Executive Summary

What is the IRS rule for an 83(b) election mailed near the deadline?

You must file a Section 83(b) election within 30 calendar days after the date property is transferred to you. If you mail the election through the U.S. Postal Service before midnight of the due date following IRS rules for a designated class of mail, IRC Section 7502 can treat the document as timely filed based on the postmark even if IRS processing arrives later—subject to statutory and regulatory details. Use Certified Mail or another method that creates a clear mailing date record, keep duplicates, and send the required employer copy separately if needed.

Anxiety around the IRS 83(b) election 30-day deadline is rational: the election is irrevocable once made, and missing the window usually means you cannot obtain the same tax timing for that transfer. This guide is intentionally narrow—deadline mechanics, mailing, postmarks, and proof—so you can execute with confidence and know when to stop self-help and call a professional.

For the full content checklist for the election statement itself (required facts, Form 15620, employer copy), pair this page with our operational guide on how to file a Section 83(b) election within 30 days and the strategic overview in Section 83(b) election: a strategic tax decision.

Scope note: Taxpayers abroad, ITIN applicants, and nonresident filers follow the same conceptual 30-day rule but often add cover letters and alternative address lines—confirm with preparers who handle international equity.

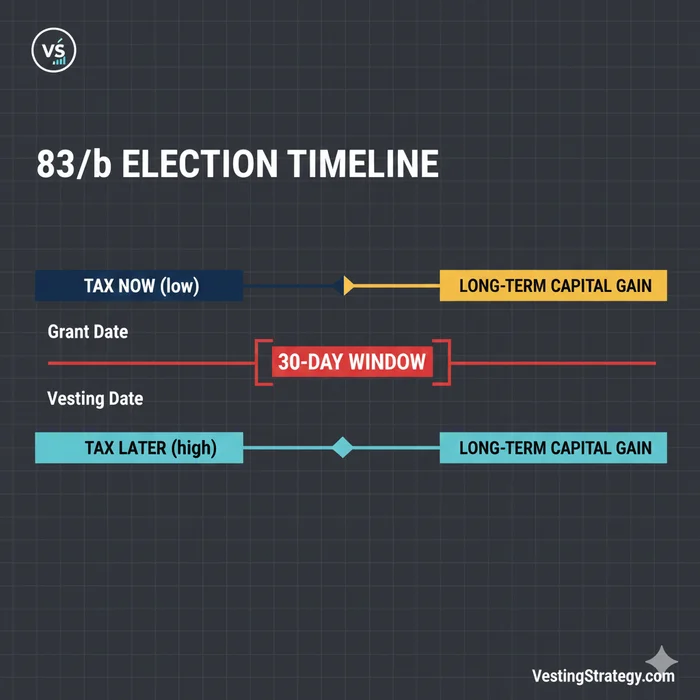

What “30 days” actually means (the transfer date)

| Question | Practical answer |

|---|---|

| When does the clock start? | On the date property is transferred to you for purposes of Section 83—commonly your restricted stock or early-exercised unvested shares issuance date reflected in plan records.1 |

| Does the grant “approval date” matter? | Only indirectly; the transfer date controls. Board or committee approval may precede issuance—do not guess which date Stock Admin will use. |

| Weekends and federal holidays | The 30th day can land on a weekend. Do not assume an automatic roll to Monday unless a specific rule applies to your delivery path. Mail early. |

| Time zones | If your company is in one state and you are in another, pin the plan’s recorded transfer date in writing (email to Stock Admin) when possible. |

Action: On the day you sign the stock purchase or exercise paperwork, ask your administrator: “What is the Section 83 transfer date that starts the 83(b) clock?”

Counting the 30-day window (checklist)

Use a written calendar count—most professionals count Day 1 as the day after transfer only if that matches their interpretive convention; the critical output is a single agreed filing due date on your calendar. If in doubt, treat earlier dates as safer and aim to file by day 25, not day 29.

| Step | Check |

|---|---|

| 1 | Obtain the confirmed transfer date from Stock Admin |

| 2 | Compute the due date on a printed calendar |

| 3 | Identify the IRS service center address used for paper filings (consistent with Regulation §1.83-2) |

| 4 | Decide mail vs. courier (see mailing section below) |

| 5 | Confirm employer/service-provider copy is sent timely as required2 |

| 6 | Prepare attachments for your Form 1040 tax year folder |

Mailing mechanics: IRS service center address

Treasury Regulation §1.83-2 requires filing the election with the IRS location referenced in the regulation (generally aligned with where you file your individual income tax returns). For a full state-by-state mailing directory (Ogden, Kansas City, Austin, and expat ZIP 73301-0215), see Where to Mail Your 83(b) Election: IRS Addresses. Addresses can shift; practitioners typically:

- Confirm the IRS Where to File resources for individuals for the tax year, and

- Prefer the printed instruction address bundled with Forms 15620 guidance over forum posts.

| Item | Why it matters |

|---|---|

| Correct campus | Wrong mailroom delays can muddy proof arguments—get the campus right |

| Recipient line | Plain English “Section 83(b) Election — [Your Name — SSN masked on outer envelope if needed per your adviser]” assists routing |

| Enclosure | Printed original signature election + concise cover sheet |

Always keep a duplicate signed PDF and a second wet-ink copy in your files.

Certified mail, tracking, and why employees use them

The Internal Revenue Code does not mandate Certified Mail for Section 83(b). In practice, Certified Mail with electronic Return Receipt (or Return Receipt requested) is widely used because it produces:

- A mailing receipt tied to the date you handed the item to USPS, and

- Tracking artifacts you can retain for years (PDF exports from USPS tools).

| Method | Strengths | Weaknesses |

|---|---|---|

| USPS Certified Mail | Familiar; strong cultural acceptance by preparers; proof of acceptance at post office | Must still follow timely-mailing rules for postmark treatment |

| USPS Priority / Express | Speed; tracking | Not all services produce a postmark that fits Section 7502 analysis—validate with counsel if cutting close |

| Designated private delivery (designated list) | Signature and tracking | Section 7502 treatment differs from USPS postmarks—use only with clear professional guidance near deadlines |

| Hand delivery | Physical control | Less common; document chain of custody if used |

Do not rely on “the envelope was stamped on time” stories from social media—your evidence package should be boring and documentary.

Postmarking & IRC Section 7502 (timely mailing treated as timely filing)

High-level rule: For certain documents mailed to the IRS through the U.S. Postal Service, Section 7502 can treat a document as filed on the postmark date if it is delivered after the due date—when the statutory conditions are met.3

| Concept | Reader translation |

|---|---|

| Timely postmark vs. timely receipt | You may be protected if the postmark is on or before the due date in qualifying USPS mailings—do not assume the rule extends to every carrier scan line |

| Electronic postmarks | There are rules for electronic postmarks offered by authorized providers—advanced planning only |

| What you should do | File with margin; if you must cut it close on day 30, involve a tax attorney or CPA firm before relying on intricate Section 7502 fact patterns |

Important: Courts and the IRS dissect Section 7502 fact patterns. This article summarizes the commercial reason Certified Mail matters—it helps establish external, third-party corroboration of your mailing—not a guarantee.

Employer / service-provider copy rules (separate deadline concern)

Treasury Regulation §1.83-2 also expects you to furnish a copy to the person for whom you performed services (typically your employer).4

Treat this as its own mini-project:

| Task | Recommendation |

|---|---|

| Method | Secure upload via Stock Admin portal plus emailed PDF confirmation when available |

| Timing | Aim to satisfy “furnish” contemporaneously—do not mail only to IRS and assume equity platform notices substitute |

| Evidence | Screenshots with timestamps, ticket numbers, upload confirmations |

If you missed the employer copy step but nailed the IRS copy, do not DIY-fix retroactive characterization—talk to counsel.

Electronic filing caveat

As of commonly available IRS instructions, practitioners typically file Section 83(b) elections on paper. If future IRS digital channels formally accept §83(b) elections, Stock Admin—not Twitter—will announce adoption. Assume paper + proof unless your counsel confirms otherwise.

Related compliance you should still plan for

| Parallel obligation | Typical timing |

|---|---|

| Attach copy to Form 1040 for transfer year | Per Regulation §1.83-2 requirement—attach with paper or follow e-file practitioner workflow5 |

| Pay any tax associated with bargain element | Driven by FMV − amount paid; coordinate estimated payments |

| State/local conformity | Separate analysis—California and other jurisdictions have their own sourcing and reporting wrinkles |

If you relocate internationally shortly after granting, scan Section 83(b) for expats for jurisdictional breadcrumbs (not individualized advice).

What happens if you miss the 83(b) deadline

| Scenario | Typical outcome |

|---|---|

| IRS receives election on day 31 | Election generally invalid for that transfer; taxation defaults to ordinary timing under Section 83(a) at vesting (or as otherwise applicable) |

| You discover miss months later | No standard administrative “fix”; explore private letter ruling only under rare, expensive facts with counsel |

| Company says “we will backdate” | Tax law does not recharacterize property transfer dates to suit convenience—escalate |

Emotional but true: “I had good intentions” is not a Section 83(b) extension ground in routine practice.

Can I fix a Section 83(b) election filed one day late?

In routine practice you should assume a filing after the 30-day period is ineffective for obtaining Section 83(b) treatment on that transfer. Some taxpayers explore private letter rulings under narrow, expensive factual paths with tax counsel—that is not a DIY internet workflow. Immediately involve a qualified professional to model tax impacts without an election.

Actionable pre-flight checklist (print this)

- Confirm transfer date in writing from Stock Admin

- Complete Form 15620 (or attorney-drafted equivalent) with exact FMV and share counts

- Sign and date the election; consider blue ink if your adviser's office prefers scanning clarity

- Mail IRS original with Certified Mail (or method your counsel approves) before the due date

- Upload / email employer copy with receipt evidence

- Store PDF + physical copy in permanent records

- Flag your CPA to attach to the correct year return

Related reading

- IRS 83(b) Election 30-Day Rule: Official Guide — procedural step-by-step for the statutory 30-day rule, Form 15620, and Certified Mail

- How to File an Official Section 83(b) Election with the IRS — Form 15620 language, service-center addresses, execution checklist

- 83(b) Election Deadline & Mailing Tracker — interactive calendar for your last filing day and Certified Mail steps

- IRS 83(b) Election Form Generator & Mailing Checklist — interactive draft letter plus Certified Mail workflow

- How to file a Section 83(b) election within 30 days — required contents and common mistakes

- Why you cannot file an 83(b) election for standard RSUs — award-type traps

- Early exercise strategies — when early exercise triggers this workflow

- AMT planning for stock options — ISO/AMT interaction after early exercise

Footnotes

Primary sources (quick reference)

| Source | URL |

|---|---|

| IRC Section 83(b) | Cornell LII |

| Treasury Regulation §1.83-2 | Cornell LII CFR |

| IRC Section 7502 | Cornell LII |

| IRS Form 15620 | IRS PDF |

Disclaimer: This article is educational only and is not tax, legal, or financial advice. Section 83(b) elections are irrevocable, can accelerate tax, and interact with AMT, state taxes, and immigration status. Confirm every deadline, address, and delivery method with a qualified CPA, enrolled agent, or tax attorney before you mail or upload anything.

Footnotes

-

Transfer timing is a facts-and-circumstances determination under Section 83; see Treasury Regulation §1.83-3 and related rules for property definitions. ↩

-

Treasury Regulation §1.83-2 describes filing with the IRS, providing copies, and attaching to the individual income tax return. ↩

-

IRC Section 7502; see also Treasury Regulation §301.7502-1 for timely mailing treated as timely filing (statutory and regulatory conditions apply). ↩

-

Treasury Regulation §1.83-2(a) and related copy provisions—confirm current text with primary sources. ↩

-

Treasury Regulation §1.83-2(d) (attach copy to return for year property is transferred). ↩