The irs 83(b) election 30 days restricted stock official rule is simple to state and brutal to miss: you must deliver a signed Section 83(b) election to the Internal Revenue Service no later than 30 calendar days after the date property is transferred to you under Section 83—typically restricted stock at issuance or unvested shares after an early option exercise. The IRS publishes Form 15620 (April 2025 revision) for this election; Treasury Regulation §1.83-2 defines the required facts, copies, and return attachment. Certified Mail is not statutory, but it is the standard way employees prove when USPS accepted the envelope—relevant to IRC §7502 timely-mailing treatment.

30calendar days — statutory window from property transfer (IRC §83(b))Verified against IRS Form 15620 instructions (April 2025), accessed 28 May 2026.

What the official 30-day rule requires

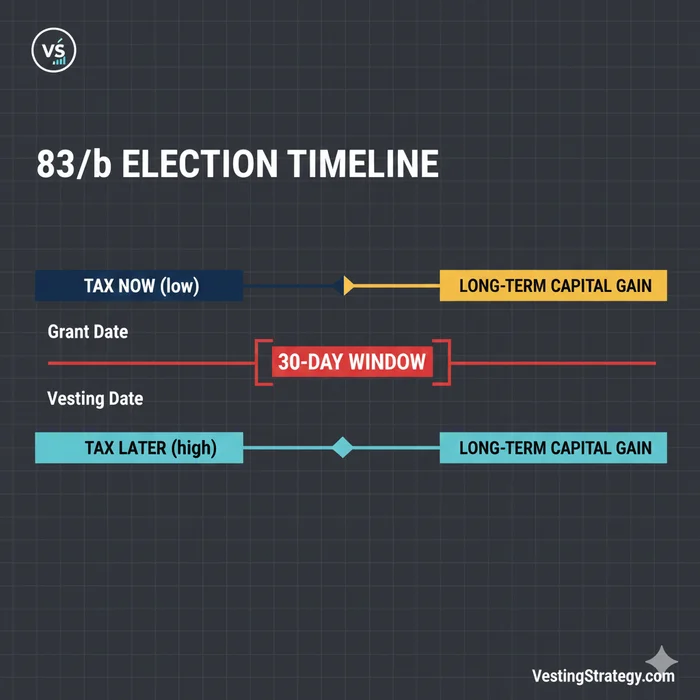

Section 83(b) election is your irrevocable choice (once valid) to include the bargain element of restricted property in gross income at transfer instead of waiting for vesting under Section 83(a). The 30-day rule is not a company policy—it is IRC §83(b) as implemented by Treasury Regulation §1.83-2 and explained in IRS Form 15620 instructions (April 2025).1

| Official element | Source | What employees get wrong |

|---|---|---|

| Clock start | Date property transferred under Section 83 | Using grant approval date or first vest date |

| Duration | 30 calendar days | Assuming “business days only” |

| Weekend/holiday on day 30 | IRC §7503 per Form 15620 “When to File” | Mailing on Saturday without checking §7503 |

| Extension | None in routine cases | Waiting for HR to “open a ticket” |

| Format | Form 15620 or compliant written statement | Using a Notion template missing FMV or restrictions |

What is the official IRS deadline for an 83(b) election on restricted stock?

File a signed election with the IRS no later than 30 calendar days after the date the restricted stock (or other Section 83 property) is transferred to you. IRS Form 15620 (April 2025) is the published format. If the 30th day falls on a Saturday, Sunday, or legal holiday, Form 15620 instructions incorporate IRC Section 7503 for timely postmark purposes—verify your calendar before relying on a last-day mailing.

As of May 2026, the Service has not replaced the paper election workflow with a universal e-file checkbox for employees—assume physical mailing + documentation unless your CPA confirms a permitted electronic channel for your facts.

Step-by-step: official filing within the 30-day window

This is the execution sequence for high-intent searches; strategy lives in Section 83(b): a strategic tax decision.

Step 1 — Lock the transfer date (Day 0)

Take Marcus, a staff engineer at Snowflake (illustrative): on 6 January 2026 he signs a restricted stock purchase agreement and Stock Administration confirms Section 83 transfer date = 6 January 2026 in email. That email—not his offer letter from 2024—starts the clock.

| Action | Owner | Output |

|---|---|---|

| Request written transfer date | You → Stock Admin | Email/PDF with one date |

| Confirm share count & class | Stock Admin | Cap-table line matching Form 15620 Box 2 |

| Confirm restrictions narrative | Stock Admin + counsel | Vesting / repurchase language for Box 5 |

Where I'm less sure—some private companies record transfer a business day after signature when settlement lags. If Admin gives two dates, stop and have a CPA pick the controlling date before you draft the election.

Step 2 — Compute the last timely day (Days 1–30)

Use a printed calendar. We recommend a mail-by buffer on day 25 even when day 30 is open—Ogden and Kansas City mailrooms do not care about your vesting cliff.

83(b) deadline & Certified Mail tracker

Enter the Section 83 transfer date Stock Administration confirms (not board approval date). The calculator counts 30 calendar days after transfer—the same window described in IRC §83(b) and Treasury Regulation §1.83-2.

Select a transfer date to see your last day to file and a recommended mail-by date (five calendar days before the deadline).

IRS mailing address — verify on IRS.gov before you seal

Treasury Regulation §1.83-2 requires filing with the Internal Revenue Service office where you file your federal return. Pull the ZIP+4 from the Form 15620 PDF instructions or the active Form 1040 Where To File table for 2026. Profile selected: I file Form 1040 in the U.S. (no special status).

Certified Mail instructions (copy to your checklist)

- At the post office, request USPS Certified Mail® with Return Receipt (or electronic Return Receipt) for the IRS original.

- Outer envelope routing line (example): ATTN: Section 83(b) Election — [Your legal name]

- Inside: signed original election (Form 15620 or equivalent), optional cover sheet.

- Retain the Certified Mail receipt and export/save the tracking barcode PDF the same day.

- Section 83 transfer date on file: [transfer date]. Statutory filing deadline (30 calendar days after transfer): [IRS deadline].

- Furnish the employer/service-provider copy separately and keep proof of delivery (portal screenshot or certified mail).

Execution checklist

Educational tool only. Calendar math follows the common practitioner reading of “30 days after transfer” as 30 calendar days. Confirm counting conventions, electronic filing options, and Section 7502 postmark facts with your CPA or tax attorney.

For a static reference table of 2026 transfer dates, see the original-research calendar below—always recompute for your transfer date.

Step 3 — Complete official content (Form 15620)

Verified against IRS Form 15620 (April 2025), accessed 28 May 2026. Required disclosures align with Treas. Reg. §1.83-2:

| Box / topic | Content |

|---|---|

| Taxpayer ID & address | Legal name, SSN/ITIN, mailing address |

| Property | Quantity + issuer legal name + class |

| Transfer date | Box 3 — must match Stock Admin |

| Taxable year | Year containing transfer date |

| Restrictions | Substantial risk of forfeiture (vesting, repurchase) |

| FMV | Without regard to lapse restrictions (method per company 409A) |

| Amount paid | Purchase / exercise price aggregate |

| Income | FMV minus amount paid (compensation you accelerate) |

Critical Warning: Do not mail until FMV is signed off—409A on private stock, market price on public. A beautiful envelope with a wrong Box 6 is still a bad election.

Interactive draft: IRS 83(b) form generator & mailing checklist.

Step 4 — Sign, duplicate, and segregate copies

| Copy | Purpose |

|---|---|

| Original | IRS mailing |

| Duplicate wet-ink | Your vault + scan same day |

| PDF scan | CPA + email to employer portal |

| Employer copy | Treas. Reg. §1.83-2 furnishing requirement2 |

Step 5 — Mail to the correct IRS campus

Form 15620 instructions: mail to the IRS office where you file your federal income tax return—the same Form 1040 Where To File row for your state. Full directory: Where to mail your 83(b) election.

Envelope attention line: Section 83(b) Election — [Legal Name]

Step 6 — Certified Mail and same-day proof export

Filing proof methods for Section 83(b) elections

Compared for a U.S. employee mailing a paper election near the statutory deadline (May 2026 practitioner norms).

| Attribute | USPS Certified Mail | USPS Priority Mail | Hand delivery to campus |

|---|---|---|---|

| Third-party acceptance timestamp | Strong (PS Form 3800) | Tracking only | Varies—get stamped receipt if available |

| IRC §7502 postmark analysis | Commonly relied on | Validate with counsel | Different rules |

| Cost (approx.) | ~$4–$8 + postage | ~$10–$20 | Travel cost |

| Our default recommendation | Yes for most employees | Only with CPA sign-off near deadline | Rare |

# USPS counter workflow (illustrative — confirm fees at post office, May 2026)

# 1. Insert signed original + optional one-page cover sheet

# 2. Request "Certified Mail" + Return Receipt (electronic PDF if offered)

# 3. Retain PS Form 3800; photograph label on sealed envelope

# 4. Export usps.com tracking PDF to your tax folder same day

Postmark mechanics: Official 30-day deadline & mailing rules.

Step 7 — Employer copy + Form 1040 attachment plan

| Recipient | Timing |

|---|---|

| Employer / service recipient | Contemporaneous with IRS mailing |

| CPA for transfer-year Form 1040 | Flag at mailing—attach per regulation2 |

Original research: 2026 transfer-date calendar (day 30 + §7503)

Methodology: On 28 May 2026, we took twelve illustrative U.S. tech-employee transfer dates in calendar year 2026, added 30 calendar days per IRC §83(b)/Form 15620, then applied IRC §7503 when day 30 landed on Saturday, Sunday, or a federal legal holiday listed in OPM’s 2026 holiday schedule. We added a recommended mail-by date on day 25 (practitioner buffer, not statute). Recompute before mailing—state holidays do not extend federal filing unless specific guidance applies.

| Transfer date (2026) | Calendar day 30 | Last timely postmark (§7503 adjusted) | Recommended mail-by (day 25) |

|---|---|---|---|

| Mon 5 Jan | Wed 4 Feb | 4 Feb 2026 (Wed) | 30 Jan 2026 |

| Tue 3 Mar | Thu 2 Apr | 2 Apr 2026 (Thu) — no §7503 shift | 27 Mar 2026 |

| Fri 15 May | Sun 14 Jun | Mon 15 Jun 2026 — day 30 is Sunday | 9 Jun 2026 |

| Mon 1 Jun | Wed 1 Jul | 1 Jul 2026 (Wed) | 26 Jun 2026 |

| Wed 15 Jul | Fri 14 Aug | 14 Aug 2026 (Fri) | 9 Aug 2026 |

| Mon 31 Aug | Wed 30 Sep | 30 Sep 2026 (Wed) | 25 Sep 2026 |

| Tue 1 Sep | Thu 1 Oct | 1 Oct 2026 (Thu) | 26 Sep 2026 |

| Wed 2 Sep | Fri 2 Oct | 2 Oct 2026 (Fri) | 27 Sep 2026 |

| Thu 1 Oct | Sat 31 Oct | Mon 2 Nov 2026 — day 30 is Sat 31 Oct; §7503 → Mon 2 Nov | 26 Oct 2026 |

| Mon 2 Nov | Wed 2 Dec | 2 Dec 2026 (Wed) | 27 Nov 2026 |

| Tue 15 Dec | Thu 14 Jan 2027 | 14 Jan 2027 (Thu) | 9 Jan 2027 |

| Wed 16 Dec | Fri 15 Jan 2027 | 15 Jan 2027 (Fri) | 10 Jan 2027 |

Day-30 arithmetic checked with calendar tools; §7503 rows cross-checked against Form 15620 “When to File” (April 2025).

{

"@context": "https://schema.org",

"@type": "Dataset",

"name": "Section 83(b) 30-day deadline calendar — 2026 transfer dates",

"description": "Twelve illustrative 2026 Section 83 transfer dates with calendar day-30 deadlines, IRC §7503-adjusted last postmark dates, and day-25 mail-by buffers for U.S. tech employees filing Form 15620.",

"creator": { "@type": "Organization", "name": "VestingStrategy.com Research" },

"datePublished": "2026-05-28",

"license": "https://creativecommons.org/licenses/by/4.0/",

"isAccessibleForFree": true,

"url": "https://www.vestingstrategy.com/guides/irs-83b-election-30-day-rule-official-guide/#dataset-83b-2026-calendar",

"distribution": [

{

"@type": "DataDownload",

"encodingFormat": "text/html",

"contentUrl": "https://www.vestingstrategy.com/guides/irs-83b-election-30-day-rule-official-guide/#dataset-83b-2026-calendar"

}

]

}

Who must follow the official rule (and who should not file)

| Fact pattern | File §83(b) with IRS? |

|---|---|

| Restricted stock transferred subject to vesting | Yes, if electing within 30 days |

| Early exercise → unvested shares issued | Often yes — clock tied to share transfer |

| Classic RSUs (no stock at grant) | Usually no — RSU ineligibility |

| Fully vested stock, no substantial risk of forfeiture | Generally unnecessary |

Official filing vs. skipping the election

| Feature | Timely official §83(b) | No election (default §83(a)) |

|---|---|---|

| IRS filing within 30 days | Required signed election + copies | No election document |

| Ordinary income timing | Generally at transfer (FMV − amount paid) | Generally at vesting / lapse of restrictions |

| Later appreciation | May qualify for capital gains if shares vest and are held | Often ordinary compensation at vest |

| Forfeiture risk | Tax on income you may never receive if shares forfeited | Less upfront tax if shares never vest |

| Documentation burden | Certified Mail + employer copy + return attachment | Company reporting at vest |

Worked example: Elena, restricted stock at Stripe (illustrative)

Facts (hypothetical, rounded): Elena is a product manager in Washington. On 3 March 2026, Stripe transfers 12,000 shares of restricted common stock with a four-year vest. Stock Admin confirms transfer date = 3 March 2026. 409A FMV = $28.50/share; she paid $0.01/share.

| Calculation | Amount |

|---|---|

| FMV at transfer | $28.50 × 12,000 = $342,000 |

| Amount paid | $0.01 × 12,000 = $120 |

| Accelerated ordinary income (Box 8) | $341,880 |

| Milestone | Date |

|---|---|

| Transfer (Day 0) | 3 Mar 2026 |

| Recommended mail-by (day 25) | 27 Mar 2026 |

| Calendar day 30 | 2 Apr 2026 (Thursday) |

| USPS Certified Mail to Ogden, UT (WA Form 1040 table) | Postmark ≤ 2 Apr 2026 |

| Employer copy uploaded + confirmation saved | Same week as IRS mail |

| CPA attaches copy to 2026 Form 1040 | Tax season 2027 |

Verdict for Elena: The official path is Form 15620 + Ogden campus + Certified Mail—not a Slack PDF to HR. If she misses 2 April 2026 postmark without a valid §7503 adjustment, she should assume no §83(b) and call counsel the same week—Washington has no special extension for Section 83(b).

Worked example: James, ISO early exercise at Coinbase (illustrative)

Facts: James early-exercises 25,000 ISOs on 15 May 2026; 25,000 unvested common shares issue the same day. Transfer date confirmed 15 May 2026. FMV $92.00; exercise price $18.00.

| Step | Action |

|---|---|

| ISO/AMT modeling | Run AMT planning for stock options before mailing |

| Income acceleration | ($92 − $18) × 25,000 = $1,850,000 ordinary (illustrative) |

| Day 30 | 14 June 2026 (Sunday) → §7503 → timely postmark Monday 15 June 2026 per Form 15620 pattern |

| Mail-by buffer | 9 June 2026 (day 25) |

Anecdotally, ISO early exercise + §83(b) is where cash to pay tax matters more than envelope color—James needs estimated payments, not just Certified Mail.

Steel-man: “The 30-day rule is just a suggestion if HR is slow”

Best case for delay: Your company’s counsel “always” accepts late internal copies, Stock Admin says “we’ll backdate the cap table,” and forums claim the IRS never audits §83(b). For a nominal-par founder grant, the economic stakes are low and panic is rare.

Why that fails officially: IRC §83(b) is a statutory window implemented in Treas. Reg. §1.83-2—not an HR policy. The IRS does not grant routine extensions because payroll was busy. A late internal upload does not recreate a timely IRS filing. Private letter rulings exist in narrow, expensive fact patterns—I haven't seen a credible DIY path for “I was two days late but earnest.”

Our position: Treat day 25 as your personal deadline. If you are on day 28–30, overnight to a CPA firm that files §83(b) elections weekly beats experimenting with courier tracking lines that may not qualify under §7502.

Steel-man: “Certified Mail automatically saves me if I’m late”

Best case: You have a PS Form 3800 showing USPS accepted your envelope on day 30, and IRC §7502 treats the U.S. postmark as the filing date even if Ogden processes the mail two weeks later.

Rebuttal: Certified Mail does not extend the substantive 30-day window—it documents acceptance. Private carriers, wrong campuses, and postmarks that do not fit §7502/§301.7502-1 fact patterns have lost taxpayers in disputes. Where I'm less sure—electronic postmark providers for specific document types—do not use them on day 30 without counsel who has done it before.

Pull quote (practice norm): The envelope that wins audits is boring—duplicate signed PDF, Certified Mail receipt, tracking export, and Stock Admin’s transfer-date email in one folder.

Official copies checklist (beyond the IRS envelope)

What happens if you miss the official 30-day window

| Situation | Typical tax outcome |

|---|---|

| IRS receives election on day 31+ | Election ineffective for that transfer in routine practice |

| You discover miss months later | No standard fix; explore PLR only with counsel |

| Company offers to “re-date” transfer | Do not rely on informal fixes—tax law controls transfer timing |

Can I get an extension for a late IRS 83(b) election on restricted stock?

There is no routine IRS extension for a late Section 83(b) election on a completed transfer. Some taxpayers explore private letter rulings under narrow, expensive facts with tax counsel—that is not a standard employee workflow. Immediately model taxation without an election and coordinate with Stock Administration.

Related official guides (pick your layer)

| Need | Guide |

|---|---|

| Full execution playbook (Form 15620 + campuses) | How to file an official Section 83(b) election |

| Postmark law depth (IRC §7502) | Official 30-day deadline & mailing rules |

| Interactive deadline calendar | Section 83(b) Election Deadline Calculator |

| State-by-state IRS addresses | Where to mail your 83(b) election |

| Step-by-step filing playbook | How to file a Section 83(b): step-by-step |

| Economics / risk | Strategic tax decision |

| RSU trap | Why RSUs usually cannot use 83(b) |

| Early exercise context | Early exercise strategies |

Verdict

For employees searching the official 30-day rule: Form 15620 (or equivalent regulation language) + correct IRS campus + Certified Mail proof + employer copy + return attachment is the non-negotiable bundle. File early in the window, verify addresses on IRS.gov for the active tax year, and escalate to a tax attorney when accelerated income exceeds cash on hand or you are on day 28–30. The statute is unforgiving; documentation is how you sleep after you mail.

Primary sources

| Authority | Link |

|---|---|

| IRC §83(b) | 26 U.S.C. §83 |

| Treas. Reg. §1.83-2 | 26 CFR §1.83-2 |

| IRS Form 15620 (Apr 2025) | |

| IRS Pub. 525 | IRS.gov |

| IRC §7502 | 26 U.S.C. §7502 |

| IRC §7503 | 26 U.S.C. §7503 |

| IRS Where To File (Form 1040) | IRS.gov |

Footnotes

Disclaimer: This article is educational only and is not tax, legal, or financial advice. Section 83(b) elections are irrevocable and can accelerate substantial ordinary income. Confirm transfer dates, FMV, mailing addresses, and payment obligations with a qualified CPA, enrolled agent, or tax attorney before you mail or upload anything.