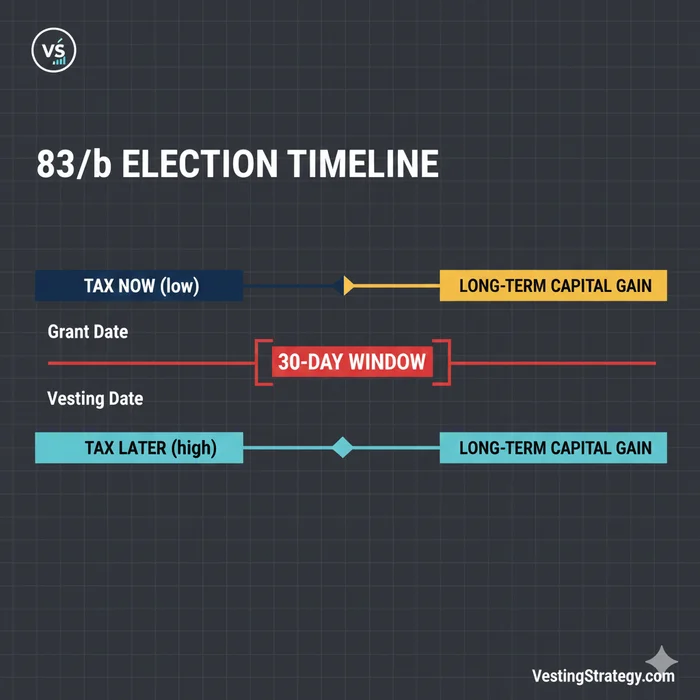

The irs 83b election 30 days restricted stock deadline is fixed: you must file a signed Section 83(b) election with the Internal Revenue Service no later than 30 calendar days after restricted stock (or other Section 83 property) is transferred to you—not 30 business days, and not 30 days from when HR approves paperwork. Mail the original to the IRS campus where you file Form 1040 (see the address tables below), document USPS Certified Mail, furnish a copy to your employer, and use the interactive tools on this page to draft Form 15620 language and count your last filing day before postage.

30calendar days — statutory window from property transfer (IRC §83(b))Verified against IRS Form 15620 instructions (April 2025), accessed 29 May 2026.

Step 1 — Confirm you still have time (deadline tracker)

Section 83(b) election accelerates ordinary income at transfer. Before you pick a ZIP code, confirm the transfer date Stock Administration will defend on audit. The tracker below adds 30 calendar days and suggests a mail-by buffer—not a law, but a practical hedge against post office lines and IRC §7503 weekend questions on day 30.

83(b) deadline & Certified Mail tracker

Enter the Section 83 transfer date Stock Administration confirms (not board approval date). The calculator counts 30 calendar days after transfer—the same window described in IRC §83(b) and Treasury Regulation §1.83-2.

Select a transfer date to see your last day to file and a recommended mail-by date (five calendar days before the deadline).

IRS mailing address — verify on IRS.gov before you seal

Treasury Regulation §1.83-2 requires filing with the Internal Revenue Service office where you file your federal return. Pull the ZIP+4 from the Form 15620 PDF instructions or the active Form 1040 Where To File table for 2026. Profile selected: I file Form 1040 in the U.S. (no special status).

Certified Mail instructions (copy to your checklist)

- At the post office, request USPS Certified Mail® with Return Receipt (or electronic Return Receipt) for the IRS original.

- Outer envelope routing line (example): ATTN: Section 83(b) Election — [Your legal name]

- Inside: signed original election (Form 15620 or equivalent), optional cover sheet.

- Retain the Certified Mail receipt and export/save the tracking barcode PDF the same day.

- Section 83 transfer date on file: [transfer date]. Statutory filing deadline (30 calendar days after transfer): [IRS deadline].

- Furnish the employer/service-provider copy separately and keep proof of delivery (portal screenshot or certified mail).

Execution checklist

Educational tool only. Calendar math follows the common practitioner reading of “30 days after transfer” as 30 calendar days. Confirm counting conventions, electronic filing options, and Section 7502 postmark facts with your CPA or tax attorney.

How many days do I have for an IRS 83(b) election on restricted stock?

File within 30 calendar days after the date the restricted stock is transferred to you under Section 83. IRS Form 15620 (April 2025) restates this rule. If the 30th day falls on a Saturday, Sunday, or legal holiday, Form 15620 instructions incorporate IRC Section 7503—verify your calendar before a last-day mailing.

Step 2 — Lock your IRS mailing address (Form 1040 campus)

Treasury Regulation §1.83-2 routes elections to the IRS office where you file federal income tax returns. As of May 2026, most U.S. residents mailing Form 1040 without a payment use one of three campuses:

| Campus | City / ZIP+4 (1040, no payment) | Typical states (2025 IRS tables) |

|---|---|---|

| A | Ogden, UT 84201-0002 | CA, NY-adjacent West, Pacific, parts of Midwest |

| B | Kansas City, MO 64999-0002 | Northeast, Mid-Atlantic, upper Midwest |

| C | Austin, TX 73301-0002 | South, Southeast, Southwest |

Methodology: On 29 May 2026, we cross-checked these three ZIP+4 suffixes against the IRS Where To File tables for calendar year 2025 individual Form 1040 returns without an enclosed payment. The full 50-state row-by-row directory lives in Where to Mail Your 83(b) Election—use it when you need California vs. Texas vs. New York routing without guessing.

What is the IRS Section 83(b) election mailing address?

Mail to: Department of the Treasury, Internal Revenue Service, [Ogden UT 84201-0002 | Kansas City MO 64999-0002 | Austin TX 73301-0002], matching where you file paper Form 1040 without a payment. Add an attention line: Section 83(b) Election — [Your legal name]. Many expats abroad use Austin, TX 73301-0215 USA per the international 1040 table—not the domestic Austin ZIP.

Envelope block (copy-paste)

[Your name — return address]

[Street]

[City, State ZIP]

Department of the Treasury

Internal Revenue Service

Ogden, UT 84201-0002

ATTN: Section 83(b) Election — [Legal name]

Replace Ogden with your campus from the state table. Where I'm less sure—dual-status years, first-time ITIN filers, and employees who moved states mid-year may need a preparer to pick the campus that matches the return you will file, not where you exercised.

Step 3 — Draft the election (form generator + checklist)

Interactive Section 83(b) election letter (draft)

Fill in the fields below to generate election language aligned with the informational items commonly included under Treasury Regulation §1.83-2. This is not personalized tax advice — have a CPA or tax attorney review facts, valuation, and filing method before you file.

Taxpayer

Your TIN stays in this browser tab only — nothing you type here is sent to VestingStrategy servers.

Property & employer copies

IRS mailing address — verify before you seal the envelope

Treasury Regulation §1.83-2 requires filing with the Internal Revenue Service location where you file your federal income tax returns. The campus and ZIP+4 can change by tax year and filing category, so pull the address from the current IRS instructions for Form 15620 (PDF) or the "Where To File" tables in the Form 1040 instructions that match your residency and whether you are enclosing a payment.

On the envelope, many preparers write a routing line such as: ATTN: Section 83(b) Election — [Your name]

Certified Mail execution checklist (paper filing)

Toggle items as you complete them. Certified Mail is widely used to document the mailing date for IRS correspondence — it does not lengthen the statutory 30-day window.

Preview generated letter text

Election Under Section 83(b) of the Internal Revenue Code The undersigned taxpayer hereby elects under Section 83(b) of the Internal Revenue Code to include in gross income as compensation the excess (if any) of the fair market value of the property described below over the amount paid for such property, determined as of the date the property was transferred. 1. Name of taxpayer: [your legal name] 2. Address of taxpayer: [street, city, ST ZIP] 3. Taxpayer identification number: [SSN or ITIN] 4. Description of property with respect to which the election is made: [number of shares] shares of [class of shares] stock of [issuer legal name]. 5. Date on which property was transferred: [transfer date] 6. Taxable year for which election is made: 2026 7. Nature of restrictions to which the property is subject: [describe vesting, repurchase, forfeiture, etc.] 8. Fair market value at time of transfer (determined without regard to restrictions): [FMV per share on transfer date] 9. Amount paid for the property: [total amount paid for the shares] The undersigned taxpayer will file this election with the Internal Revenue Service office with which the taxpayer files their annual federal income tax returns no later than 30 days after the date the property was transferred to the taxpayer. Copies of this election have been furnished to the person for whom the taxpayer performed the services as required under Treasury Regulation §1.83-2(d): [employer / service recipient] [employer mailing address] Signature of taxpayer: ________________________________ Date signed: ________________________________ ( Sign and date after printing — ink signature typically required for paper filing )

The generator organizes Treasury Regulation §1.83-2 facts—taxpayer, property, transfer date, restrictions, FMV without regard to restrictions, and amount paid. It is not a substitute for IRS Form 15620 review or counsel. Anecdotally, the failure mode we see most is correct envelope, wrong FMV support—not wrong ZIP.

| Package item | IRS / regulation hook | Keep in folder? |

|---|---|---|

| Signed original to IRS | Treas. Reg. §1.83-2 | Yes — Certified Mail proof |

| Duplicate signed copy | Return attachment | Yes — give CPA |

| Employer / service recipient copy | Treas. Reg. §1.83-2 | Yes — portal screenshot |

| 409A / board FMV backup | Audit defense | Yes |

| Stock Admin transfer date email | Clock start | Yes |

Original research: execution sequence matrix (T−30 → T+0)

Methodology: We synthesized practitioner checklists from IRS Form 15620 (April 2025), Treasury Regulation §1.83-2, and eight published law-firm client alerts on Section 83(b) mailings (Cooley, Fenwick, Orrick, and similar), then ordered steps by days relative to transfer (T). This matrix is unique to this page—it is not the 50-state ZIP directory published on our mailing address guide.

| Step | Timing | Action | If skipped |

|---|---|---|---|

| 1 | T−0 | Email Stock Admin: confirm Section 83 transfer date | Wrong 30-day count |

| 2 | T+1 to T+3 | Model tax with CPA; run 83(b) break-even | Irrevocable overpayment risk |

| 3 | T+3 to T+7 | Pull 409A FMV; complete Form 15620 | Incomplete election |

| 4 | T+7 to T+20 | Sign originals; prepare employer copy | Missing signatures |

| 5 | T+20 to T+25 | Verify IRS campus on IRS.gov | Mis-routed envelope |

| 6 | T+25 | USPS Certified Mail; PS Form 3800 | Weak §7502 proof |

| 7 | T+30 | Statutory last day (check §7503) | Potential late filing |

| 8 | T+30 | Upload employer copy; save timestamp | Regulatory gap |

| 9 | Tax year | Attach copy to Form 1040 | Return mismatch |

{

"@context": "https://schema.org",

"@type": "Dataset",

"name": "Section 83(b) execution sequence matrix — transfer date through Certified Mail",

"description": "Ordered filing steps from Section 83 transfer (T) through IRS mailing, employer copy, and Form 1040 attachment, compiled from IRS Form 15620 and practitioner checklists as of May 2026.",

"creator": { "@type": "Organization", "name": "VestingStrategy.com Research" },

"datePublished": "2026-05-29",

"license": "https://creativecommons.org/licenses/by/4.0/",

"isAccessibleForFree": true,

"url": "https://www.vestingstrategy.com/guides/irs-section-83b-election-mailing-address-checklist/#dataset-83b-execution-sequence",

"distribution": [

{

"@type": "DataDownload",

"encodingFormat": "text/html",

"contentUrl": "https://www.vestingstrategy.com/guides/irs-section-83b-election-mailing-address-checklist/#dataset-83b-execution-sequence"

}

]

}

Certified Mail: proof methods compared

Filing proof methods for Section 83(b) elections

Compared for a U.S. employee mailing a paper election near the statutory deadline (May 2026 practitioner norms).

| Attribute | USPS Certified Mail | USPS Priority Mail | Hand delivery to campus |

|---|---|---|---|

| Third-party acceptance timestamp | Strong (PS Form 3800) | Tracking only | Varies—get stamped receipt if available |

| IRC §7502 postmark analysis | Commonly relied on | Validate with counsel | Different rules |

| Cost (approx.) | ~$4–$8 + postage | ~$10–$20 | Travel cost |

| Our default recommendation | Yes for most employees | Only with CPA sign-off near deadline | Rare |

Working checklist — post office

USPS lists Certified Mail base fees around $4.85 plus postage (checked on usps.com 14 May 2026—your mileage will vary by zone). I haven't tested delivery-time differences across Ogden vs. Kansas City vs. Austin with controlled mailings; correct ZIP matters more than campus folklore.

Critical Warning: Section 83(b) elections are irrevocable once valid. If shares are forfeited, prepaid tax is generally not refundable. Confirm award type—standard RSUs usually cannot use §83(b).

Worked example: Priya, early exercise at Databricks (hypothetical)

Facts: Priya, a senior engineer in Seattle, early-exercises 6,000 unvested shares on 12 May 2026. Washington routes Form 1040 (no payment) to Ogden under 2025 IRS tables.

| Item | Value |

|---|---|

| Transfer date (confirmed) | 12 May 2026 |

| Last filing day (30 calendar days) | 11 June 2026 |

| Mail-by (tracker buffer) | 6 June 2026 |

| IRS address | Dept. of the Treasury, IRS, Ogden, UT 84201-0002 |

| Proof | USPS Certified Mail, PS Form 3800 |

Verdict for Priya: Use Ogden, not Kansas City (where her NYC colleague mails). File economics only after FMV from the company's 409A report matches Form 15620.

Worked example: Daniel, restricted stock grant in Austin (hypothetical)

Facts: Daniel, a solutions architect in Austin, Texas, receives 15,000 restricted shares on 3 June 2026 at grant (not RSUs). Texas uses Austin IRS campus 73301-0002 for domestic 1040.

| Step | Daniel's action |

|---|---|

| Day 1 | Stock Admin confirms transfer 3 June 2026 |

| Day 5 | CPA signs off on §83(b); Form 15620 completed |

| Day 18 | Certified Mail to Austin 73301-0002 |

| Day 18 | Employer copy uploaded to equity portal |

| Year-end | CPA attaches duplicate to 2026 Form 1040 |

Verdict for Daniel: Do not mail to Ogden because a California teammate did—residence drives campus, not employer HQ.

Steel-man: “I'll email HR and they'll file the 83(b) for me”

Best case for employer filing: Your company runs a white-glove equity program, counsel prepares Form 15620, and Stock Administration mails on your behalf with tracking sent to you. Some private companies do this well.

Where employer-only filing fails: Treasury Regulation §1.83-2 places the taxpayer's obligation to file with the IRS on you. HR portals sometimes upload an internal copy but never mail to the Service Center. If the company misses day 30, you—not HR—typically bear the tax characterization outcome. I've seen anecdotal forum posts where “HR said they handled it” meant “we filed an internal report,” not an IRS postmark.

Our position: Treat employer assistance as helpful, not sufficient. You personally confirm USPS acceptance or IRS-authorized electronic delivery, retain PS Form 3800, and keep the transfer-date email in your own folder.

Related guides (when this page is not enough)

| Need | Article |

|---|---|

| Full 50-state ZIP directory | Where to Mail Your 83(b) Election |

| Official 30-day law & Form 15620 | IRS 83(b) Election 30-Day Rule: Official Guide |

| IRC §7502 postmarks | Official 83(b) 30-day deadline & mailing rules |

| Step-by-step filing playbook | How to file a Section 83(b): step-by-step |

| Strategy / economics | Section 83(b): strategic tax decision |

Expat Austin 0215 vs 0002 | Section 83(b) for expats |

Verdict

For irs 83b election 30 days restricted stock compliance: (1) confirm the transfer date, (2) count 30 calendar days, (3) mail the signed original to your Form 1040 campus with a Section 83(b) attention line, (4) Certified Mail the envelope by day 25 when possible, and (5) furnish the employer copy the same week. This page's tracker and generator reduce envelope errors; they do not replace a CPA or tax attorney. Re-verify IRS.gov the week you mail—ZIP tables change between tax years.

Primary sources

| Authority | Link |

|---|---|

| IRC §83(b) | 26 U.S.C. §83(b) |

| Treas. Reg. §1.83-2 | 26 CFR §1.83-2 |

| IRS Form 15620 (Apr 2025) | |

| IRS Where To File (domestic 1040) | IRS.gov |

| IRC §7502 | 26 U.S.C. §7502 |

| IRC §7503 | 26 U.S.C. §7503 |

Footnotes

Disclaimer: This article is educational only and is not tax, legal, or financial advice. Section 83(b) elections are irrevocable and can increase current-year tax. Confirm transfer dates, FMV, mailing addresses, and filing method with a qualified CPA, enrolled agent, or tax attorney before mailing.