Executive Summary

How do I read and understand my equity grant document?

Your equity grant shows: (1) strike price or grant price—the price at which you can buy or receive shares; (2) vesting schedule—when you earn the right to exercise or receive shares, typically 4 years with 1-year cliff; (3) post-termination exercise window—often 90 days to exercise after leaving; (4) option type—ISO or NSO, which affects taxes. Request the full plan document if terms are unclear.

Your equity grant document is a contract—and like any contract, the fine print matters. Misreading a single term can cost you tens of thousands of dollars, whether it's missing an exercise deadline or misunderstanding your vesting acceleration in a merger.1 This guide walks you through each section of a typical grant so you know exactly what you're signing.

The bottom line: Focus on four things: strike price, vesting schedule, post-termination exercise window, and option type. Everything else supports these core terms.2

Critical Warning: The post-termination exercise window (often 90 days) is strict. If you leave and don't exercise within that period, your vested options expire—no extensions. Calendar this date before you give notice.3

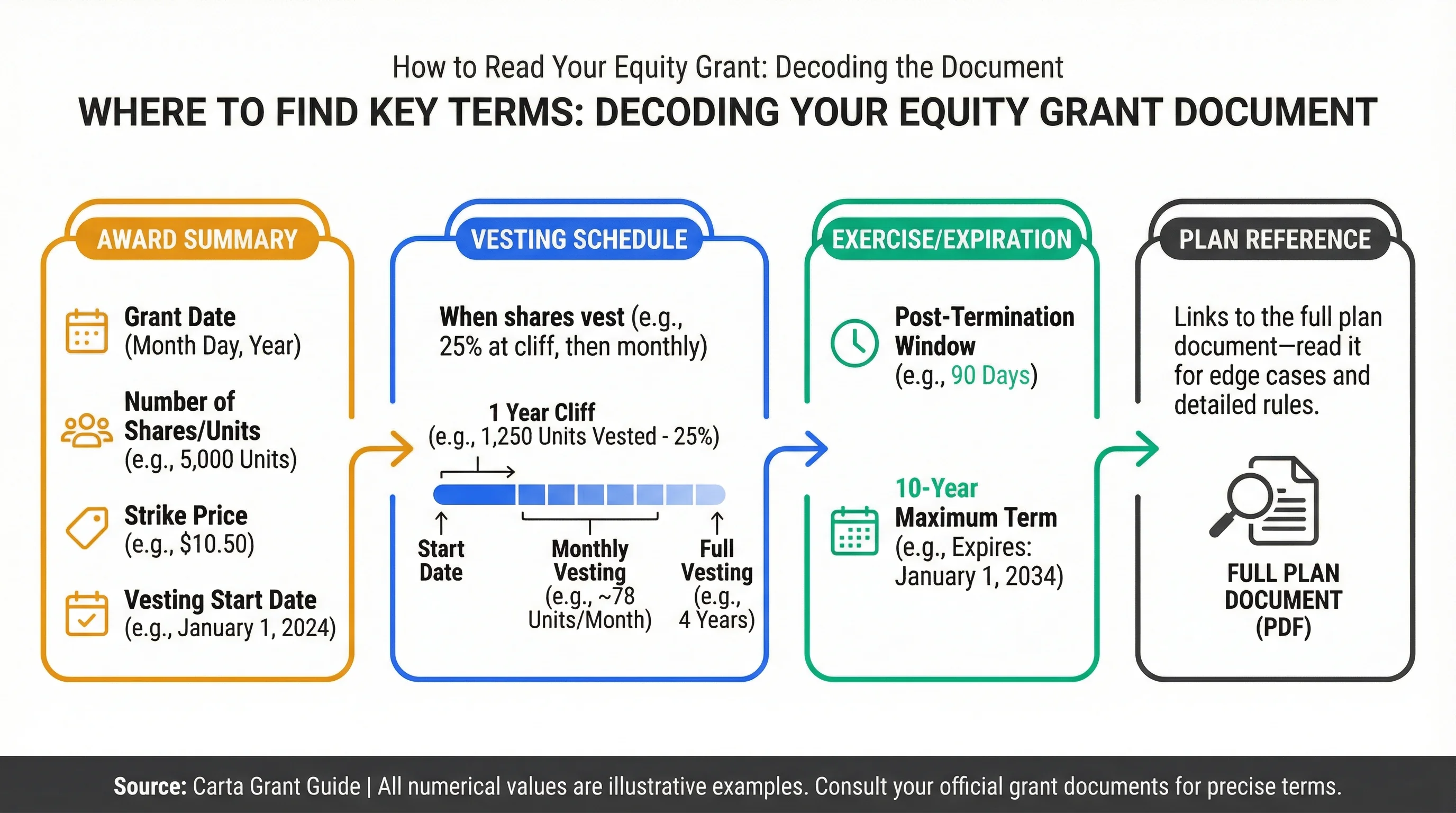

Where to Find Key Terms

Document Structure

Most equity grants follow a similar structure, whether from Carta, E*TRADE, Fidelity, or a custom system:

| Section | What It Contains |

|---|---|

| Award Summary | Grant date, number of shares/units, strike price, vesting start date |

| Vesting Schedule | When shares vest (e.g., 25% at cliff, then monthly) |

| Exercise/Expiration | Post-termination window, 10-year maximum term |

| Plan Reference | Links to the full plan document—read it for edge cases |

Source: Carta Grant Guide

Figure 1: Typical equity grant document structure — where to find strike price, vesting, and exercise deadline.

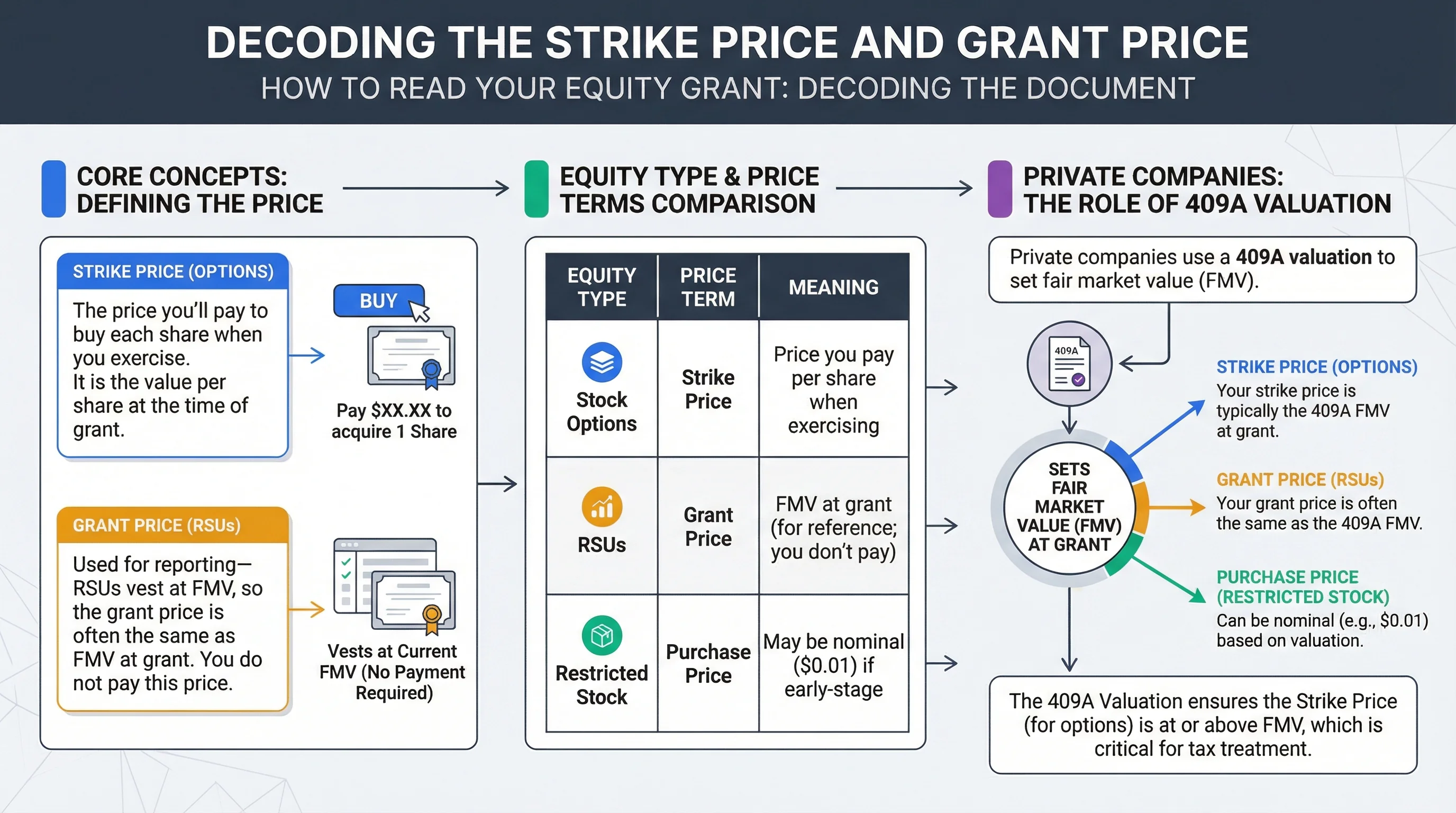

Decoding the Strike Price and Grant Price

What It Means

The strike price (for options) or grant price (for RSUs) is the value per share at the time of grant. For options, it's the price you'll pay to buy each share when you exercise. For RSUs, it's used for reporting—RSUs vest at FMV, so the grant price is often the same as FMV at grant.

| Equity Type | Price Term | Meaning |

|---|---|---|

| Stock Options | Strike Price | Price you pay per share when exercising |

| RSUs | Grant Price | FMV at grant (for reference; you don't pay) |

| Restricted Stock | Purchase Price | May be nominal ($0.01) if early-stage |

For Private Companies: 409A Valuation

Private companies use a 409A valuation to set fair market value (FMV). Your strike price is typically the 409A FMV at grant. The current 409A (updated periodically) tells you today's FMV—and thus your intrinsic value if in-the-money.4

Related Guides: See our Section 409A Valuation guide for how FMV is determined.

Understanding Your Vesting Schedule

Typical Format

Vesting schedules are usually expressed as:

- Time-based: "25% at 1-year cliff, then 1/48th monthly"

- Cliff: The date when the first tranche vests (often 12 months)

- Vesting start date: Usually your start date or grant date

| Vesting Type | Example | What It Means |

|---|---|---|

| 4-year, 1-year cliff | 25% at month 12, then ~2.08%/month | Most common for options |

| 4-year, no cliff | 1/48th monthly from start | Less common; faster initial vest |

| Performance-based | Vest on milestone | Tied to company or individual goals |

Acceleration Clauses

Some grants include acceleration—vesting faster under certain conditions:

| Trigger | Single-Trigger | Double-Trigger |

|---|---|---|

| Change of control | All unvested vests on deal close | Unvested vests only if you're terminated after deal |

| Death/Disability | Often full acceleration | Varies by plan |

Source: Stock Options in M&A guide

Figure 2: Vesting schedule — cliff, acceleration, and change of control triggers.

The Post-Termination Exercise Window

Why It Matters

When you leave, you have a limited time to exercise vested options. After that, they expire—worthless.

| Typical Window | Common For |

|---|---|

| 90 days | Most ISO/NSO plans (IRC Section 422 requires ≤3 months for ISO) |

| 30 days | Some startups (shorter = more pressure) |

| 1–10 years | Good leavers (retirement, disability, death) |

Where to find it: Look for "Post-Termination Exercise Period," "Exercise Period Following Termination," or similar. It's often in the plan document, not the award letter.

ISO vs NSO: Identifying Your Option Type

How to Tell

The grant document usually states the type explicitly:

- "Incentive Stock Option" or "ISO" → Tax-advantaged, $100K limit, AMT risk

- "Nonqualified Stock Option" or "NSO" or "Nonstatutory" → Ordinary income at exercise

If unclear, check the plan name (e.g., "2020 Incentive Plan" may offer both) or ask HR.

| Type | Tax at Exercise | Holding Period for Favorable Treatment |

|---|---|---|

| ISO | None (if held); AMT may apply | 2 years from grant + 1 year from exercise |

| NSO | Ordinary income on spread | 1 year from exercise for LTCG on appreciation |

Related Guides: ISO vs NSO guide, AMT planning.

Figure 3: Post-termination exercise window — 90 days standard, good leaver exceptions.

Action Checklist: Your First Grant Review

Frequently Asked Questions

What if my grant doesn't specify the post-termination exercise window?

Answer: It's usually in the plan document, not the award letter. Request the full plan from HR or your equity administrator (Carta, etc.). The plan governs.

Can I negotiate the terms of my equity grant?

Answer: Strike price and vesting are typically non-negotiable (set by board/409A). Some companies negotiate number of shares, acceleration, or extended exercise for executives. For most employees, terms are fixed.

What is the difference between the award letter and the plan document?

Answer: The award letter summarizes your specific grant. The plan document contains the full legal terms—acceleration, good leaver provisions, expiration rules. The plan overrides the letter if there's a conflict.

How often is the 409A valuation updated for private companies?

Answer: At least annually, and after material events (funding, product launch, etc.). Your equity administrator can provide the current 409A.

Where do I find my grant document?

Answer: Your company's equity platform (Carta, E*TRADE, Fidelity, Shareworks, etc.) or from HR. You should receive it at grant and can access it anytime.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRS Publication 525 | Reference | https://www.irs.gov/publications/p525 |

| IRC Section 409A | Reference | https://www.law.cornell.edu/uscode/text/26/409A |

| Carta Grant Guide | Educational | https://carta.com/blog/understanding-your-equity-grant |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Tax laws vary by jurisdiction and change frequently. Always consult a qualified tax professional (CPA, tax attorney, enrolled agent) before making decisions based on this information. The authors accept no liability for actions taken based on this content.