Executive Summary

What is the IRC Section 4999 excise tax?

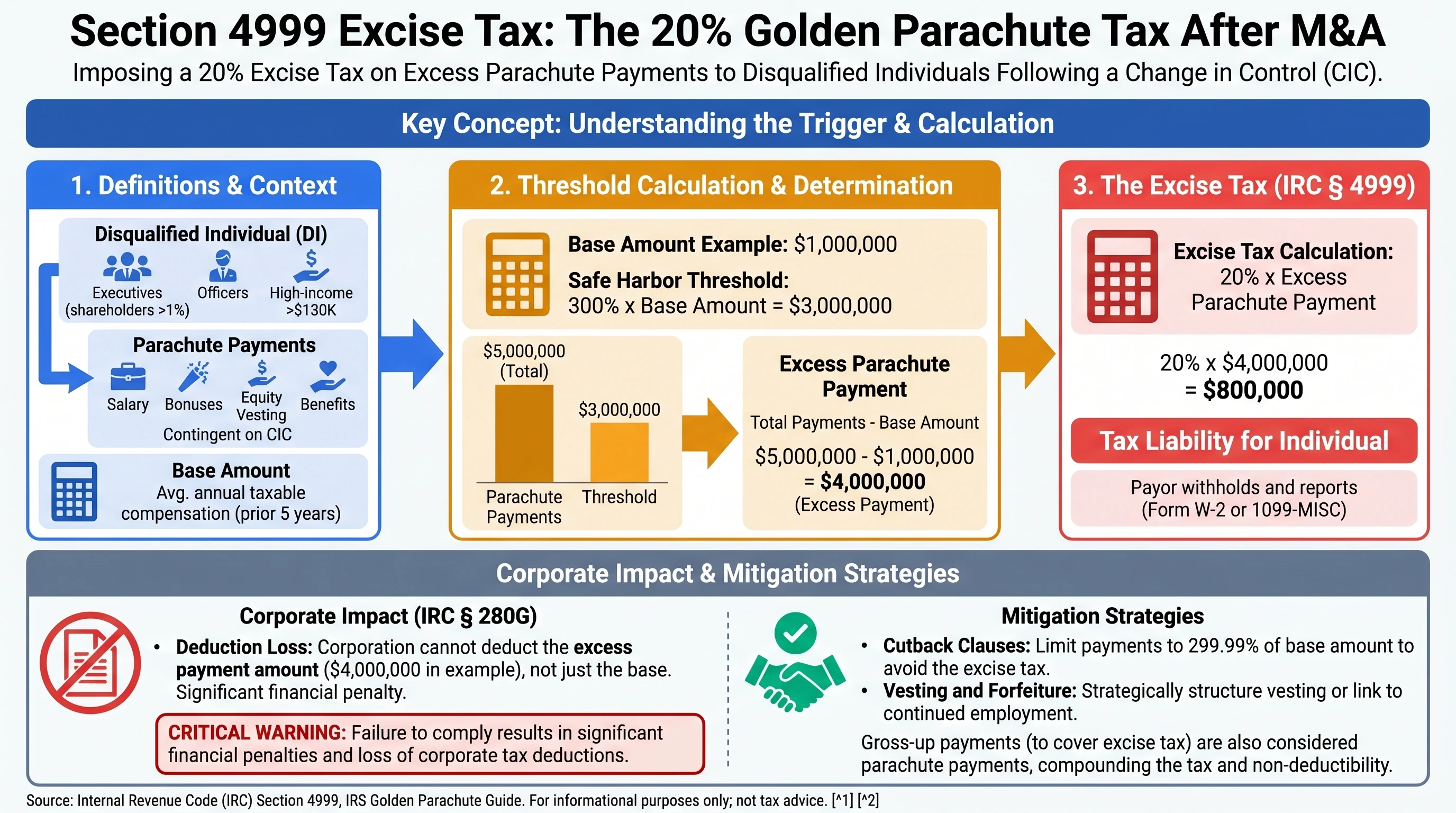

Section 4999 generally imposes a 20% excise tax on the recipient on excess parachute payments (as defined in Section 280G) when the statutory tests are met—which often happens around corporate changes in ownership or control. The tax is layered on ordinary income taxation; it does not replace it.

In mergers, acquisitions, and similar corporate transactions, IRC §4999 is the provision that commonly imposes a 20% federal excise tax on excess parachute payments (as defined under IRC §280G). Practitioners frequently discuss “280G/4999” together: §280G often raises corporate deduction issues; §4999 focuses on the individual excise.

This guide is education-only: golden parachute analysis is fact-intensive (definitions, exclusions, stacking of equity acceleration, payroll reporting, withholding, and gross-ups).

Related on this site: Golden Parachute & IRC §280G, Section 280G for executives, Stock options in M&A.

The bottom line: If the statutory tests are met after applying full definitions—not shortcut “headline math”—§4999 can materially reduce executive after-tax outcomes, especially when gross-ups enlarge the parachute payment stack.1

Critical Warning: Excess parachute payment is generally not “total parachute payments minus base amount.” Before relying on any arithmetic, confirm the legal definitions and exclusions with counsel.2

Understanding IRC Section 4999

Key definitions and the “3× base amount” corridor

Disqualified individuals, parachute payments, base amount, and excess parachute payment are statutory terms under IRC §280G. Section 4999 generally imposes the excise on excess parachute payments once those definitions are satisfied.

Threshold sketch (education only):

- Start from parachute payments determined under §280G.

- Compare against 3 × base amount (commonly described as the “3× corridor”).

- Excess parachute payment is generally parachute payments minus that 3× amount (not “parachute payments minus base amount”), subject to detailed rules and exclusions.

Illustrative arithmetic (not legal advice):

| Base amount | 3× corridor | Parachute payments (as defined) | Excess parachute payment (illustrative) | §4999 excise (20% of excess) |

|---|---|---|---|---|

| $1,000,000 | $3,000,000 | $5,000,000 | $5,000,000 − $3,000,000 = $2,000,000 | $400,000 |

| $500,000 | $1,500,000 | $1,600,000 | $1,600,000 − $1,500,000 = $100,000 | $20,000 |

Corporate impact, gross-ups, and iterative modeling

The 20% rate applies to the excess parachute payment (when defined). Separately, §280G can deny a corporate deduction for excess parachute payments. Because gross-up payments are often themselves treated as parachute payments in later passes, diligence teams sometimes model multiple iterations (gross-up on gross-up) rather than a single line-item guess.

Example (illustrative only): if an executive has $2,000,000 of excess parachute payments, a 20% excise might be about $400,000 before considering how any additional gross-up payments change the parachute stack.

Important note: Withholding, reporting, and whether a payor must gross up are contractual and payroll-specific—verify with counsel and your payroll provider.

Mitigation strategies (high level)

Transaction planning often includes cutbacks (reducing payments below defined thresholds), better-off cutbacks (choose the best after-tax outcome), shareholder cleansing procedures where available for private companies, and re-timing or re-characterization of payments—each path requires professional modeling.

| Strategy | Idea | What to validate |

|---|---|---|

| Cutback / cap | Reduce total parachute payments below the excise trigger after definitions | Documented legal analysis, not spreadsheet shortcuts |

| Better-off cutback | Compare after-tax outcomes with vs. without excise | Often includes state tax and payroll layers |

| Gross-up | Contractually reimburse excise | Can increase parachute payments—iterate the model |

How golden parachute rules show up for tech equity

In technology M&A, single-trigger or double-trigger vesting, transaction bonuses, cash severance, and equity acceleration can stack into the same analysis. If you are new to the equity mechanics, start with vesting schedules & acceleration and what happens in M&A, then return to the §280G/§4999 definitions with your transaction team.

Cross-border note: If you are not a U.S. taxpayer—or have foreign payers—U.S. golden parachute rules may still matter for U.S.-sourced pay and U.S. reporting, but the analysis is not the same as a purely domestic W-2 employee. Treat any blog claim that “foreign executives are exempt” as suspect until verified.

Frequently asked questions (Section 4999)

Is Section 4999 the same as Section 280G?

Answer: No. §280G is generally where deduction and definitions live for golden parachutes. §4999 generally imposes the 20% excise on excess parachute payments. You usually analyze both in the same workbook.

Who actually pays the 20% excise?

Answer: Typically the individual on excess parachute payments, but payment mechanics, withholding, and gross-up obligations are contractual and payroll-specific—confirm with advisors.

Does every large severance trigger Section 4999?

Answer: Not automatically. Payments must satisfy specific definitions, including contingency on a qualifying change in control, and statutory exceptions may apply depending on facts.

Can gross-ups eliminate the economics of Section 4999?

Answer: Gross-ups change cash flow, but they can increase the parachute payment stack depending on characterization and iteration. Modeling without iterating gross-ups frequently understates total exposure.

Where should I read the raw law?

Answer: Start with the statutes: 26 U.S.C. §4999 and 26 U.S.C. §280G.

Three modeling mistakes teams make (education only)

Deal models are only as good as definitions.

| Mistake | Why it hurts | Practical fix |

|---|---|---|

| Using total cash severance as “parachute payments” without testing contingency and exclusions | Severance unrelated to change can fall outside parachute definitions | Tie each pay element to statutory definitions and exclusions |

| Forgetting equity spread mechanics at acceleration | Acceleration can accelerate ordinary income timing (AMT/for ISO overlaps are separate puzzles) | Build equity grids with vesting timelines and forfeiture carve-outs |

| Treating gross-ups as “free cash” instead of potentially additive parachute payments | Gross-ups can move threshold math in iterative models | Model two or three iterations explicitly |

These points are deliberately non-prescriptive. Your counsel will map payments → definitions → withholding.

Worked vignettes (illustrative arithmetic only)

Vignette A — Narrow miss of the corridor

Assume a base amount of $600,000 (illustrative) and total parachute payments of $1,790,000 after definitions.

- 3× corridor = $1,800,000

- Because $1.79M < $1.8M, no excess parachute payment under the simplistic threshold story many teams narrate—but facts can still disqualify reliance on simplistic screens.

- Lesson: spreadsheets need footnote discipline tying each dollar to statutory buckets.

Vignette B — Crossing the corridor

Same base amount ($600,000). Parachute payments: $2,500,000.

- 3× corridor = $1,800,000

- Excess parachute payment (illustrative) = $2,500,000 − $1,800,000 = $700,000

- §4999 excise (illustrative) = 20% × $700,000 = $140,000

- Separate question: ordinary income taxation on inclusion items still rides alongside the excise.

Vignette C — Deferred pieces

If portions are paid later, present value/discount elections and payroll timing rules can reorganize perceived stacking. This is precisely why diligence copies award agreements, plans, offer letters, and change-in-control appendices.

How Section 4999 interacts (conceptually) with other federal layers

Federal tax debates around equity often mention ordinary rates, NIIT, and AMT. Section 4999 is different: think of it as a labeled excise on a defined excess amount, not “just another payroll withholding line.” Employees still face their normal inclusion mechanics for wages and equity—that is not replaced by §4999.

If you came from ISO disqualifying disposition threads or AMT planning, remember those topics do not substitute for a 280G modeling workbook prepared for your transaction facts.

Private-company “cleansing” vote (conceptual checklist)

Private corporations sometimes pursue shareholder approvals referenced in statutory safe harbors—but eligibility, disclosure, vote mechanics, and who counts as a disinterested shareholder vary. Public companies face different realities. Anything that sounds like “automatic cleansing” should trigger follow-up questions, not reassurance.

High-level diligence checklist:

- Identify every payment that references termination, sale, merger, or change in control

- Map timing—single bonus vs installments vs earnouts

- Reconcile payroll Forms W-2, Forms 1099, and equity broker statements buyers expect

- Compare seller vs buyer withholding responsibilities if your deal allocates obligations

Again: templates are not substitutes for advisors.

What to pull into diligence (checklist for employees, not legal advice)

Even if you never touch a tax model yourself, you can still force completeness by asking for the right artifacts.

| Document / data | Why buyers care |

|---|---|

| Equity ledger showing acceleration, cash-out, assumption, replacement awards | Determines how much economics move at close vs afterward |

| Severance / change-in-control exhibit referencing thresholds, better-off, caps | Contracts—not slide decks—drive whether pay is contingent |

| 402(b) / 280G materials if provided (names vary) | Shows whether teams already modeled disqualified individuals |

| Payroll memos describing withholding treatment for transaction bonuses | Cash in your bank account can differ from headline severance |

If you are comparing roles, also read how to read your equity grant so you can spot single-trigger vs double-trigger language before you rely on back-of-the-envelope equity value.

State income tax can layer on top (conceptual)

Federal golden parachute modeling is not the end of the story. State tax results can diverge when you move during a deal period or when sourcing disputes arise. This site covers patterns, not individualized outcomes—pair federal discussion with localized reading when needed (for example California equity sourcing topics if your facts resemble multi-state careers).

Example line-item map (fiction, illustrates categories only)

Imagine a hypothetical technology executive—not tax advice—with the following purely fictional payments tied to closing:

| Bucket | Stylized inclusion | Modeling note |

|---|---|---|

| Earned salary through close | Ordinary wages | Typically not the core of “parachute” storytelling—verify |

| Transaction bonus labeled “CIC” | Often scrutinized first | Watch net vs gross, clawbacks, and repayment terms |

| Single-trigger RSU acceleration | Big ordinary income event | Equity ops + payroll must align share delivery with taxable event timing |

| Cash severance | Often front-and-center | Installment vs lump sum can change present value elections and employee cash flow |

| COBRA / benefits top-ups | Sometimes smaller dollars | Still need characterization—do not ignore “small” lines in bulk |

If you add these rows and the 3× corridor still looks “close,” that is when teams run sensitivity tables (±5% on equity marks, ±1 year on earnout timing, alternative base amount calculations). The point is not to predict your tax—it is to show why diligence is iterative.

What this article will not do

We do not provide transaction-specific conclusions, withholding instructions, or state-by-state golden parachute outcomes. We also do not claim that any blog “safe harbor” phrase replaces statutory text. When your counsel says “the model says,” ask which definition path produced each listed dollar.

Quick reader checklist before you close the tab: Did you separate headline severance from payments that are actually contingent on a qualifying change? Did you ask whether gross-ups appear in multiple drafts of your agreement? Did you identify who owns withholding obligations—seller, buyer, or portfolio company payroll?

If you answered “not sure” to each question, treat that uncertainty as your cue to escalate—not as an invitation to negotiate harder on vibes alone.

High-level visual of how corporate change-in-control pay stacks can trigger golden-parachute modeling (280G/4999)—educational only, not individualized tax advice.

Footnotes

Primary Sources

Disclaimer: This guide is for general education only and is not individualized tax, legal, or investment advice. Tax rules change, and your facts (employer plan design, residency, treaty status, payroll reporting) may differ. Consult a qualified tax professional before making decisions.

Footnotes

-

Sections 280G and 4999 are read together in practice: definitions and deduction questions are usually 280G; the 20% excise sits in 4999 once excess parachute payments exist under the statutory tests. ↩

-

Shortcut math is a common failure mode: “excess parachute payment” is not the same as total parachute payments minus base amount in the colloquial sense—use the statute (and professional modeling) for your facts. ↩