Executive Summary

Where can I get an IRS 83(b) election form template I can actually file?

Most practitioners start from IRS Form 15620 or an equivalent signed statement listing the taxpayer, property, transfer date, taxable year, restrictions, FMV (without regard to restrictions), and amount paid, plus proof copies went to the employer as Treasury Regulation §1.83-2 requires. Use the generator on this page to pre-fill those narrative slots, then finalize wording with your CPA or tax attorney.

Searches for 83(b) election form template, official IRS language, and 30-day mailing proof usually mean one thing: you already decided (with advice) to accelerate income recognition, and now you need operational certainty before the statutory window closes.

This guide closes the gap between strategy articles and envelope-ready execution:

| Reader stage | What this page adds |

|---|---|

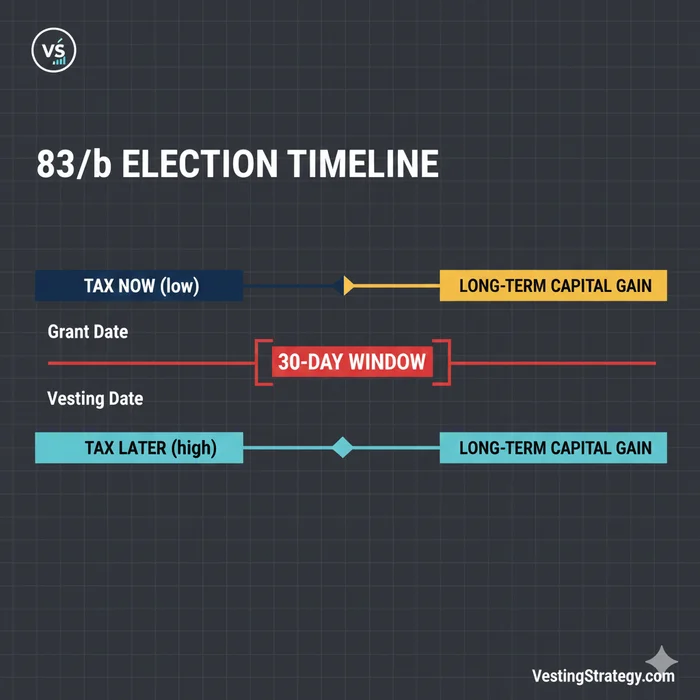

| Strategy | Economics remain in Section 83(b) election: strategic overview and 83(b) break-even tool |

| Checklists | Narrative filing steps stay in How to file an 83(b) within 30 days |

| Deadline law | Certified mail + IRC §7502 nuances live in Official 83(b) 30-day deadline & mailing rules |

| Deadline math | Section 83(b) Election Deadline Calculator — last filing day + PDF letter |

| Official filing | How to file an official Section 83(b) with the IRS — Form 15620 language, campuses, Certified Mail |

| Mailing addresses | Where to Mail Your 83(b) Election: IRS Addresses — 50-state directory + expat ZIP |

| All-in-one hub | IRS Section 83(b) mailing address & checklist — deadline tracker + address + generator |

| Execution | Interactive generator + mailing checklist directly below |

Why “template” searches need a generator—not a static PDF

Is downloading a random 83(b) template PDF safe?

Unvetted PDFs may omit required facts, use outdated IRS addresses, or mismatch your grant’s actual restrictions and FMV methodology. Prefer IRS Form 15620 or counsel-reviewed language, then personalize numbers from Stock Administration and your 409A report.

| Approach | Strength | Risk |

|---|---|---|

| IRS Form 15620 | Structured prompts aligned with Service expectations | Still requires accurate FMV + narrative attachments |

| Law firm starter forms | Often vetted for completeness | Licensing / customization still required |

| Random SEO PDFs | Fast | Address drift, incomplete disclosures, wrong facts |

| This generator | Fills narrative gaps interactively | Not a substitute for professional review |

Digital filing reminder: IRS publishing cycles occasionally add electronic submission pathways for Form 15620. If your counsel selects e-file, follow IRS.gov instructions for the active tax year—do not also mail a duplicate unless instructed.

Interactive generator & Certified Mail checklist

Interactive Section 83(b) election letter (draft)

Fill in the fields below to generate election language aligned with the informational items commonly included under Treasury Regulation §1.83-2. This is not personalized tax advice — have a CPA or tax attorney review facts, valuation, and filing method before you file.

Taxpayer

Your TIN stays in this browser tab only — nothing you type here is sent to VestingStrategy servers.

Property & employer copies

IRS mailing address — verify before you seal the envelope

Treasury Regulation §1.83-2 requires filing with the Internal Revenue Service location where you file your federal income tax returns. The campus and ZIP+4 can change by tax year and filing category, so pull the address from the current IRS instructions for Form 15620 (PDF) or the "Where To File" tables in the Form 1040 instructions that match your residency and whether you are enclosing a payment.

On the envelope, many preparers write a routing line such as: ATTN: Section 83(b) Election — [Your name]

Certified Mail execution checklist (paper filing)

Toggle items as you complete them. Certified Mail is widely used to document the mailing date for IRS correspondence — it does not lengthen the statutory 30-day window.

Preview generated letter text

Election Under Section 83(b) of the Internal Revenue Code The undersigned taxpayer hereby elects under Section 83(b) of the Internal Revenue Code to include in gross income as compensation the excess (if any) of the fair market value of the property described below over the amount paid for such property, determined as of the date the property was transferred. 1. Name of taxpayer: [your legal name] 2. Address of taxpayer: [street, city, ST ZIP] 3. Taxpayer identification number: [SSN or ITIN] 4. Description of property with respect to which the election is made: [number of shares] shares of [class of shares] stock of [issuer legal name]. 5. Date on which property was transferred: [transfer date] 6. Taxable year for which election is made: 2026 7. Nature of restrictions to which the property is subject: [describe vesting, repurchase, forfeiture, etc.] 8. Fair market value at time of transfer (determined without regard to restrictions): [FMV per share on transfer date] 9. Amount paid for the property: [total amount paid for the shares] The undersigned taxpayer will file this election with the Internal Revenue Service office with which the taxpayer files their annual federal income tax returns no later than 30 days after the date the property was transferred to the taxpayer. Copies of this election have been furnished to the person for whom the taxpayer performed the services as required under Treasury Regulation §1.83-2(d): [employer / service recipient] [employer mailing address] Signature of taxpayer: ________________________________ Date signed: ________________________________ ( Sign and date after printing — ink signature typically required for paper filing )

Pair the letter with economics (before you accelerate income)

| Question | Resource |

|---|---|

| Does paying tax now beat deferring? | 83(b) Election Break-Even Calculator |

| What triggers the 30-day clock? | How to file an 83(b) within 30 days |

| How does Certified Mail intersect with IRC §7502? | 83(b) mailing rules guide |

Critical Warning: Section 83(b) elections are generally irrevocable. If the stock forfeitures or fails, prepaid tax is usually not refundable—model downside cases before filing.

Footnotes

Primary sources

| Source | Why it matters |

|---|---|

| IRC §83(b) | Statutory authority for the election |

| Treas. Reg. §1.83-2 | Mandatory statement contents & copy procedures |

| IRS Form 15620 PDF | Standardized election format |

| IRS Publication 525 | Plain-language supplement—not a substitute for regulations |

| IRC §7502 | Timely mailing treated as timely filing (qualified mailings) |

Disclaimer: This article is for education only and is not tax, legal, or financial advice. Interactive outputs are drafts for discussion with a qualified professional; VestingStrategy does not verify your facts, valuation, or filing method.