower tax rate | 20% max vs 37% on ordinary income |

| Upside capture | You benefit if stock rises |

| AMT credit | AMT paid creates recoverable credit |

Disadvantages

| Disadvantage | Risk |

|---|---|

| Cash required | Must pay strike × shares at exercise |

| AMT at exercise | May owe large AMT bill even before selling |

| Stock risk | Stock can fall—you lose money |

| Illiquidity | Can't access proceeds for 1+ year |

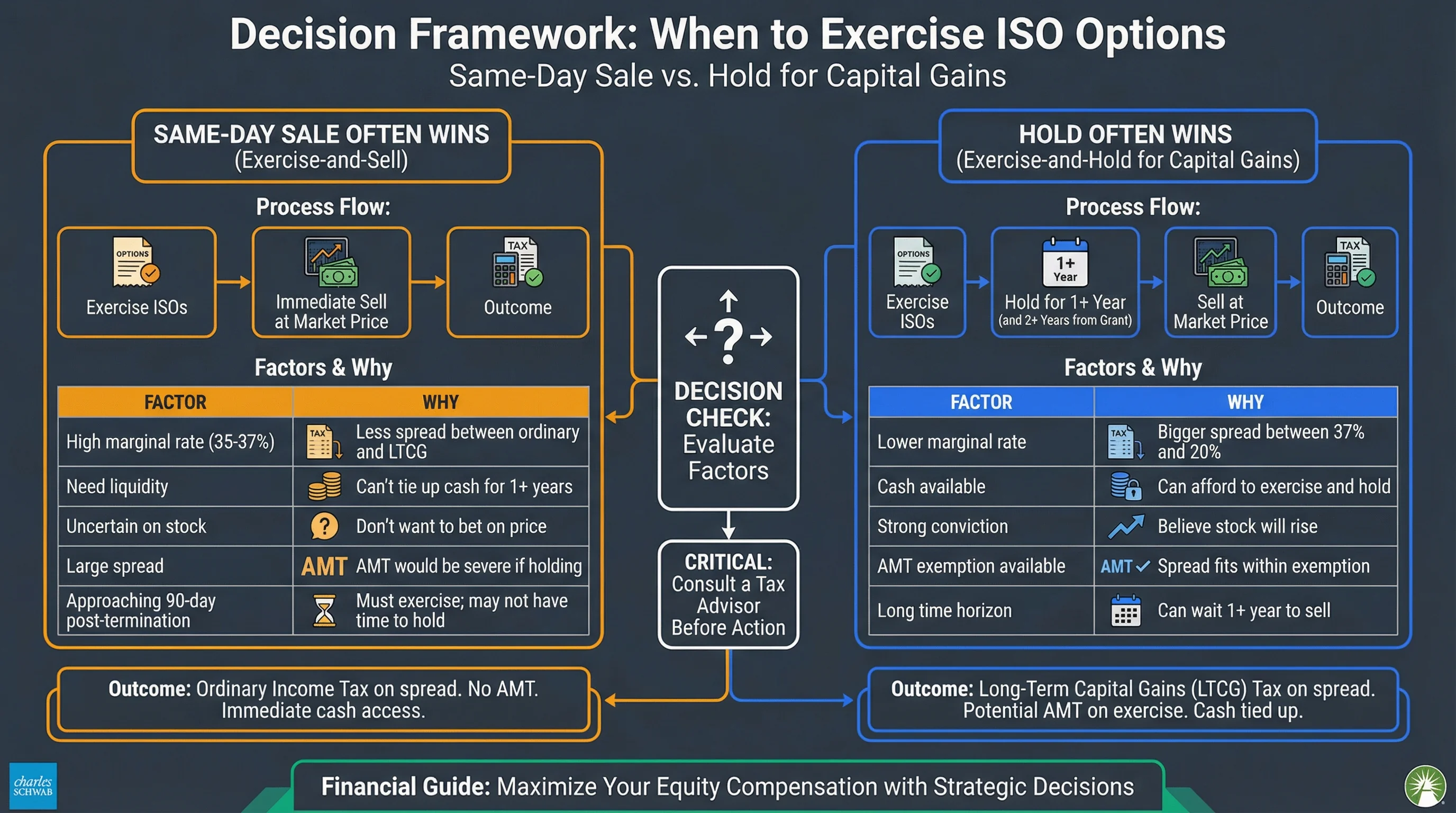

Decision Framework

When Same-Day Sale Often Wins

| Factor | Why |

|---|---|

| High marginal rate (35-37%) | Less spread between ordinary and LTCG |

| Need liquidity | Can't tie up cash for 1+ years |

| Uncertain on stock | Don't want to bet on price |

| Large spread | AMT would be severe if holding |

| Approaching 90-day post-termination | Must exercise; may not have time to hold |

When Hold Often Wins

| Factor | Why |

|---|---|

| Lower marginal rate | Bigger spread between 37% and 20% |

| Cash available | Can afford to exercise and hold |

| Strong conviction | Believe stock will rise |

| AMT exemption available | Spread fits within exemption |

| Long time horizon | Can wait 1+ year to sell |

Figure 3: Decision framework — when each strategy wins.

Numerical Comparison

Scenario: 1,000 ISOs, strike $10, FMV $50. Sale price if holding: $80 (after 1 year). Marginal rate: 37%. LTCG rate: 20%.

Same-Day Sale (Sale at $50)

Gain: ($50 − $10) × 1,000 = $40,000

Tax (37%): $14,800

Net: $40,000 − $14,800 = $25,200

Hold (Sale at $80)

Exercise: Pay $10,000 (strike)

AMT on spread ($40,000): Assume $8,000 (simplified)

Sale gain: ($80 − $10) × 1,000 = $70,000

LTCG tax (20%): $14,000

Net: $70,000 − $14,000 − $8,000 AMT = $48,000 (before AMT credit recovery)

Hold wins in this example—but only if the stock reaches $80. If it falls to $30, you lose.

Tools to Model Your Scenario

| Tool | Use For |

|---|---|

| ISO AMT Impact Calculator | AMT at exercise |

| Capital Gains Calculator | LTCG vs ordinary |

| Holding Period Tracker | Qualifying sale date |

| Early Exercise Break-Even | When early exercise pays off |

Related Guides: ISO Qualifying vs Disqualifying Disposition, AMT Planning.

Frequently Asked Questions

Can I do a partial same-day sale and hold the rest?

Answer: Yes. You can sell some shares to cover exercise cost and taxes, and hold the remainder for qualifying disposition. This hybrid approach reduces cash need while preserving some upside.

What if I hold and the stock crashes?

Answer: You lose. You paid the strike price and owe AMT (if applicable). The stock is worth less. This is the key risk of holding—only hold if you can afford the downside.

How does AMT credit recovery work?

Answer: If you pay AMT in the exercise year, you get a credit. In future years when regular tax exceeds AMT, you use the credit to reduce your tax. The credit can take years to fully recover.

Is same-day sale reported differently than hold?

Answer: Same-day sale: spread on W-2 or 1099 as compensation; sale on Form 8949. Hold: Form 3921 at exercise; sale on Form 8949 at disposition. Basis differs—consult a tax advisor.

What if I'm in the 32% bracket—does that change the math?

Answer: Yes. The spread between 32% ordinary and 15% LTCG (or 20%) is smaller than 37% vs 20%. Same-day sale becomes relatively more attractive at lower brackets.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRC Section 422 | Reference | https://www.law.cornell.edu/uscode/text/26/422 |

| IRS Publication 525 | Reference | https://www.irs.gov/publications/p525 |

| Form 6251 | Reference | https://www.irs.gov/pub/irs-pdf/f6251.pdf |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Always consult a qualified tax professional before making decisions based on this information.