Executive Summary

How do I report an RSU stock sale without paying tax twice?

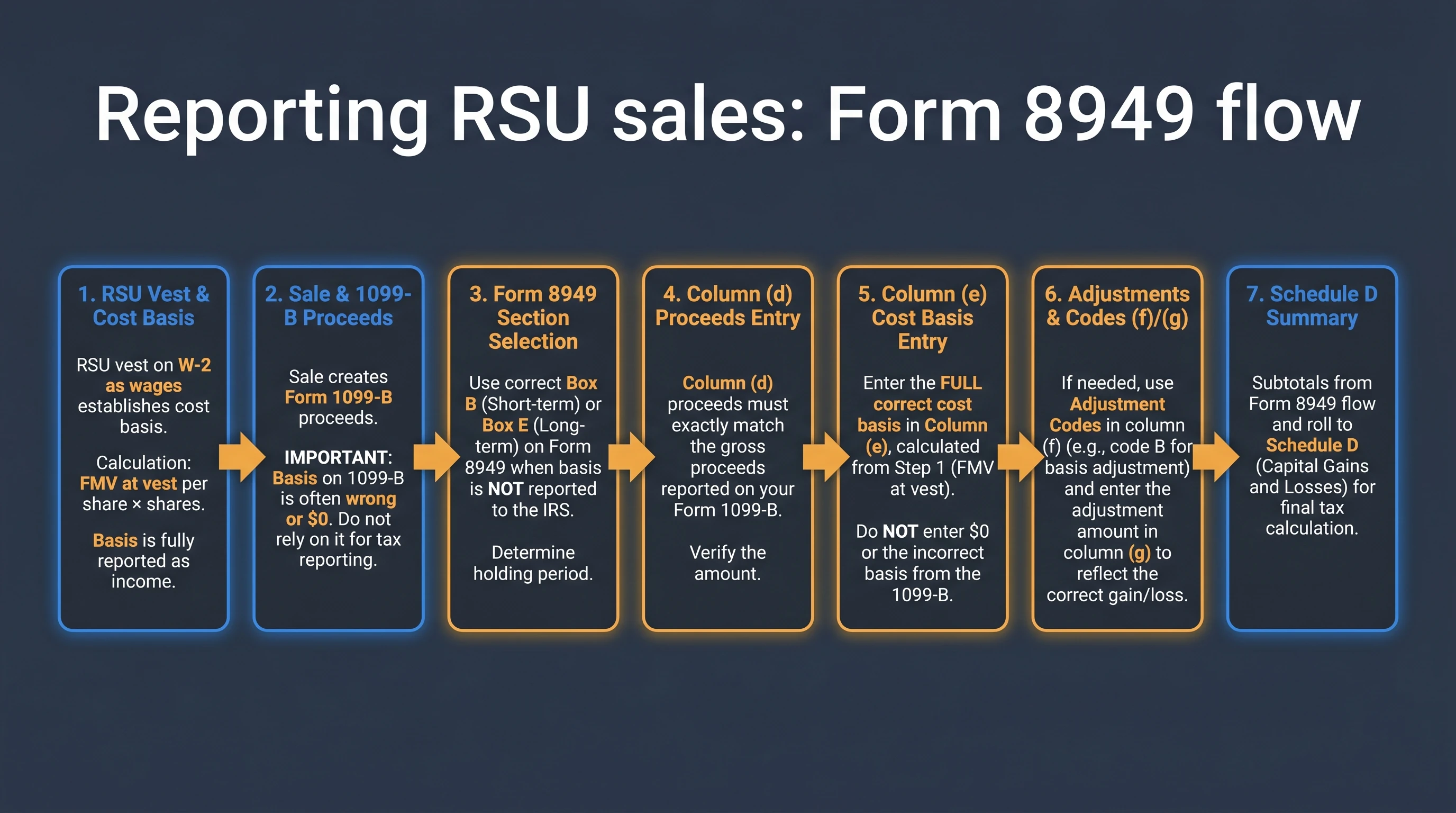

Report the proceeds shown on Form 1099-B in Form 8949 column (d) as the IRS instructs reconcilers to do. In column (e), enter your true cost basis—usually the FMV taxed as wages when the RSUs vested (documented via W-2 and employer statements)—not the incomplete number the broker may print. Adjust in columns (f) and (g) when directed by the instructions. Carry Form 8949 totals to Schedule D.

If you pasted “how to report RSU sale form 8949” into a search engine at 11 p.m. in April, you are not alone. RSUs produce a clean story in the abstract—ordinary income at vest, capital gain on later sale—but broker statements obsess over trades, while the wage inclusion lives on payroll paperwork. IRS Form 8949 exists precisely to splice those worlds together before Schedule D summarizes the tournament bracket.1

Pair this procedural guide with the RSU Adjusted Cost Basis Calculator (Form 8949) (interactive calculator plus step-by-step basis adjustment), the RSU Tax Basis Adjuster guide, RSU income on your full Form 1040 (how vesting wages fit before you get to the sale), our deep cost basis troubleshooting article for theory, How to Avoid IRS CP2000 Notices on RSU and ISO Sales if matching errors already triggered a notice, Form 1099-B basics for intuition, and the full RSU tax guide for lifecycle context.

The bottom line: You are not debating whether RSU vesting happened—the IRS cares that proceeds match the broker filing while basis reflects economics already taxed elsewhere.2

Critical Warning: Tax software autopilot loves to import

$0basis from brokerage feeds. If you blindly accept it, Schedule D may show fictitious gains and you may overpay—even though the vest income already appeared on Box 1 of your W-2.3

The Three Artifacts Employees Must Align

Modern RSU sales routinely touch three contemporaneous snapshots, none of which tell the entire truth alone:

| Artifact | Typical RSU relevance | Fail mode |

|---|---|---|

| Form W-2 | Includes wage income equal (before payroll quirks) to aggregate FMV of vested shares taxed as wages | Employee ignores it when staring at brokerage import |

| Form 1099-B | Lists proceeds per sale; basis may omit compensation layer | Imported as gospel |

| Equity administrator PDF | Per-vest FMV/share, share counts, sell-to-cover withholding | Forgotten inside a folder named “old laptop” |

Planning move: Save supplemental equity statements the month they arrive; they outperform memory when TurboTax prompts for “purchase date acquired.” For sell-to-cover mechanics, revisit sell-to-cover withholding so you reconcile net share sales versus whole vest economics.

Why Form 8949 Exists Before Schedule D

The IRS explains that Form 8949 reconciles amounts reported on Form 1099-B (or substitutes) with amounts you enter on your return, then totals flow forward to Schedule D for aggregate netting.4 Employees who misread Form 8949 can still land on plausible Schedule D numbers momentarily—but the IRS downstream matching compares capital gain detail versus broker data, so skipping proper boxes/codes attracts CP2000-style friction.

Think of Schedule D as the dashboard—Form 8949 is the line-item reconciliation. If Schedule D asks for Form 8949 attachment, omission is deliberate noncompliance absent an applicable IRS exception summarized below.

Picking Short-Term (Part I) vs Long-Term (Part II)

Holding period determines whether trades belong in Part I (short-term) or Part II (long-term):

- Generally short-term if held one year or less.

- Generally long-term if held more than one year.

Instructions specify you begin counting the day after you receive the shares (acquisition date) through the disposition date inclusively—which matters for cliff vest bursts where your first sale arrives 366 days minus one weekend vs exactly 366.5

| Fact pattern | Acquisition date anchor | Typical bucket |

|---|---|---|

| Classic single tranche vest + immediate sale months later | Settlement into brokerage | Likely Part I Box B/E until one-year milestone |

| Hold post-vest one year plus one day | Same vest/settlement timestamp | Moves to Part II Box E/K pattern |

| Multiple vests aggregated into sold lot ID | Separate rows per disposition if facts differ | Software may summarize only if justified |

If your broker labeled short/long term incorrectly on Form 1099-B Box 2, you fix via your records consistent with IRS instructions rather than blindly copying theirs.6

Digital asset quirks (Boxes G/L, etc.) do not apply to classic employer RSUs—but keep PDF instructions handy if brokers merge crypto with stock activity on one consolidated statement.

Choosing the Correct Checkbox Box at the Top of Part I / Part II

Most RSU nightmares cluster around basis not reported to IRS on Form 1099-B even when brokers show a nominal number to you—which maps to IRS narrative for Part I Box B (short) or Part II Box E (long).7

Conversely Box A / Box D cover situations where brokers affirm basis was reported to the IRS and you mainly mirror their columns unless adjustments apply. Mis-checking wastes hours when tax software clones the wrong totals.

Use this employee-centric decision grid (always confirm your actual 1099-B checkboxes each year—the IRS reorganizes captions periodically):

| 1099-B signals (conceptual) | Likely Form 8949 column treatment | Checkbox family |

|---|---|---|

Basis missing or $0; “noncovered” language | Columns (e)/(g) need your reconstructed wage basis | Part I Box B / Part II Box E |

| Basis forwarded to IRS; matches vesting comps | Possibly Box A/D with fewer adjustments—verify Exception 1 | Part I Box A / Part II Box D |

| No broker statement issued (manual private sale analog) | Part I Box C / Part II Box F (uncommon for Nasdaq RSUs) | Rare for standard plans |

If you qualify for IRS Exception 1—all statements show IRS-reported basis, no adjustments—you may aggregate directly onto Schedule D line 1a/8a and skip granular Form 8949 rows altogether. Equity employees rarely qualify without manual fixes, but read the bullets each filing season anyway.8

Column-by-Column Sanity Check for RSUs

Column (a) Description

Name the security ticker, number of shares, and reference “RSU vested [date range]”—future-you audits thank present-you.

Columns (b) and (c) Dates acquired / sold

Acquisition date anchors to delivery/settlement absent unusual facts. Sale date mirrors broker confirmations.

Column (d) Proceeds

Always match Form 1099-B totals per IRS reconciliation mandate when you receive the form—exceptions are narrowly technical.9

Column (e) Cost or other basis

For typical RSUs, basis starts at aggregate FMV taxed as ordinary income attributable to shares sold—not 0, not strike (there is none), not random cost from employer stock purchase plans.

Worked example:

Vest taxable wages for tranche sold: 240 shares × $190.42 FMV/share = $45,700.80

Later sale proceeds: $52,830.90 (broker column d)

Rough pre-adjustment gain: $52,830.90 − $45,700.80 ≈ $7,130.10 long-term vs short depending on clocks

If you sold fewer than vested shares earlier in the year via sell-to-cover, basis allocation still tracks FIFO or plan-specific layering spelled in plan docs—coordinate with supplemental statements rather than naive averaging.

Columns (f)/(g)/(h)—Adjustments when basis ≠ brokerage import

Instructions describe using column (g) with letter codes explaining adjustments—for example correcting basis inconsistencies or other permitted adjustments. Equity employees often cite basis correction narratives consistent with Publication 550 and Form 8949 worksheets when needed.10

Do not silently zero out column (g)—the IRS compares patterns.

Multistate Moves and Payroll Friction Before the Brokerage Ledger

Relocation mid-year splits wage sourcing (W-2 boxes) independently from brokerage sale characterization. If California or New York surfaced in your withholding story while you sold elsewhere, reconcile credit ordering separately from Form 8949 mechanics—starting point remains correct federal Schedule D storytelling. Guides: multi-state remote work equity.

Software Import Pitfalls and CP2000 Context

Popular DIY software maps broker feeds into Form 8949 automatically. Typical failure loops:

| Symptom | Likely root cause | Fix |

|---|---|---|

| Massive phantom capital gain overnight | Imported basis $0 vs wage basis | Override column (e) + document |

| Duplicate rows RSU vest/sale combos | Employer + broker simultaneous feeds | Deduplicate with broker lots |

| “Missing cost basis” flag ignored | Covered vs non-covered mislabel | Box B/E path adjustments |

Maintain a basis binder: PDF vest confirmations, supplemental tax statements (some employers label “Fair Market Value at Release”), screenshots of brokerage lot detail.

When You Truly Need Schedule D Complexity Beyond RSUs

If you concurrently trade options, ETFs, QSBS exclusions, futures on Section 1256 contracts, installment sales—Schedule D overlays additional schedules. RSU sales themselves avoid Form 4797 traps unless entrepreneurial facts appear. QSBS aficionados referencing Section 1202 still begin on Form 8949 / Schedule D with extra labels—see Section 1202 guide.

Wash Sales and Dividend Stripping Basics

Employees selling RSUs at a capital loss shortly before re-buying brokerage shares unrelated to payroll may collide with wash sale rules. RSUs themselves do not create wash sales—but post-vest open market trades do if pattern mirrors Section 1091 timelines.

Figure 1: Conceptual reconciliation path from payroll wage inclusion (vest) → broker disposition reporting → Form 8949 adjustments → Schedule D aggregation.

Frequently Asked Questions

Do RSU vesting gains go on Schedule D?

Answer: Ordinary income inclusion from vest/settlement ordinarily hits payroll Forms W-2 (and analogous state withholding), not Schedule D profit lines. Schedule D captures capital gain/loss on later sales or exchanges absent special sections. Publication 525’s framework maps compensation vs investments even though Publication 525 is not imported line-by-line like Form 8949.11

Source: IRS Publication 525

My 1099-B shows $0 cost basis—is that authoritative?

Answer: Brokers follow cost basis reporting rules that often omit vest wage components; Form 8949 instructions explicitly contemplate adjusting basis discrepancies reconciling filings.12

Source: Instructions for Form 8949

How do I calculate gain if employer used per-share rounding different than broker rounding?

Answer: Maintain employer FMV workbook as primary authoritative tie-out; pennies differences rarely move tax materially but obsessive matching prevents audit ping-pong. When immaterial deltas exist, document conservative approach.

Can I aggregate multiple RSU sales on one attachment statement?

Answer: Instructions allow aggregated statements resembling Form 8949 columns under Exception 2 subject to meticulous totals—employees with dozens of drip sells often exploit this—but QOF deferral elections explicitly forbid sloppy aggregation—irrelevant to typical RSUs.13

Will estimated tax withholding from RSU vents reduce Schedule D surprises?

Answer: Payroll withholding settles ordinary wage liabilities; insufficient withholding still surfaces via Form 1040 even if Schedule D accurately reports capital gains layered above. Coordinate via estimated tax guide.

Which VestingStrategy tool helps ballpark withholding before April?

Answer: Combine RSU tax estimator projections with brokerage realized gain exports around Q4—not perfect but directionally grounding.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| About Form 8949 | IRS form overview | irs.gov/forms-pubs/about-form-8949 |

| Instructions for Form 8949 (PDF/HTML) | Official instructions | irs.gov/instructions/i8949 |

| About Schedule D (Form 1040) | IRS schedule overview | irs.gov/forms-pubs/about-schedule-d-form-1040 |

| Publication 525 | IRS publication | irs.gov/publications/p525 |

| Publication 550 | IRS publication | irs.gov/publications/p550 |

Research note

Topic selection followed VestingStrategy’s Chief Content Officer (CCO) API (npm run cco:recommend; see docs/processes/CCO-CONTENT-RECOMMENDATIONS.md). During this run the sandbox Perplexity API quota was exhausted, so research drew from IRS primary sources fetched directly (About Form 8949, Instructions for Form 8949, Schedule D overview, Publication 525/550) plus existing site guides cited above—still aligned with the intent of docs/processes/CURSOR-CONTENT-CREATION.md, which prescribes authoritative sourcing and Gemini gemini-3-pro-image-preview infographics exported as WebP.

Disclaimer

This guide is for general education only and is not legal, tax, or investment advice. IRS forms and instructions update annually—always read current PDFs alongside your brokerage and payroll documents, or retain a CPA/EA specializing in equity compensation.

Footnotes

-

Form 8949 purpose statement emphasizes reconciliation—not optional commentary. irs.gov/forms-pubs/about-form-8949 ↩

-

Double-tax fear when basis wrong is unpacked in are RSUs taxed twice?. ↩

-

See cost basis avoid double taxation for column code orientation. ↩

-

About Form 8949 — reconciliation role. irs.gov/forms-pubs/about-form-8949 ↩

-

Holding period counting convention per Form 8949 instructions. irs.gov/instructions/i8949 ↩

-

Same citation—broker may leave Box 2 blank with code prompting manual classification. ↩

-

Box B/E descriptions for trades without adequately reported IRS basis. Instructions for Form 8949 ↩

-

Exception 1 criteria summarized in IRS instructions annually—verify bullets before relying. ↩

-

Column (d) proceeds matching unless narrow exceptions enumerated in PDF instructions—read annually. ↩

-

Column (g) adjustments + Publication 550 context for basis layering. IRS Publication 550 ↩

-

Pub. 525 overview of wages vs dividends vs capital concepts. ↩

-

Form 8949 instructions—adjustments reconcile broker vs taxpayer reality. ↩

-

Instructions—Exception 2 attached statements; carve-outs for qualified opportunity fund deferrals irrelevant here but illustrative of strict aggregation limits. ↩