Executive Summary

What is a vesting schedule and how does the cliff work?

A vesting schedule determines when you earn the right to your equity. The most common structure is 4 years with a 1-year cliff: nothing vests for the first 12 months, then 25% vests at the cliff, followed by roughly 1/48th per month for the remaining 36 months. If you leave before the cliff, you typically forfeit all unvested equity.

Your vesting schedule controls when you actually earn your equity—and what happens to it in a merger, acquisition, or when you leave. Misunderstanding acceleration clauses has cost employees millions when single-trigger vesting created massive tax bills at deal close, or when double-trigger left them with nothing after an acquirer layoff.1 This guide explains the mechanics.

If you landed here from double trigger vesting, double trigger acceleration, or single trigger vs double trigger: single-trigger acceleration usually means one event (often a change of control) vests some or all unvested equity; double-trigger typically requires change of control plus a second event (commonly involuntary termination within a window). Exact definitions are in your plan and grant—see also RSU double trigger: IPO vs M&A.

The bottom line: Know your cliff date, your monthly vest rate, and whether you have single or double-trigger acceleration. These terms are often buried in plan documents.2

Critical Warning: Single-trigger acceleration vests all unvested equity when the deal closes—creating a large ordinary income tax bill in that year. Double-trigger only vests if you're terminated after the deal, which can leave you with nothing if the acquirer keeps you but doesn't accelerate.3

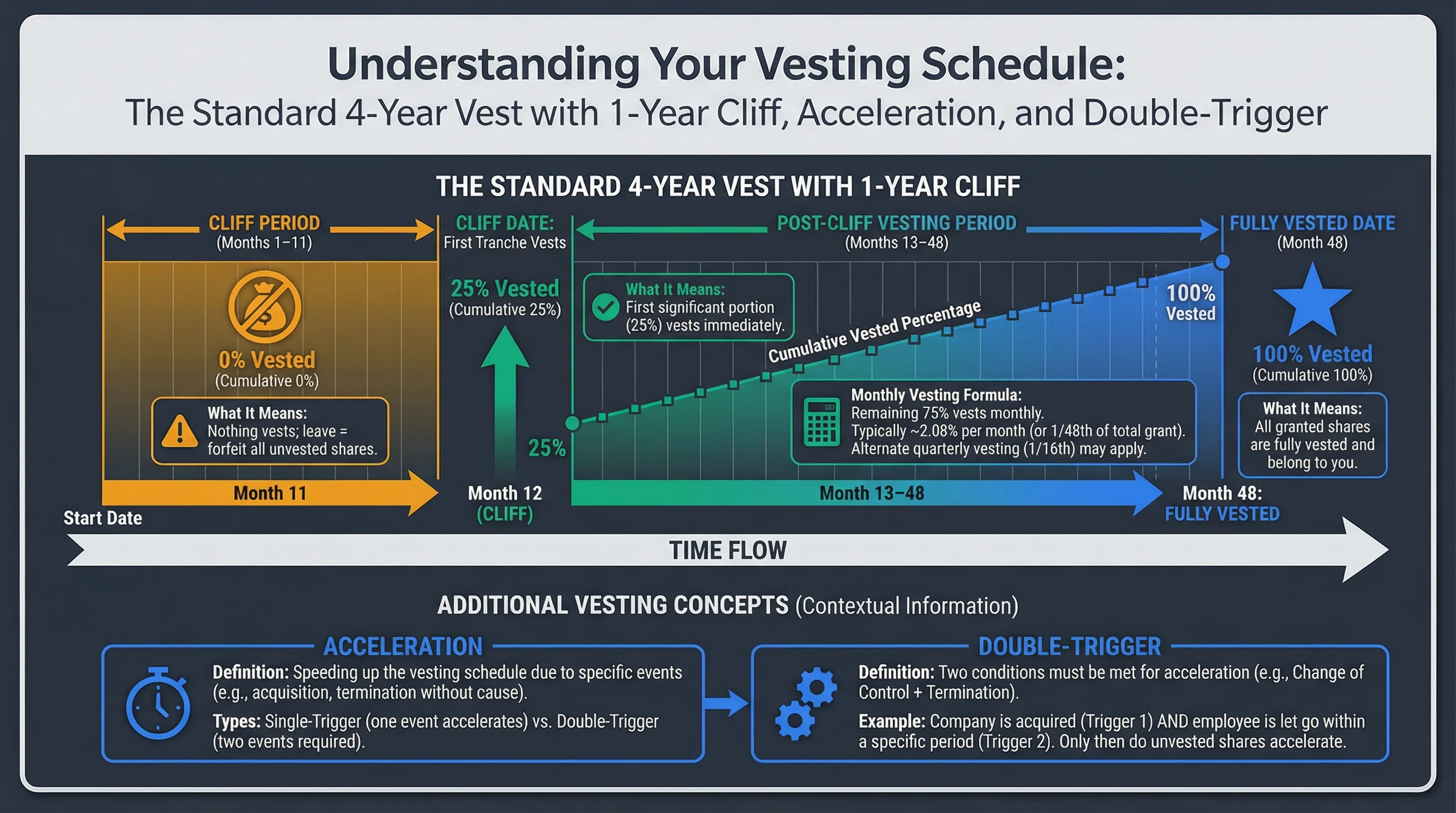

The Standard 4-Year Vest with 1-Year Cliff

How It Works

| Period | Vesting | Cumulative | What It Means |

|---|---|---|---|

| Months 1–11 | 0% | 0% | Nothing vests; leave = forfeit all |

| Month 12 (cliff) | 25% | 25% | First tranche vests |

| Months 13–48 | ~2.08% per month | 100% | Remaining 75% vests monthly |

Formula: After the cliff, you typically vest 1/48th of the total grant each month (or 1/16th quarterly, depending on plan).

Figure 1: Standard 4-year vest with 1-year cliff — when you vest.

Why the Cliff Exists

The cliff aligns incentives: it discourages short-term hires and rewards employees who stay at least one year. Companies use it to reduce turnover in the critical first year. For a simpler explanation, see our What is a vesting cliff? guide.

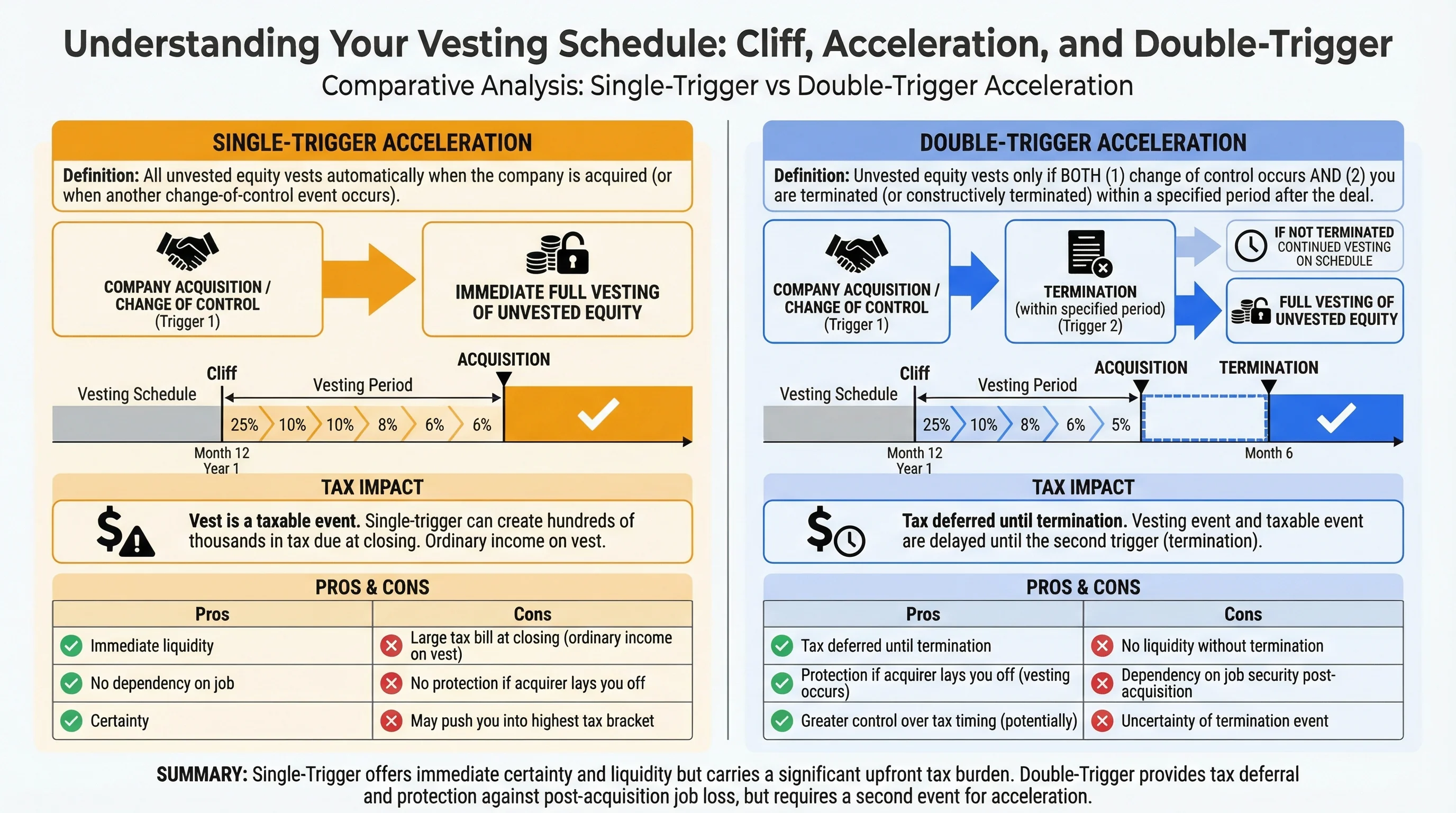

Single-Trigger vs Double-Trigger Acceleration

Single-Trigger Acceleration

Definition: All unvested equity vests automatically when the company is acquired (or when another change-of-control event occurs).

| Pros | Cons |

|---|---|

| Immediate liquidity | Large tax bill at closing (ordinary income on vest) |

| No dependency on job | No protection if acquirer lays you off |

| Certainty | May push you into highest tax bracket |

Tax impact: Vesting is a taxable event. Single-trigger can create hundreds of thousands in tax due at closing.

Double-Trigger Acceleration

Definition: Unvested equity vests only if BOTH (1) change of control occurs AND (2) you are terminated (or constructively terminated) within a specified period after the deal.

| Pros | Cons |

|---|---|

| Tax deferred until termination | No acceleration if acquirer keeps you |

| Protects against acquirer layoffs | Uncertainty—you may get nothing |

| Common for rank-and-file | Executives often negotiate enhanced terms |

Typical trigger window: 12–24 months after deal close. If you're terminated in that window, unvested equity vests.

Source: Stock Options in M&A guide

Figure 2: Single-trigger vs double-trigger — when unvested equity vests in M&A.

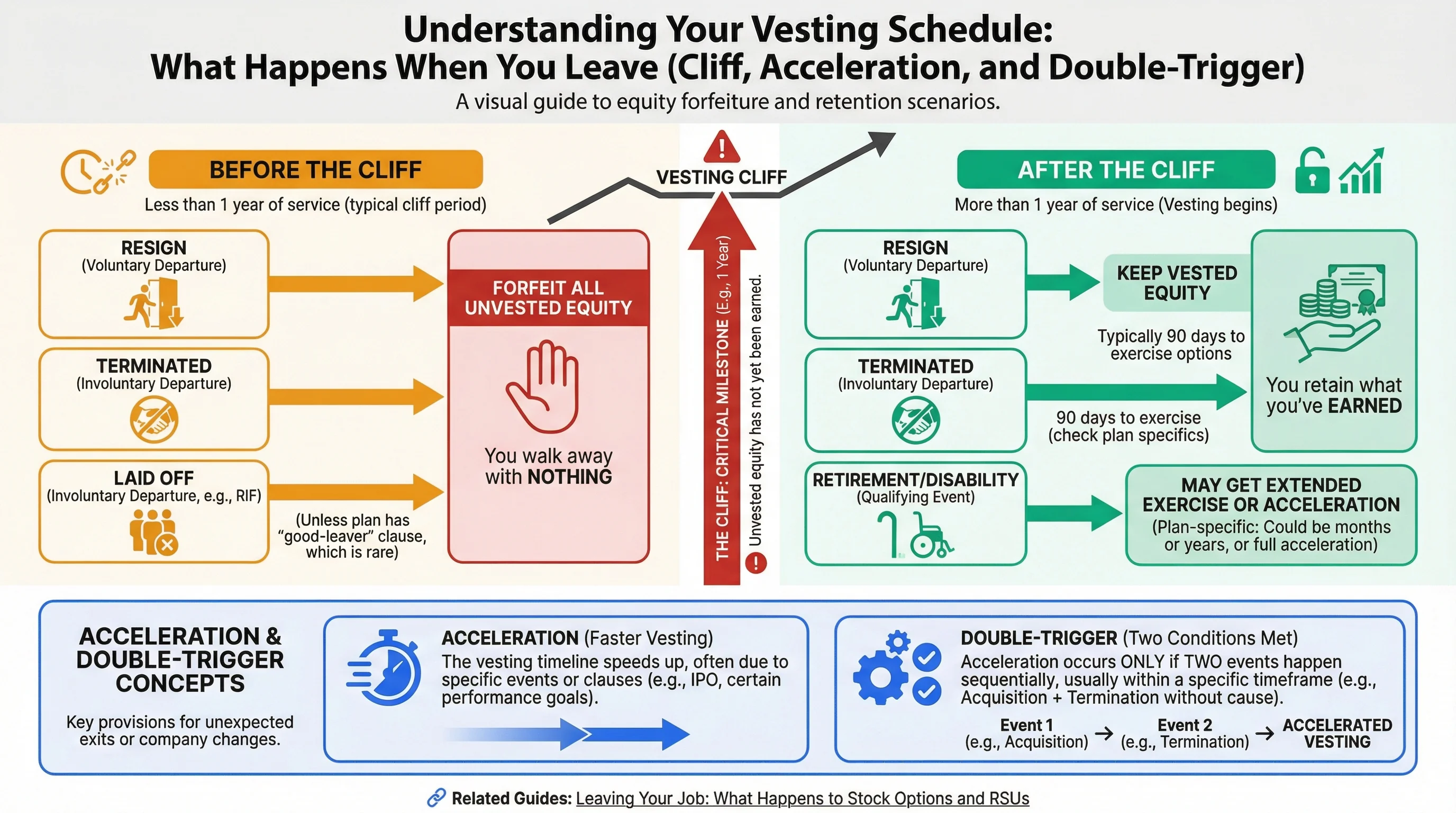

What Happens When You Leave

Before the Cliff

| Scenario | Outcome |

|---|---|

| Resign | Forfeit all unvested |

| Terminated | Forfeit all unvested |

| Laid off | Forfeit all unvested (unless plan has good-leaver clause) |

After the Cliff

| Scenario | Outcome |

|---|---|

| Resign | Keep vested; typically 90 days to exercise options |

| Terminated | Keep vested; 90 days to exercise (check plan) |

| Retirement/Disability | May get extended exercise or acceleration (plan-specific) |

Related Guides: Leaving Your Job: What Happens to Stock Options and RSUs.

Good Leaver vs Bad Leaver

Some plans distinguish between good and bad leavers:

| Leaver Type | Examples | Typical Treatment |

|---|---|---|

| Good leaver | Retirement (55+), disability, death, mutual agreement, layoff | Extended exercise (1–10 years); sometimes acceleration |

| Bad leaver | Resignation, termination for cause | Standard 90-day window; no acceleration |

Negotiation: Executives often negotiate good-leaver status for voluntary resignation with notice.

Figure 3: Good leaver vs bad leaver — exercise window differences.

Action Checklist

Frequently Asked Questions

Can I negotiate my vesting schedule?

Answer: Uncommon for rank-and-file. Executives sometimes negotiate shorter cliffs (6 months), faster vesting, or double-trigger acceleration. New hires have the most leverage.

What if my company extends the cliff?

Answer: Plan amendments can change future vesting. Typically, already-vested amounts are protected. Check your plan document and any amendment notices.

Does acceleration apply to RSUs and options the same way?

Answer: Generally yes—both can have single or double-trigger. RSUs vest as shares; options vest as exercisable rights. Tax treatment differs (RSUs taxed at vest, options at exercise).

What is "modified single-trigger"?

Answer: A hybrid: partial acceleration on deal close (e.g., 50% of unvested), with the rest on double-trigger. Reduces tax hit while providing some protection.

How do I find my acceleration terms?

Answer: Check your equity plan document and grant agreement. HR or your equity administrator (Carta, etc.) can provide copies.

Footnotes

Primary Sources

| Source | Type | URL |

|---|---|---|

| IRC Section 424 | Reference | https://www.law.cornell.edu/uscode/text/26/424 |

| Stock Options in M&A | Guide | Stock Options in M&A |

| Carta Vesting Guide | Educational | https://carta.com/blog/vesting-schedules |

Disclaimer: This guide discusses legal tax optimization strategies only. Tax evasion is illegal and is never recommended. This content is for educational purposes and does not constitute tax, legal, or financial advice. Always consult a qualified tax professional before making decisions based on this information.