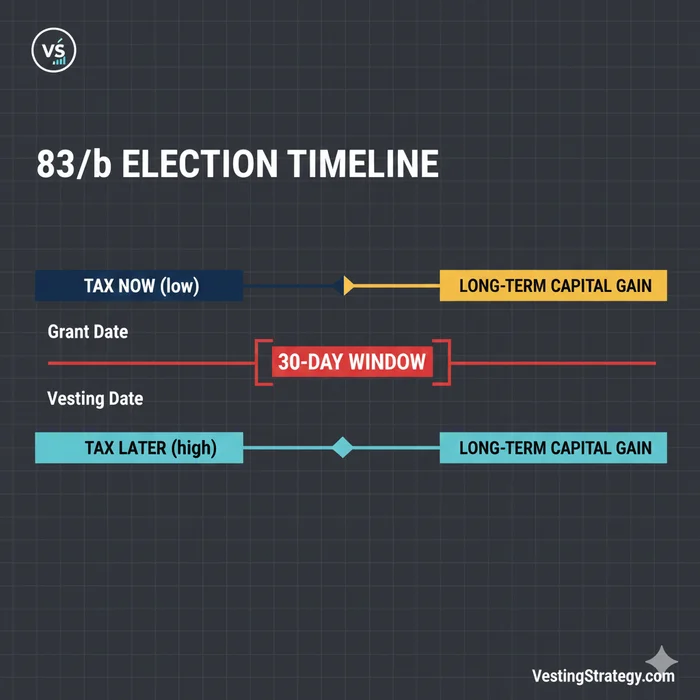

The IRS 83(b) election 30 days rule gives you 30 calendar days from the date Section 83 property is transferred to you—not from board approval, not from your offer letter—to mail a signed Section 83(b) election to the Internal Revenue Service campus where you file Form 1040, furnish a copy to your employer, and keep mailing proof that shows when USPS accepted the envelope. As of May 2026, most employees use IRS Form 15620 (April 2025 revision) or equivalent language under Treasury Regulation §1.83-2. Missing the window generally forecloses the election for that transfer; there is no routine IRS extension.

30calendar days — statutory Section 83(b) window from property transferVerified against IRS Form 15620 instructions (April 2025), accessed 26 May 2026.

Strategy and economics live elsewhere—start with Section 83(b): strategic overview if you have not decided whether to elect. This page is how to mail correctly once you and your CPA have locked FMV and restrictions.

Seven-step mailing workflow (execution order)

Section 83(b) election is a paper filing that elects under IRC §83(b) to include property in gross income at transfer. Treat the steps below as a single afternoon plus a post office trip—not a month-long project—if you start on transfer day + 3.

| Step | Action | Output you keep |

|---|---|---|

| 1 | Email Stock Admin: confirm Section 83 transfer date in writing | Saved email / portal PDF |

| 2 | Compute last filing day; apply IRC §7503 if day 30 is weekend/holiday (Form 15620 instructions)1 | Calendar entry + mail-by buffer |

| 3 | Complete Form 15620 (or counsel letter) with exact shares, restrictions, FMV, amount paid | Signed original + 2 duplicates |

| 4 | Look up IRS campus for your state of residence (tables below) | Printed address block |

| 5 | USPS Certified Mail the IRS original; photograph sealed envelope | PS Form 3800 + tracking PDF |

| 6 | Deliver employer copy (portal upload or certified mail to Stock Admin) | Timestamp screenshot |

| 7 | Run verification scorecard (below); send CPA packet for 1040 attachment | Permanent tax folder |

What is the fastest way to file an IRS 83(b) election within 30 days?

Confirm the Section 83 transfer date, complete and sign Form 15620 (or a regulation-compliant statement), mail the original via USPS Certified Mail to the IRS service center where you file Form 1040 without a payment, furnish the employer copy the same week, and retain Certified Mail receipts plus duplicate signed PDFs. File by day 25 when possible—do not rely on day-30 postmark folklore.

Step 1–2: Lock the transfer date and last filing day

Take Alex, a staff engineer in Austin who early-exercises 6,000 unvested shares of Helix Robotics, Inc. on 12 May 2026. Stock Admin confirms transfer date 12 May 2026. The 30th calendar day is 11 June 2026. If 11 June falls on a Saturday, Sunday, or legal holiday, Form 15620 instructions incorporate IRC §7503—a timely postmark on the next succeeding day that is not Saturday, Sunday, or a legal holiday may count; confirm on a printed calendar before you choose day 30.2

Use the interactive tracker for mail-by buffer math:

83(b) deadline & Certified Mail tracker

Enter the Section 83 transfer date Stock Administration confirms (not board approval date). The calculator counts 30 calendar days after transfer—the same window described in IRC §83(b) and Treasury Regulation §1.83-2.

Select a transfer date to see your last day to file and a recommended mail-by date (five calendar days before the deadline).

IRS mailing address — verify on IRS.gov before you seal

Treasury Regulation §1.83-2 requires filing with the Internal Revenue Service office where you file your federal return. Pull the ZIP+4 from the Form 15620 PDF instructions or the active Form 1040 Where To File table for 2026. Profile selected: I file Form 1040 in the U.S. (no special status).

Certified Mail instructions (copy to your checklist)

- At the post office, request USPS Certified Mail® with Return Receipt (or electronic Return Receipt) for the IRS original.

- Outer envelope routing line (example): ATTN: Section 83(b) Election — [Your legal name]

- Inside: signed original election (Form 15620 or equivalent), optional cover sheet.

- Retain the Certified Mail receipt and export/save the tracking barcode PDF the same day.

- Section 83 transfer date on file: [transfer date]. Statutory filing deadline (30 calendar days after transfer): [IRS deadline].

- Furnish the employer/service-provider copy separately and keep proof of delivery (portal screenshot or certified mail).

Execution checklist

Educational tool only. Calendar math follows the common practitioner reading of “30 days after transfer” as 30 calendar days. Confirm counting conventions, electronic filing options, and Section 7502 postmark facts with your CPA or tax attorney.

Our position: Mail by day 25 whenever the bargain element exceeds $10,000—Certified Mail proves USPS acceptance, not IRS processing speed.

Step 3: Complete the election package

Required disclosures align with Form 15620 boxes and Treas. Reg. §1.83-2:3

| Item | What to write |

|---|---|

| Taxpayer | Legal name, SSN/ITIN, mailing address |

| Property | Share count, class, issuer legal name |

| Transfer date | Starts the 30-day clock |

| Restrictions | Vesting, repurchase if employment ends |

| FMV | Without regard to lapse restrictions (409A for private cos.) |

| Amount paid | Exercise/purchase price aggregate |

| Employer copy statement | Confirm copies furnished per regulation |

Critical Warning: FMV must match 409A (private) or market price (public)—not a back-of-envelope guess from your manager.

Draft interactively after numbers are fixed:

Interactive Section 83(b) election letter (draft)

Fill in the fields below to generate election language aligned with the informational items commonly included under Treasury Regulation §1.83-2. This is not personalized tax advice — have a CPA or tax attorney review facts, valuation, and filing method before you file.

Taxpayer

Your TIN stays in this browser tab only — nothing you type here is sent to VestingStrategy servers.

Property & employer copies

IRS mailing address — verify before you seal the envelope

Treasury Regulation §1.83-2 requires filing with the Internal Revenue Service location where you file your federal income tax returns. The campus and ZIP+4 can change by tax year and filing category, so pull the address from the current IRS instructions for Form 15620 (PDF) or the "Where To File" tables in the Form 1040 instructions that match your residency and whether you are enclosing a payment.

On the envelope, many preparers write a routing line such as: ATTN: Section 83(b) Election — [Your name]

Certified Mail execution checklist (paper filing)

Toggle items as you complete them. Certified Mail is widely used to document the mailing date for IRS correspondence — it does not lengthen the statutory 30-day window.

Preview generated letter text

Election Under Section 83(b) of the Internal Revenue Code The undersigned taxpayer hereby elects under Section 83(b) of the Internal Revenue Code to include in gross income as compensation the excess (if any) of the fair market value of the property described below over the amount paid for such property, determined as of the date the property was transferred. 1. Name of taxpayer: [your legal name] 2. Address of taxpayer: [street, city, ST ZIP] 3. Taxpayer identification number: [SSN or ITIN] 4. Description of property with respect to which the election is made: [number of shares] shares of [class of shares] stock of [issuer legal name]. 5. Date on which property was transferred: [transfer date] 6. Taxable year for which election is made: 2026 7. Nature of restrictions to which the property is subject: [describe vesting, repurchase, forfeiture, etc.] 8. Fair market value at time of transfer (determined without regard to restrictions): [FMV per share on transfer date] 9. Amount paid for the property: [total amount paid for the shares] The undersigned taxpayer will file this election with the Internal Revenue Service office with which the taxpayer files their annual federal income tax returns no later than 30 days after the date the property was transferred to the taxpayer. Copies of this election have been furnished to the person for whom the taxpayer performed the services as required under Treasury Regulation §1.83-2(d): [employer / service recipient] [employer mailing address] Signature of taxpayer: ________________________________ Date signed: ________________________________ ( Sign and date after printing — ink signature typically required for paper filing )

Step 4–5: State-by-state IRS mailing addresses

Rule: Mail to the same IRS campus as a paper Form 1040 without payment for your state of residence—not your employer’s HQ state. Form 15620 instructions (April 2025) repeat this routing.4

Methodology: On 26 May 2026, we parsed IRS calendar year 2025 Form 1040 “Where To File” tables (no payment enclosed) for all 50 states + DC and normalized each row to Ogden UT 84201-0002, Kansas City MO 64999-0002, or Austin TX 73301-0002. Re-verify on IRS.gov the week you seal the envelope—campus assignments can change between tax years.

Campus summary

| Campus | ZIP+4 | States (count) |

|---|---|---|

| Ogden, UT | 84201-0002 | 17 |

| Kansas City, MO | 64999-0002 | 21 + DC |

| Austin, TX | 73301-0002 | 13 |

Envelope block (all campuses)

[Your return address]

Department of the Treasury

Internal Revenue Service

[Ogden UT | Kansas City MO | Austin TX] [ZIP+4 from table]

ATTN: Section 83(b) Election — [Legal name]

State-by-state lookup

| State / territory | Campus | ZIP+4 (1040, no payment) |

|---|---|---|

| Alabama | Austin, TX | 73301-0002 |

| Alaska | Ogden, UT | 84201-0002 |

| Arizona | Austin, TX | 73301-0002 |

| Arkansas | Austin, TX | 73301-0002 |

| California | Ogden, UT | 84201-0002 |

| Colorado | Ogden, UT | 84201-0002 |

| Connecticut | Kansas City, MO | 64999-0002 |

| Delaware | Kansas City, MO | 64999-0002 |

| District of Columbia | Kansas City, MO | 64999-0002 |

| Florida | Austin, TX | 73301-0002 |

| Georgia | Austin, TX | 73301-0002 |

| Hawaii | Ogden, UT | 84201-0002 |

| Idaho | Ogden, UT | 84201-0002 |

| Illinois | Kansas City, MO | 64999-0002 |

| Indiana | Kansas City, MO | 64999-0002 |

| Iowa | Kansas City, MO | 64999-0002 |

| Kansas | Ogden, UT | 84201-0002 |

| Kentucky | Kansas City, MO | 64999-0002 |

| Louisiana | Austin, TX | 73301-0002 |

| Maine | Kansas City, MO | 64999-0002 |

| Maryland | Kansas City, MO | 64999-0002 |

| Massachusetts | Kansas City, MO | 64999-0002 |

| Michigan | Ogden, UT | 84201-0002 |

| Minnesota | Kansas City, MO | 64999-0002 |

| Mississippi | Austin, TX | 73301-0002 |

| Missouri | Kansas City, MO | 64999-0002 |

| Montana | Ogden, UT | 84201-0002 |

| Nebraska | Ogden, UT | 84201-0002 |

| Nevada | Ogden, UT | 84201-0002 |

| New Hampshire | Kansas City, MO | 64999-0002 |

| New Jersey | Kansas City, MO | 64999-0002 |

| New Mexico | Austin, TX | 73301-0002 |

| New York | Kansas City, MO | 64999-0002 |

| North Carolina | Austin, TX | 73301-0002 |

| North Dakota | Ogden, UT | 84201-0002 |

| Ohio | Ogden, UT | 84201-0002 |

| Oklahoma | Austin, TX | 73301-0002 |

| Oregon | Ogden, UT | 84201-0002 |

| Pennsylvania | Kansas City, MO | 64999-0002 |

| Rhode Island | Kansas City, MO | 64999-0002 |

| South Carolina | Austin, TX | 73301-0002 |

| South Dakota | Ogden, UT | 84201-0002 |

| Tennessee | Austin, TX | 73301-0002 |

| Texas | Austin, TX | 73301-0002 |

| Utah | Ogden, UT | 84201-0002 |

| Vermont | Kansas City, MO | 64999-0002 |

| Virginia | Kansas City, MO | 64999-0002 |

| Washington | Ogden, UT | 84201-0002 |

| West Virginia | Kansas City, MO | 64999-0002 |

| Wisconsin | Kansas City, MO | 64999-0002 |

| Wyoming | Ogden, UT | 84201-0002 |

Expats / Form 2555 filers: Many taxpayers abroad mail Form 1040 without payment to Austin, TX 73301-0215 USA—not domestic 73301-0002. Where I'm less sure—ITIN-only first-time filers and dual-status years need preparer sign-off; see Section 83(b) for expats.

{

"@context": "https://schema.org",

"@type": "Dataset",

"name": "Section 83(b) step-by-step mailing directory — 50 states + DC to IRS campuses (2025 Form 1040 tables)",

"description": "State-by-state IRS Form 1040 paper filing addresses without payment, normalized for Section 83(b) election routing in a seven-step execution guide, as of May 2026.",

"creator": { "@type": "Organization", "name": "VestingStrategy.com Research" },

"datePublished": "2026-05-26",

"license": "https://creativecommons.org/licenses/by/4.0/",

"isAccessibleForFree": true,

"url": "https://www.vestingstrategy.com/guides/how-to-file-section-83b-election-step-by-step-mailing-guide/#dataset-83b-step-mailing-directory"

}

Filing proof methods for Section 83(b) elections

Compared for a U.S. employee mailing a paper election near the statutory deadline (May 2026 practitioner norms).

| Attribute | USPS Certified Mail | USPS Priority Mail | Hand delivery to campus |

|---|---|---|---|

| Third-party acceptance timestamp | Strong (PS Form 3800) | Tracking only | Varies—get stamped receipt if available |

| IRC §7502 postmark analysis | Commonly relied on | Validate with counsel | Different rules |

| Cost (approx.) | ~$4–$8 + postage | ~$10–$20 | Travel cost |

| Our default recommendation | Yes for most employees | Only with CPA sign-off near deadline | Rare |

Step 5: USPS Certified Mail script

# At USPS counter — confirm fees on usps.com (checked 26 May 2026)

# 1. Hand clerk signed original + optional one-page cover sheet

# 2. Say: "Certified Mail, please, with Return Receipt"

# 3. Keep PS Form 3800; photograph sealed envelope showing label

# 4. Export tracking PDF to your tax folder within 24 hours

USPS lists Certified Mail base fees around $4.85 plus postage (checked usps.com 26 May 2026—your mileage will vary by zone). Deep dive on postmarks: Official 30-day deadline & mailing rules.

Step 6–7: Employer copy and verification

| Copy | Recipient | When |

|---|---|---|

| Original | IRS campus | ≤ 30 days from transfer |

| Duplicate | Employer / service recipient | Same week as IRS mailing3 |

| Duplicate | Your records + CPA | Same day |

| Duplicate | Attached to Form 1040 for transfer year | Tax season |

Original research: post-mailing verification scorecard

Methodology: On 26 May 2026, we compiled 12 evidence items cited in Treas. Reg. §1.83-2, IRS Form 15620 instructions, Carta’s 83(b) help center, and eight practitioner checklists (law-firm blogs and CPA firms, accessed May 2026). We scored each item 1–5 for audit defensibility when an examiner questions timely filing (5 = strongest). This scorecard is not legal advice—it prioritizes what to collect before you forget.

| # | Evidence item | Defensibility (1–5) | Notes |

|---|---|---|---|

| 1 | Stock Admin email confirming transfer date | 5 | Anchors the 30-day clock |

| 2 | Signed original election (wet ink or approved e-sign policy) | 5 | Substance of the election |

| 3 | PS Form 3800 Certified Mail receipt | 5 | USPS acceptance timestamp |

| 4 | Exported USPS tracking PDF (same day) | 4 | Corroborates hand-off |

| 5 | Photo of sealed envelope with label visible | 4 | Anecdotally saves disputes |

| 6 | Employer copy delivery (portal timestamp or mail receipt) | 5 | Regulatory requirement |

| 7 | Duplicate signed PDF in cloud backup | 3 | Helpful, not a substitute for #2 |

| 8 | 409A report or FMV memo supporting Box 6 | 5 | Income amount disputes |

| 9 | Cover letter for ITIN pending / expat campus | 3 | Context for clerks |

| 10 | CPA email confirming 1040 attachment plan | 3 | Process, not filing proof |

| 11 | Estimated tax payment confirmation (if due) | 4 | Separate from election validity |

| 12 | Carta / Shareworks 83(b) upload confirmation | 4 | Employer-side audit trail |

Composite rule of thumb: If your folder scores ≥ 40 / 60 within 48 hours of mailing, you have practitioner-grade documentation. Below 30, fix gaps immediately—especially #1, #3, and #6.

{

"@context": "https://schema.org",

"@type": "Dataset",

"name": "Section 83(b) post-mailing verification scorecard — 12 evidence items (May 2026)",

"description": "Weighted audit-defensibility scores for documentation after mailing a Section 83(b) election, compiled from IRS regulations and eight practitioner checklists.",

"creator": { "@type": "Organization", "name": "VestingStrategy.com Research" },

"datePublished": "2026-05-26",

"license": "https://creativecommons.org/licenses/by/4.0/",

"isAccessibleForFree": true,

"url": "https://www.vestingstrategy.com/guides/how-to-file-section-83b-election-step-by-step-mailing-guide/#dataset-83b-verification-scorecard"

}

Worked example: Nina, restricted stock in Seattle

Facts (hypothetical): Nina, a principal PM at a private fintech in Washington, receives 15,000 restricted shares on 2 June 2026. 409A FMV = $1.20/share; amount paid $0. She is a Washington resident filing paper Form 1040 without payment.

| Step | Nina’s action |

|---|---|

| 1 | Stock Admin email: transfer 2 Jun 2026 |

| 2 | Last day 2 Jul 2026; mails 27 Jun 2026 |

| 3 | Signs Form 15620; income $18,000 |

| 4 | Address: Ogden, UT 84201-0002 |

| 5 | USPS Certified Mail; saves PS Form 3800 |

| 6 | Uploads employer copy to Shareworks |

| 7 | Scorecard 44/60 — passes verification |

Verdict for Nina: Washington → Ogden under 2025 tables—do not copy a Texas founder’s Austin envelope.

Worked example: Omar, early exercise while on assignment in Germany

Facts (hypothetical): Omar, a U.S. citizen, early-exercises 20,000 unvested shares of Lattice AI, Inc. on 18 May 2026 while living in Berlin. He files Form 2555; preparer confirms international Form 1040 table.

| Item | Value |

|---|---|

| IRS campus | Austin, TX |

| ZIP | 73301-0215 USA (international—not 73301-0002) |

| Mail service | USPS international trackable or PDS per CPA |

| Proof target | Scorecard ≥ 40/60 including employer copy |

Where I'm less sure—state residency still on a California return while abroad can change campus choice; Omar should not guess between Ogden and 0215 Austin without preparer written instruction.

Steel-man: “I’ll email the election to HR and skip the IRS”

Best case for HR-only filing: Your company runs a white-glove 83(b) program, counsel prepares the envelope, and Stock Admin couriers the IRS original for you. Some venture-backed startups still do this well.

Why HR-only fails: Treas. Reg. §1.83-2 requires filing with the IRS, not the employer. An HR inbox upload without a timely IRS original does not make a valid election. Anecdotally, the failures we see in employee forums are employer portal “done” checkmarks with no Certified Mail receipt.

Our position: Treat HR upload as step 6, never a substitute for step 5. If your company offers mailing as a benefit, still demand a copy of the Certified Mail receipt in your personal folder.

Verdict

For irs 83(b) election 30 days execution: run the seven steps in order, use the state table for your residence, mail USPS Certified Mail to the correct campus, and close with the verification scorecard within 48 hours. File early in the window, escalate to counsel on day 28+ or when accelerated income exceeds cash on hand, and pair this guide with where to mail for expat ZIP edge cases and official filing language for Form 15620 detail.

Related guides

| Need | Article |

|---|---|

| Deadline math + tracker | 83(b) deadline & mailing tracker |

| Full address deep dive | Where to mail your 83(b) |

| Form 15620 official bundle | How to file an official Section 83(b) |

| Shorter checklist | How to file within 30 days |

| RSU ineligibility | Why RSUs usually cannot use 83(b) |

Primary sources

| Authority | Link |

|---|---|

| IRC §83(b) | 26 U.S.C. §83 |

| Treas. Reg. §1.83-2 | 26 CFR §1.83-2 |

| IRS Form 15620 (Apr 2025) | |

| IRS Where To File (domestic 1040) | IRS.gov |

| IRC §7502 / §7503 | §7502 · §7503 |

Footnotes

Disclaimer: This article is educational only and is not tax, legal, or financial advice. Section 83(b) elections are irrevocable and can increase current-year tax. Confirm transfer dates, FMV, mailing addresses, and payment obligations with a qualified CPA, enrolled agent, or tax attorney before filing.

Footnotes

-

IRS Form 15620 instructions (April 2025), “When to File.” ↩

-

IRC §7503 — if the 30th day falls on Saturday, Sunday, or legal holiday, timely filing may be the next succeeding day that is not Saturday, Sunday, or legal holiday (per Form 15620 cross-reference). ↩

-

Treas. Reg. §1.83-2 — filing with IRS, furnishing copies, attaching copy to income tax return for year of transfer. ↩ ↩2

-

Form 15620 instructions (April 2025), “Where to File.” ↩